Introducing Consolidation

Welcome back to the Aimco public REIT valuation series. Here, we’re going to unpack consolidation, which has already reared its head in the figures we pulled for the previous post on GAV. When building public company net asset value (NAV) analyses, it’s important to handle consolidation consistently and back out minority interests as needed.

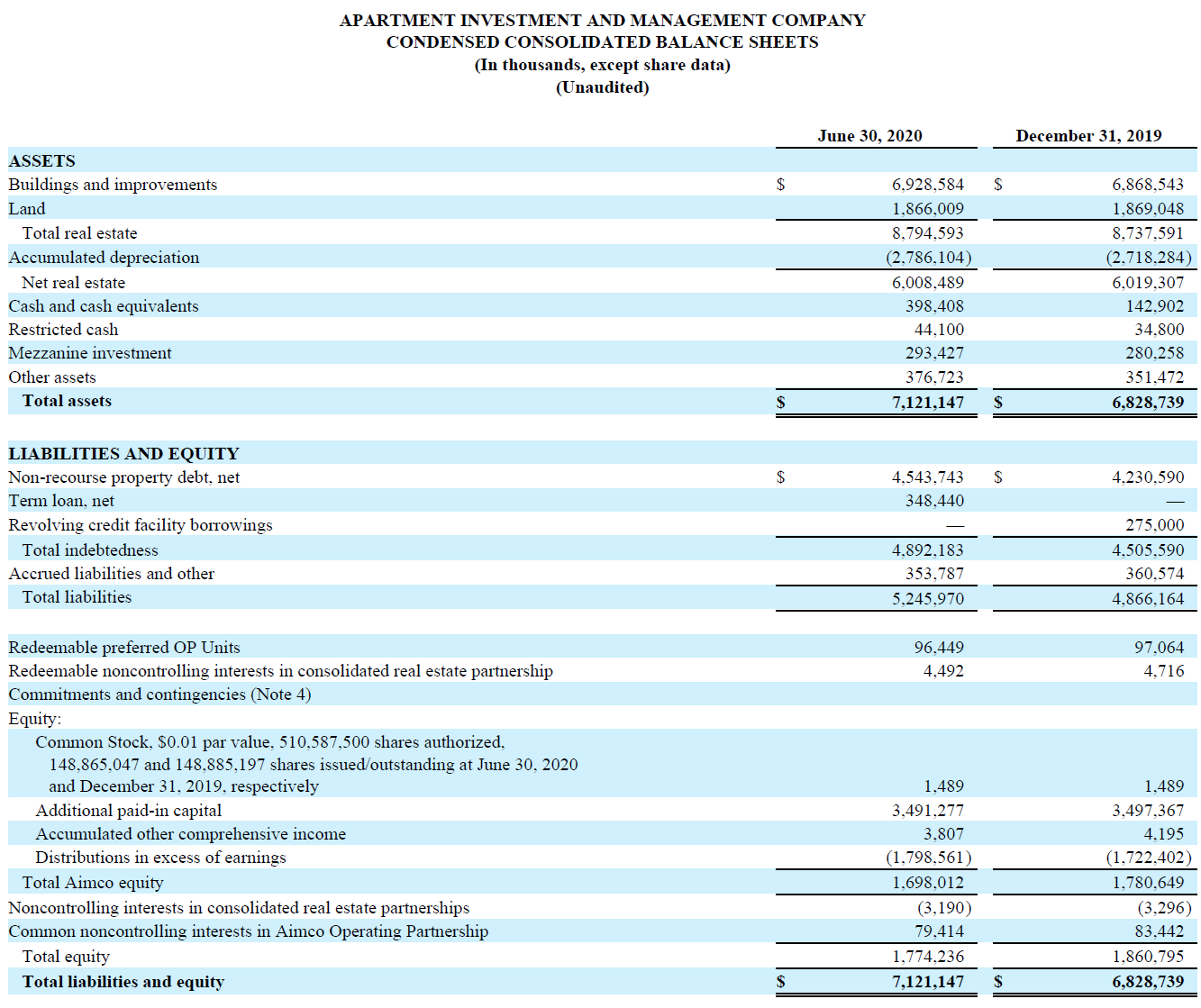

If these concepts are foreign to you, or if you’d like a refresher on this real estate private equity skill, you’re in the right place. Below is a snipping of our reference balance sheet followed by a high-level discourse on consolidation as it relates to a real estate private equity career path.

Where do we encounter consolidation?

So if you look at the top of the balance sheet, you’ll read “condensed consolidated balance sheets.” This means every number you read is a consolidated figure. In fact, nearly every figure reported in the 10Q is consolidated, unless otherwise noted. But to understand what consolidation truly is, let’s back up and think about how Aimco exists not as one single company but as a collection of interconnected legal entities.

How Consolidation Aims to Simplify a Complex World

In the real world, Aimco is a series of interconnected entities that own percentages of each other in a hierarchical structure. In its true form, however, Aimco is a bunch of child companies controlled in a chain of ownership that ultimately ends with AIMCO Properties, L.P. as the parent entity. Yet, it would be needlessly cumbersome to publicly report information for each entity. So, accountants use consolidation to simplify Aimco’s presentation and show it as if it were a single entity.

So in the consolidated world, this complex web of entities is flattened into a singular “Aimco.” Now, this flattening would be straightforward if the parent entity owned 100% of each child entity, and each child entity owned 100% of its children. In this straightforward world, you would just sum everything together. But the world is complex, and the true structure of Aimco’s joint ventures likely involves ownership stakes ranging from 100% – 50%, 50% to 20%, and less than 20%.

Specific Examples of Consolidation

These three percentage buckets are important delineations in the world of consolidation. In short, consolidation typically handles these buckets of ownership as follows:

- 100% to 50%: Any entity that Aimco owns more than 50% of is shown at its full 100% value. So, if Aimco owns 51% of a $100M apartment building, then The $6.92B asset line for “Buildings and improvements” above would be representing the full $100M value and not the pro-rata $51M.

- 50% to 20%: Entities owned in this band are generally accounted for under the equity method. This method reflects the investment value at the corresponding ownership percentage. So, a 39% stake of a $100M apartment building would be reflected as $39M. Note, this contrasts with how a 51% stake in that same apartment building would be reflected as a full $100M, per the above bullet.

- Less than 20%: Aimco would use cost method accounting to represent anything owned under a 20% stake. Cost method accounting would represent the ownership stake as its pro-rata investment value at cost. So a $15M investment to own 15% of a $100M apartment building would be shown at $15M, and the value wouldn’t fluctuate as would other fair market value-based accounting methods such as the consolidated and equity methods mentioned above.

If you aren’t familiar with consolidation, these methods might jump out at you – particularly the first. But there is a plug at the bottom of the balance sheet that adjusts for these gaps in ownership percentage. The noncontrolling interest lines back out the bits of value that Aimco doesn’t actually own in the consolidated figures.

Conclusion

We’ll dive further into the specifics of consolidation as needed. For now, we’ll model Aimco with its consolidated figures and reverse out noncontrolling interest at the end. This is a fine way to handle consolidation for a high-level model. If we, as a theoretical private equity fund, were to get private information (after signing an NDA in a formal process that Aimco hypothetically invites us to), or otherwise try to build a full asset-by-asset model, we might ultimately skirt around using consolidated figures. This is because we would then be working bottom-up, rather than top-down as we are now with public figures.

Learn with Leveraged Breakdowns

Leveraged Breakdowns teaches you the full suite of real estate private equity skills necessary for success in this competitive industry. From nuanced concepts such as the above discussion on consolidation to direct Q&A interview guides, we have everything to set you on the right path down your real estate private equity career path. Check out all we have to offer, everything is made by industry insiders with years of continued megafund experience!