Executive Summary / “TLDR”

Industrial is a core sector within commercial real estate and is a popular sector for real estate private equity firms to invest in. Industrial’s main purpose is to store goods and facilitate the distribution of goods from manufacturers to retailers and direct to consumers. The industrial sector was favorably impacted by the COVID-19 pandemic, which accelerated existing trends that were already in-place pre-pandemic — namely, the buying of retail goods online, or e-commerce.

E-commerce retail sales inflected higher as a result of the pandemic, due to mandated quarantine and the need to have goods delivered to one’s house vs. shopping in-person at retailers. The industrial real estate market is the backbone of the e-commerce space, serving a key role in the distribution of goods. As a result, demand for industrial space, which was already strong pre-pandemic, has accelerated and is likely to remain very robust going forward.

Quick Note: Think of this blog post as part industrial real estate primer and part industrial sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to touch on the things that really matter for a sector in just a few, easily digestible pages.

Types of Industrial Real Estate

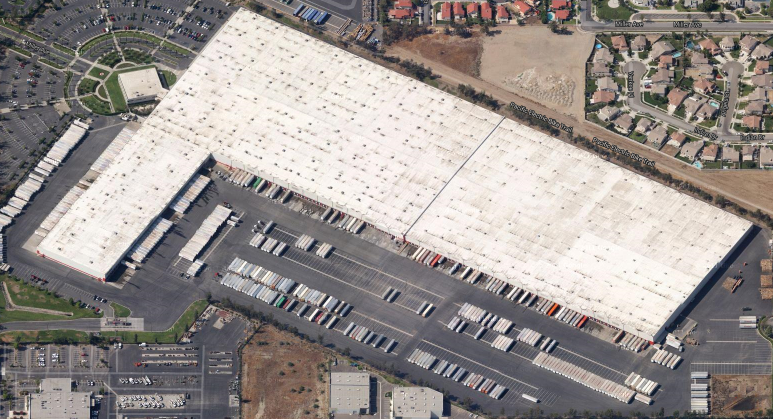

While the main purpose of industrial real estate in the U.S. is to store and distribute goods, there are other functions, including manufacturing, research and development, service, showroom space, and even cold storage. The size of an industrial building ranges from 25-50k square feet at the low end to more than one million square feet at the high end (for context, one million square feet is about 20 football fields lined up side-by-side). Ceiling heights or “clear heights” are an important metric in the industrial sector, generally ranging from 20 feet to as high as 40 feet for large bulk distribution centers. Below is an aerial view of a large industrial building, with multiple dock doors along its side where trucks can pull up to drop-off and receive goods.

Source: https://www.mwpvl.com/html/target.html

In terms of industrial market segments, industrial real estate is generally divided into a few categories:

- Warehouse Distribution

Warehouse distribution makes up the majority of industrial real estate in the U.S., and can further be subdivided into two categories:

- Regional distribution: regional distribution facilities are traditional industrial warehouses with 20-30 foot clear heights that facilitate the distribution of goods in a given regional area.

- Bulk distribution: bulk distribution facilities are very large buildings (250k+ square feet, 40-foot ceiling heights) that facilitate the distribution of goods over a larger geographic area. An example of this type would be an Amazon fulfillment center, with an average size of around 800k square feet. Amazon currently has just over 100 of these facilities in the U.S.

Below is an image of the inside of a large bulk distribution facility, with goods stored up to the ceiling (this illustrates why clear heights are important):

Source: https://pxhere.com/en/photo/663063

- Manufacturing

Manufacturing industrial buildings are used by tenants for the assembly and production of goods. In some cases they also have a smaller component of warehouse space and office space alongside the manufacturing space. These buildings typically have high power requirements, in order to facilitate the use of heavy machinery.

- Flex (short for “flexible”) Buildings

Flex industrial buildings offer tenants multiple areas for alternative uses. The mix of uses may include some combination of showroom space, research and development space, warehouse space, and office space. Flex buildings are popular in the technology industries, given that they can serve multiple uses at a single location.

Asset Quality

Most core commercial real estate is classified by quality into Class A, Class B, or Class C real estate. In the case of industrial, there are several key characteristics that impact the quality classification:

- Location: location is always important in real estate, but the key factors for industrial include distance to airports, seaports, major highways, rail hubs, or large manufacturing facilities; a central location for regional distribution also makes an industrial building more desirable.

- Clear Height: clear height is the distance from the floor to the ceiling of a building, with a higher distance being better. Clear height governs the maximum storage capacity for a building, as illustrated in the picture above.

- Bay Depth and Width: bay depth and width is the distance between vertical support beams of the building, with larger being better. This is because the size of the bays directly impacts how efficiently goods can be moved through the building.

- Dock Doors and Trailer Parking: the number of dock doors in a building governs the amount of trucks that can service the building at one time. Trailer parking is also important in order to accommodate the storage of goods in trailers on-site.

Users of Industrial Real Estate

The below chart is sourced from CBRE’s March 2021 Industrial Outlook report, where they detail the top industries represented in North America CBRE industrial transactions in 2020. By far, the two most represented industries include e-commerce (i.e. Amazon) and third-party logistics (i.e. UPS, FedEx). Users from these two industries account for more than half of all CBRE industrial transactions in 2020. While 2020 is just one transaction year, it is also a pivotal year due to the structural economic shifts caused by COVID. Thus, this is probably a reasonable proxy for industry demand in the near-to-medium-term. Below is the chart of user type:

User Market Share from North America CBRE Industrial Transactions in 2020

| Industrial Building User Type | % Share of Transactions in 2020 |

| E-commerce | 27% |

| Third-Party Logistics | 26% |

| General Retail & Wholesale | 25% |

| Food & Beverage | 10% |

| Auto | 4% |

| Medical | 4% |

| Other | 4% |

Lease Structure

The typical industrial lease is 3-5 years in length, which is on the shorter end when compared to other core commercial property types (i.e. office and certain types of retail). In the current market environment, where industrial rents are rising quickly, this is favorable to landlords since it allows them to capture changes in the underlying economy as leases rollover. For very large industrial developments leased to single users, however, leases are typically longer in length, with lease terms up to 10-15 years.

Leases can either be structured as 1) net leases, 2) gross leases, or 3) modified gross leases. With net leases, the tenant pays a net rent and is responsible for covering all of the operating expenses of the building. Net leases are very common for single-tenant buildings. Gross leases are where the tenant pays a higher gross rent, but is not responsible for any of the operating expenses of the building. Gross leases are more common for multi-tenant industrial buildings with many users. Lastly, modified gross leases are a blend of the two, where the tenant pays a gross rent but is responsible for certain of the operating expenses of the building. For more detail on lease types, please see our post on leasing fundamentals.

Top Industrial Markets

The top 10 North America industrial markets are listed below, per a CBRE report. Note that they are spread out regionally, and tend to be located in close proximity to major coastal ports or rail lines.

North America Top Ten Industrial Markets by Square Feet

| Market | Million Square Feet |

| Chicago | 570 |

| Southern NJ/Eastern PA | 470 |

| Northern/Central NJ | 396 |

| Dallas/Fort Worth | 387 |

| Inland Empire (Southern CA) | 359 |

| Atlanta | 310 |

| Toronto | 258 |

| Los Angeles | 212 |

| Indianapolis | 179 |

| Columbus | 177 |

Demand Drivers

The primary demand drivers for industrial real estate include the following:

- Retail Sales (including e-commerce)

- Retail Inventories

- Import Volume

- Business and Manufacturing Activity

The way that industry professionals generally determine demand drivers for industrial real estate is to look at correlations between the growth rates of the above factors and industrial square feet absorption. High correlations are generally in the 0.5-0.7 range, which indicates a pretty solid directional relationship between the given factor and demand for industrial space. Below we outline the primary demand drivers.

- Retail Sales (including e-commerce)

Retail sales are tracked and reported by the U.S. Census Bureau on a monthly basis. Retail sales growth has generally trended between 1% and 6% annually for the majority of the last economic cycle (2009 – 2020), before dipping to negative 15% in April 2020 due to the COVID-induced economic shutdown. Retail sales growth has meaningfully recovered since then, and in March/April 2021 spiked to more than 30%1. This is somewhat of an anomaly due a variety of factors, but retail sales growth is likely to remain very robust for a period of time as the economy continues to re-open post-COVID.

E-commerce sales have been a big driver of retail sales growth over the last several years, with e-commerce growing in the 11%-15% range annually. E-commerce growth inflected higher as a result of COVID, moving from the low double-digit range to more than 30%2. E-commerce sales now represent about 10% of all retail sales3. While e-commerce is still a small piece of the retail picture, it is a key driver and is quickly becoming more important over time. As retail sales increasingly shift from in-person to online, this drives significant demand for industrial space. This sounds obvious, but the reason is that the space required to fulfill an online order in an industrial building is a multiple of the space required to fulfill that same order in a retail store (estimated at three times the required space, per Prologis4). So not only is demand for real estate shifting from retail space to industrial space, but it is happening at a multiplied rate.

- Retail Inventories

Retail inventories are measured by the Retailer Inventories to Sales Ratio published by the U.S. Census Bureau5. This ratio has been fairly steady over time, but did sharply decrease due to the COVID pandemic, when supply chains were disrupted and retailer inventories fell to all-time lows (you probably experienced this anecdotally during the COVID pandemic, when normal retail purchases were frequently out of stock both in-store and online). Post-pandemic, many retailers are now shifting from “just-in-time” inventory management to “just-in-case” inventory management, where retailers will have higher inventory levels as a precautionary measure against future supply-chain disruptions. This will likely lead to greater demand for industrial space, as inventory levels trend higher along with industrial space requirements.

- Import Volume

Import volume reflects the volume of trade with other countries. As more goods enter the country, there is more space needed to store those goods on the way to reach the end consumer. Import volume is measured on a quarterly basis by the U.S. Bureau of Economic Analysis6. Seaport volume, a subset of import volume, is especially correlated with industrial demand. When goods come into the country via large coastal seaports (i.e. Port of L.A. or Port of Houston) they drive demand for industrial space in large geographic areas surrounding the ports.

- Business and Manufacturing Activity

The ISM Manufacturing Index7, measured on a monthly basis by the Institute of Supply Management, tracks the change in production levels across the U.S. economy. Historically, this metric has been moderately correlated with demand for industrial space. A ISM score above 50 indicates an expansion of the manufacturing economy. The ISM Index fell from 50 pre-COVID to about 41 at the low, before rebounding to 60+ in 1Q 2021.

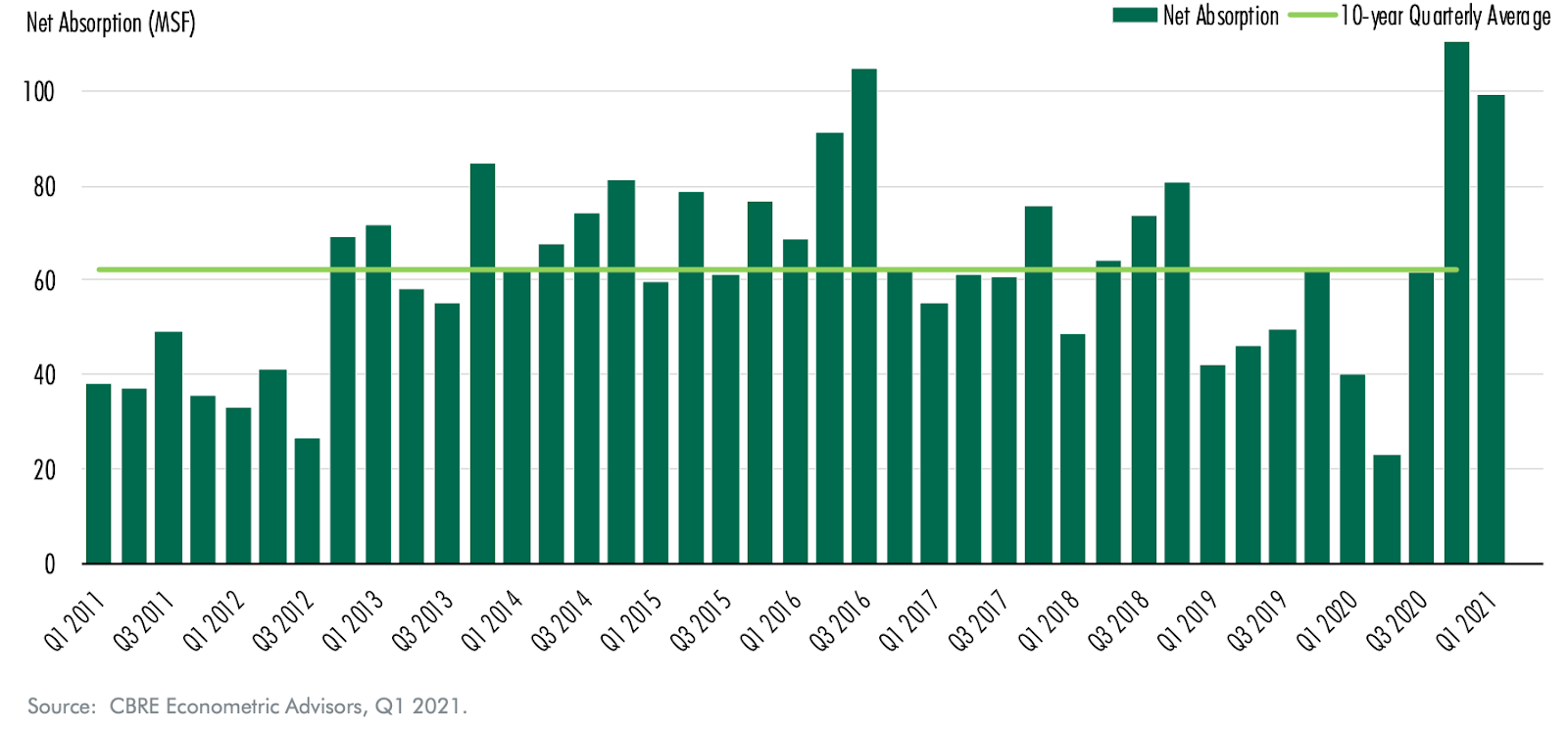

While some of the above industrial demand drivers took a hit during the early stages of the COVID pandemic, some even accelerated, like e-commerce sales. Those that took a hit have rebounded strongly as the economy has reopened post-COVID. This has translated to very robust absorption of industrial space for the Q4 2020 and Q1 2021 quarterly periods, as indicated in the chart below. Going forward, demand for industrial space is likely to remain very strong as the economy further reopens, inventories are replenished, and e-commerce becomes an even greater percentage of overall retail spending.

U.S. Industrial Space Absorption

Supply

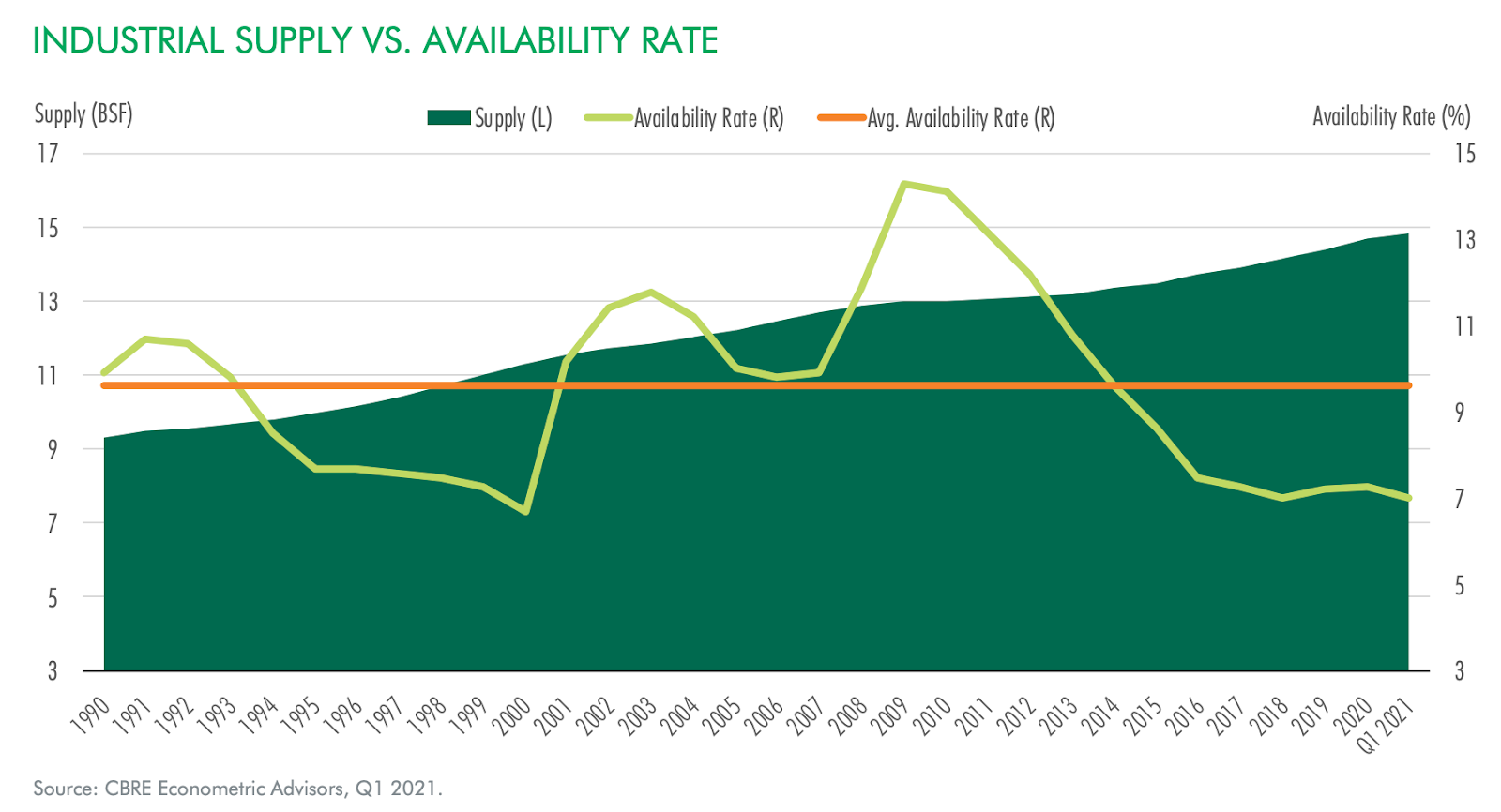

As you might expect, given the strong demand for industrial space that has emerged over the last several years, new construction has progressed at a steady pace to meet increased demand. The below chart from CBRE shows the long-term supply of U.S. industrial space, which has seen a modest uptick from about 2013 – 2020 (13 to 15 billion square feet of industrial space). Despite the increase in supply over the last several years, demand has more than met this new supply, resulting in a steadily declining vacancy rate over time (represented by the light green line, below).

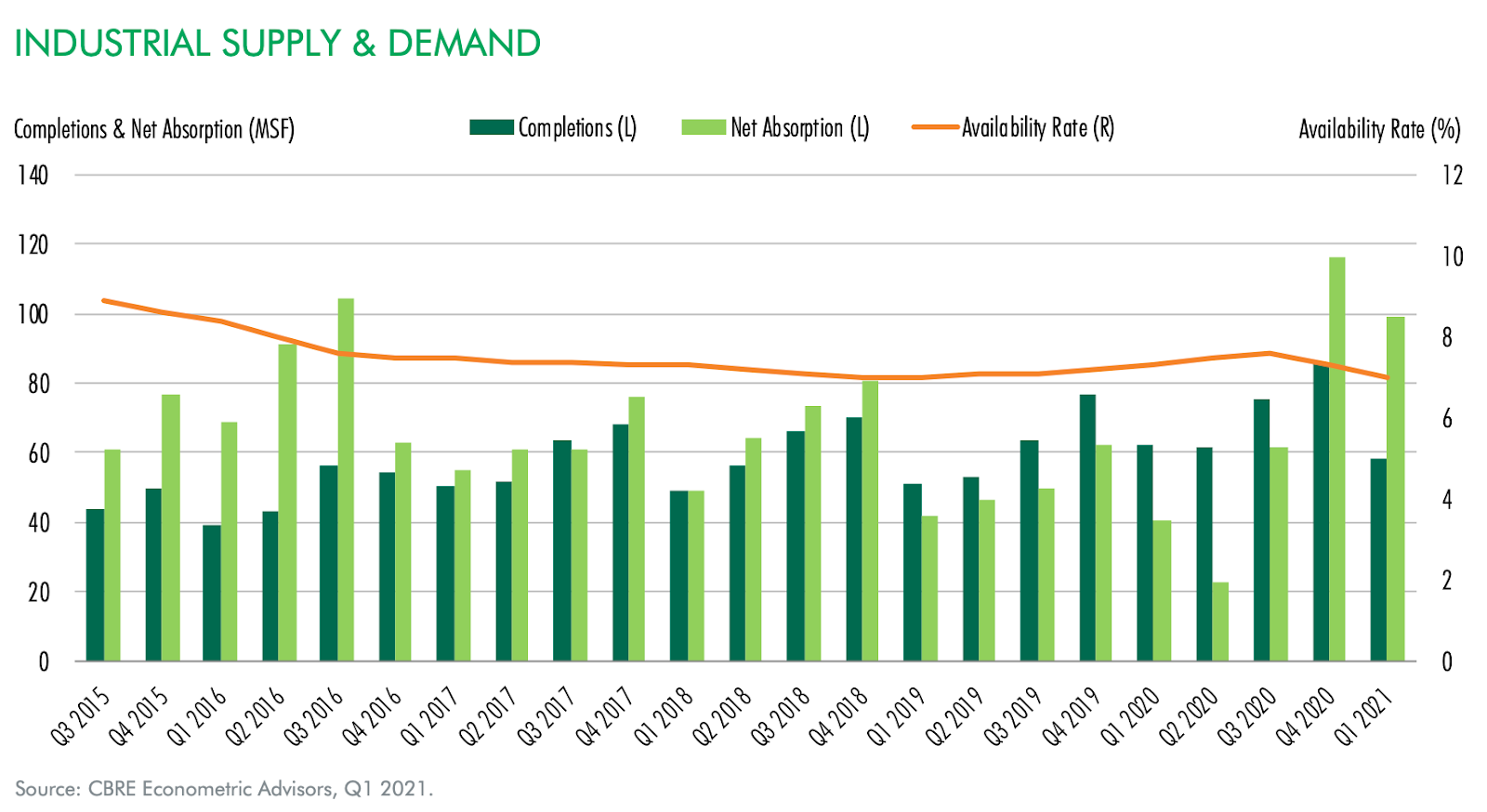

Lastly, the below chart from CBRE shows industrial space absorption alongside new supply on a more condensed timeline (2015 through 2020). As you can see from the below chart, historical absorption (light green bars) has exceeded new supply (dark green bars) for the majority of the time. This has resulted in a modestly lower vacancy rate over this period, represented by the orange line below (from 9% vacancy to 7% vacancy).

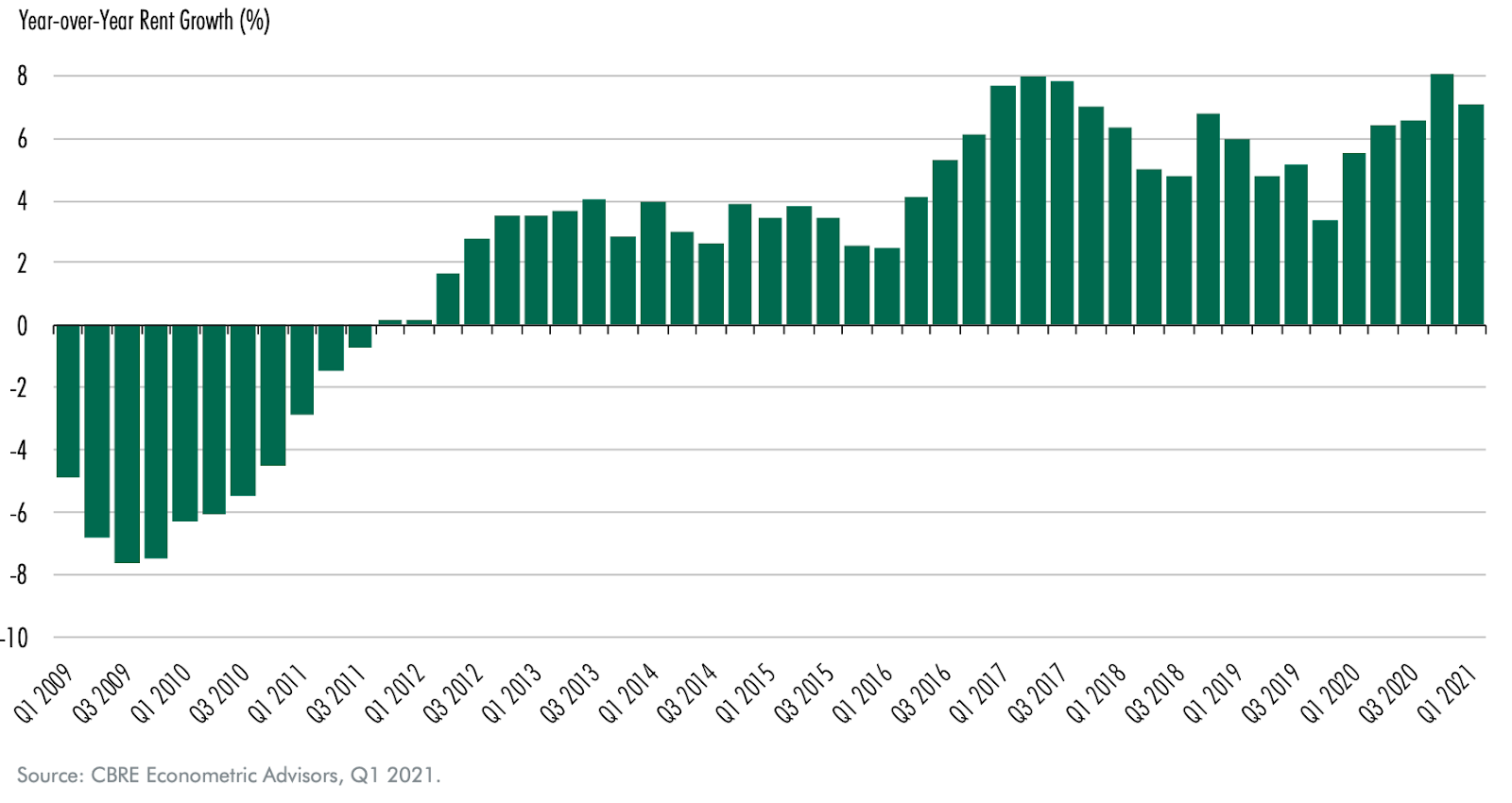

Pricing Power / Rent Growth

Given the strong demand for industrial space that has exceeded new supply over the last several years, landlord pricing power has gone up and rent growth has accelerated. The below chart from CBRE shows year-over-year rent growth for the U.S. industrial market. After recovering from the 2008-09 financial crisis, industrial rent growth hovered in the 2%-4% range for a couple of years, before accelerating to the 4%-8% range for the next few years. This is very solid rent growth, well above inflationary levels. This rent growth factor has helped the industrial sector differentiate itself vs. other core real estate sectors over this time period.

Conclusion

Demand for industrial space has been very strong for the last several years, mainly driven by the incremental space requirements needed to support e-commerce sales (Amazon has been a big part of this). The COVID pandemic has positively impacted growth in e-commerce sales, and in-turn industrial demand. Other factors that correlate with industrial demand took a temporary hit, but have bounced back and appear to be trending positively over the near-term.

The primary risk to the sector is probably overbuilding, given strong investor interest in the sector, ease of capital, and short construction cycles. Longer-term technological risks include the mass adoption of self-driving trucks (reduces transportation costs of goods and potentially reduces the demand for industrial space), drone delivery, and 3D printing. All that said, given that demand is likely to remain very robust for the foreseeable future, the outlook for the sector is very positive.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.