Executive Summary / “TLDR”

Data centers, or large buildings that house racks of servers to store data, serve an important role in the increasingly digital world. While the data center sector is not dominated by traditional real estate private equity firms, it is worthwhile to have a baseline knowledge of the sector. This overview reviews items like lease terminology, major markets and companies, and supply/demand trends.

Also worth noting, in the last several years there has been an acceleration of interest by capital providers in the sector, which has put some downward pressure on development yields. Over the last several years yields have moved from the low-teens to the high-single-digits. Though this is also part of the natural life cycle of a sector maturing and achieving a lower cost of capital. The bottom-line is that the underlying long-term drivers for the sector remain very positive, likely inflecting higher post-COVID, serving as a positive secular tailwind for the sector going forward.

What are Data Centers?

Data centers are large buildings that are constructed to house racks of servers that store data and connect internet traffic. Anyone that has spent a couple of decades in the workforce may remember a time when their company or organization had an “IT closet” that stored racks of servers. Today, the majority of companies outsource this function to third-party data centers that provide this service in exchange for a monthly rent payment. Data centers are similar to other real estate sectors except that they provide space for servers, not people.

Types of Data Centers

There are two main types of enterprise data centers:

- Hyperscale data centers

- Colocation data centers

Hyperscale data centers are typically very large buildings owned by data center companies (i.e. Digital Realty Trust) that are occupied by one or a few large tenants. In some cases, they may be owned by the single tenant or net-leased by that tenant. Amazon Web Services, for example, leases many hyperscale data centers.

Colocation data centers are buildings owned and/or managed by data center companies (i.e. Equinix) that have racks of servers leased by smaller tenants. This type of data center allows enterprises to outsource their data storage needs and effectively move that expense item from a fixed cost to a variable cost that can scale up and down as needed.

From an investor standpoint, Hyperscale data center deals typically have lower yields and minimal rent growth, but also have longer-term leases to very large companies with minimal credit risk (think blue-chip companies like Amazon or Facebook). Colocation data center deals have higher yields and more rent growth, but also have shorter-term leases to smaller tenants that typically have more credit risk.

Lease Structure and Terminology

Unlike most traditional real estate leases, data centers leases are structured in terms of power consumption, measured in megawatts, rather than square feet. One megawatt is equal to one million watts, which is enough capacity to power about 500-1,000 homes at any given moment. For reference, the largest data center in the world in China has a capacity of about 150 megawatts. In terms of leasing, at the current time, multi-megawatt deals are generally considered to be larger leases in the data center space. In total, the U.S. multi-tenant data center industry leased 700 megawatts of capacity during the full year 20201.

More Terminology: Private, Public, and Hybrid Cloud

Over the last 10-20 years, there’s been a big shift in enterprise data storage from on-premise, i.e. physically at the office, to the cloud, i.e. in cyberspace. The cloud is a much more efficient way to store enterprise data, since the cloud is easily accessible from anywhere and can also be flexed up and down as the needs of the enterprise change. Within the cloud framework, there are three types of cloud models that are employed by enterprises today:

- Private Cloud

- Public Cloud

- Hybrid Cloud

A private cloud is a cloud environment that is designed for a single organization. This model can make sense for very large organizations that need their data solutions to be tailored to their specific needs, but can also be expensive. The less expensive alternative is the public cloud, which is a cloud environment offered by third-party cloud providers, such as Amazon Web Services or Microsoft Azure. These cloud providers lease large data centers and effectively rent out cloud storage to companies that purchase it at retail prices. The majority of enterprises use a hybrid cloud model, where they combine the private cloud with the public cloud. For example, an enterprise may use a private cloud for storing more sensitive information or running specific workloads, while utilizing a public cloud for the rest of their data storage and compute needs.

Largest Data Center Markets

Data centers tend to be clustered in certain markets, based on a number of factors including: historical proximity to Network Access Points (NAPs) introduced in the early internet infrastructure of the 1990s, proximity to transcontinental undersea telecom cables, availability and cost of power, susceptibility or lack thereof to natural disasters, and cost of land.

The largest data center market in the world by far is Northern Virginia, which has nearly 1,200 megawatts of capacity, almost double that of the second-largest global market (Tokyo). Several factors have contributed to Northern Virginia becoming such a big data center mecca, including 1) Northern Virginia being designated a Network Access Point during the rollout of the early 1990s internet infrastructure; 2) its geographic location both near transatlantic telecom cables and central location on the east coast of the U.S., which allows it to serve large metros up and down the east coast with limited latency; 3) its proximity to large users in the Washington DC area, including government agencies, defense contractors, and cybersecurity companies; and 4) the availability of low-cost land in the area and reliable access to power.

Below are the top 10 global data center markets in 2021, per a Cushman & Wakefield report2. Note that the top U.S. markets are Northern Virginia, Silicon Valley, Dallas, and Chicago, which are geographically distributed throughout the country in order to evenly serve various metro areas with limited latency.

Top global data center markets in term of power capacity:

- Northern Virginia (approximately 1,200 megawatts)

- Tokyo (725 megawatts)

- London (650 megawatts)

- Shanghai (590 megawatts)

- Silicon Valley (550 megawatts)

- Dallas (400 megawatts)

- Singapore (400 megawatts)

- Frankfurt (390 megawatts)

- Chicago (375 megawatts)

- Beijing (350 megawatts)

Largest Data Center Companies

Below is a list of the top U.S. data center companies3. Note that five out of seven of these companies are public companies, and a sixth (Cyxtera) is currently in the process of going public via a SPAC deal. The big four public data center companies are all structured as REITs.

- Equinix (approximate $60 billion market cap)

- Digital Realty Trust ($40 billion market cap)

- CyrusOne ($8 billion market cap)

- CoreSite ($5 billion market cap)

- Cyxtera

- Lumen ($15 billion market cap)4

- Flexential

Capital Flows

For nearly a decade post-2008-09 financial crisis, investment in the U.S. data center market was dominated by the major REITs (Equinix, Digital Realty Trust, CyrusOne, etc.). However, due to attractive double-digit development yields and the perceived secular tailwind of data consumption, in the last several years the sector has attracted other types of capital. Private equity firms have invested in the data center market in a big way, alongside digital infrastructure funds, and even sovereign wealth funds. Given the low required return on capital for the latter two capital providers, and more competition to invest in the space generally, development yields for new-build data centers have come down considerably in the last several years (from the low-teens to the high-single-digits). Joint venture deals have also become more popular, where less operationally-experienced players (i.e. sovereign wealth funds) can invest capital via JV deals with the public REITs.

Big Picture: Data Growth Driving Demand

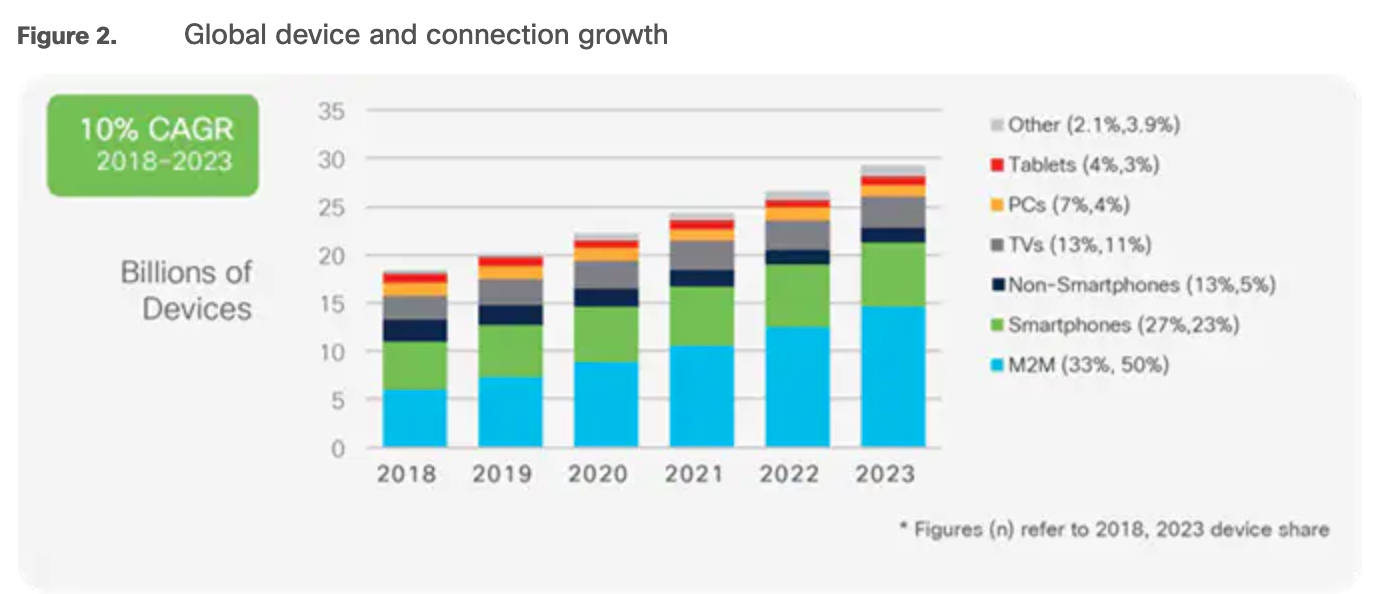

Cisco publishes a widely followed annual Internet Report where it forecasts a variety of metrics related to the internet, including global internet growth and device connectivity. This report is useful for sizing up the big picture demand profile for data centers. Simply put, if the world is using more data, there’s more need for capacity to store that data. Below is a chart from the latest Cisco Internet Report on forecasted global device connectivity. This chart shows a 10% CAGR from 2018-2023. This is a robust growth rate, but also note that the latest report was published pre-COVID. It is very likely that growth rates have notched higher following the COVID pandemic, where remote work, education, and personal connection have all become mainstream.

Chart from Cisco Annual Internet Report on Global Device Connection Growth (published March 2020)

Source: Cisco Annual Internet Report

Looking further into the future, growth in data will likely be driven by a few major technological themes that are still in the very early stages, including a proliferation of the internet of things (IoT), more mainstream applications of artificial intelligence, and the build-out of 5G broadband cellular networks.

What About Supply?

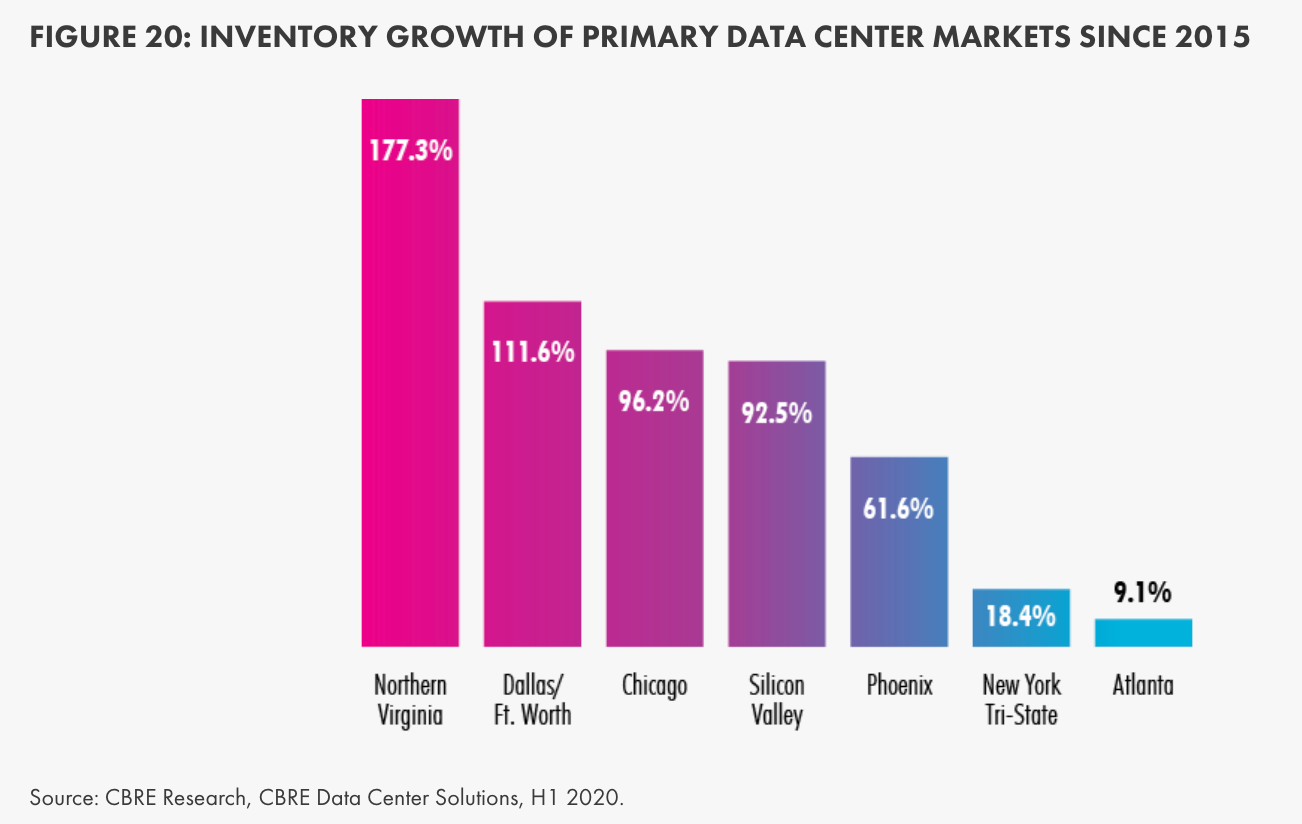

The U.S. data center inventory is constantly expanding, with new development chugging along to meet constantly ramping demand. Leasing of data center space tends to be somewhat cyclical, meaning that leasing can be elevated in a given quarter or year, before retreating for a period of time. This leads to occasional pockets of supply and elevated vacancy for a period of time, but it tends not to last very long. Historically, demand has always come back to meet supply, and the market has stayed in relative equilibrium.

The below chart from a CBRE data center outlook report illustrates the magnitude of the growth in inventory over the last five years, with inventory effectively doubling in several markets over this time (approximate 15% CAGR).

Chart from CBRE Data Center Outlook Report on Historical Inventory Growth

Conclusion

The data center market is a non-core property type in the real estate world, but is an important sector to follow, given its mission-critical role in an increasingly digital world. The underlying trends in data growth and consumption that support growth in the data center sector are very positive, and if anything have accelerated further following COVID. Technology is always evolving, and it’s important to keep an eye on potential disruptors to the space, particularly when evaluating investments over a long time horizon. Despite the more competitive capital environment for data centers in the last several years, the sector remains attractive, given the ever-increasing demand for data that is showing no signs of slowing down.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.

- https://www.datacenterknowledge.com/colocation/microsoft-bytedance-facebook-leased-more-us-data-center-space-anyone-2020

- https://cushwake.cld.bz/2021-Data-Center-global-Market-Comparison/24/

- Note that Amazon Web Services and Microsoft Azure are both cloud services companies. They rent server racks wholesale from data center companies and provide cloud capacity as a service to smaller companies at retail prices. In some cases they do own the data centers outright, but since they’re not leasing physical racks to other companies and instead providing cloud space as a service, they’re not actually considered data center companies in the sense that we’re talking about in this report.

- Note that Lumen is not a pure-play data center company.