Note: If you have not already read Part 1 of Office Sector Series, you may want to start there. Part 1 provides a basic overview of office real estate, including types of office buildings, factors that determine asset quality, and a discussion of office leasing and office capex. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Impact of COVID on Office Real Estate

Office has been one of the more affected subsectors by the COVID-19 pandemic, given that social distancing measures significantly disrupted the congregation of employees in offices. Given that COVID was such a significant catalyst that will likely change the nature of office real estate going forward, it is critical to review the various implications.

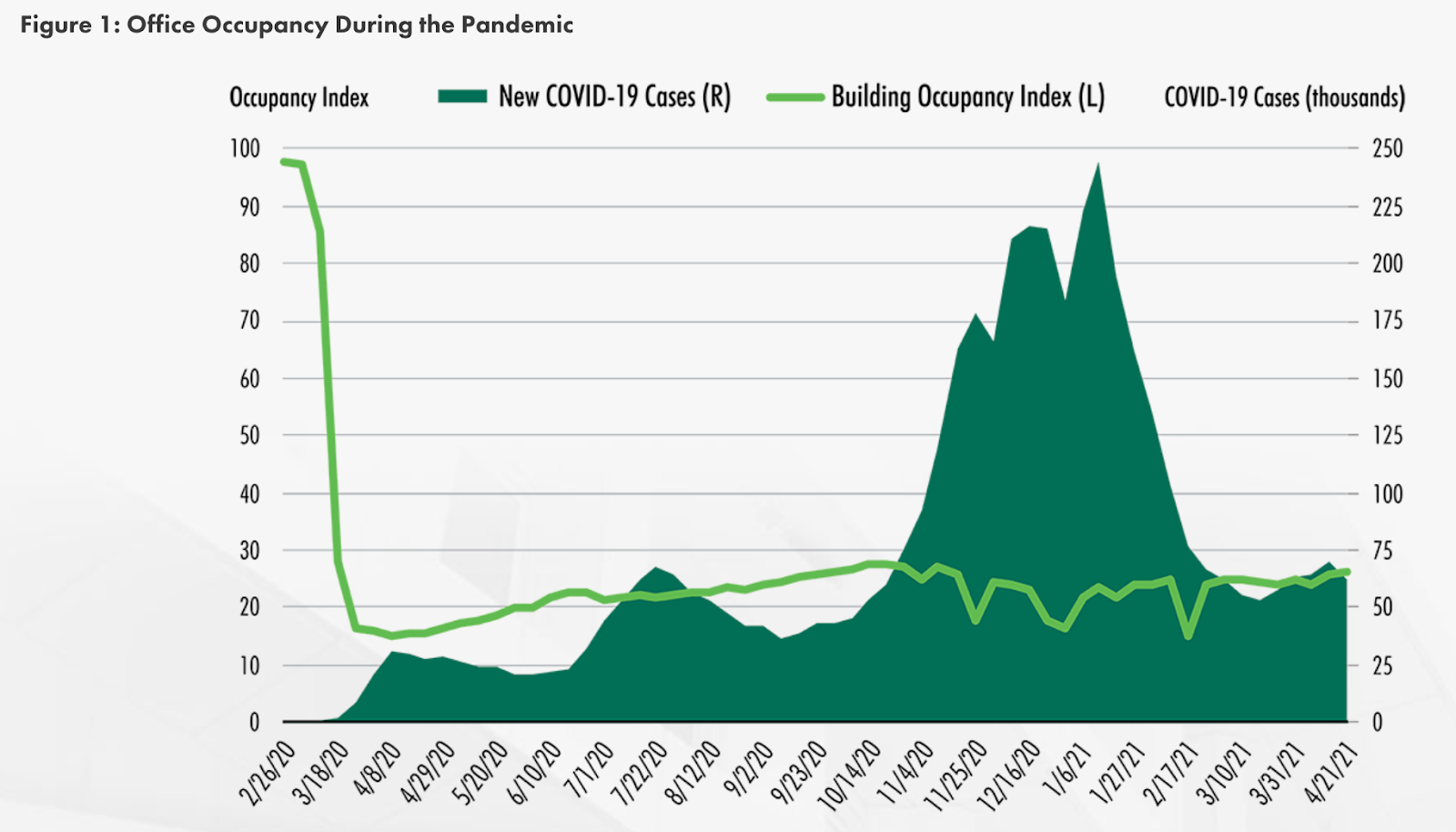

At the onset of the pandemic, many companies quickly shifted from a traditional office environment to work-from-home, in order to accommodate social distancing. This led to a severe decline in office building occupancy. The below chart from CBRE indicates that the office building occupancy index, which measures the actual space utilization of tenants, fell from nearly 100% to approximately 20% during most of the pandemic.

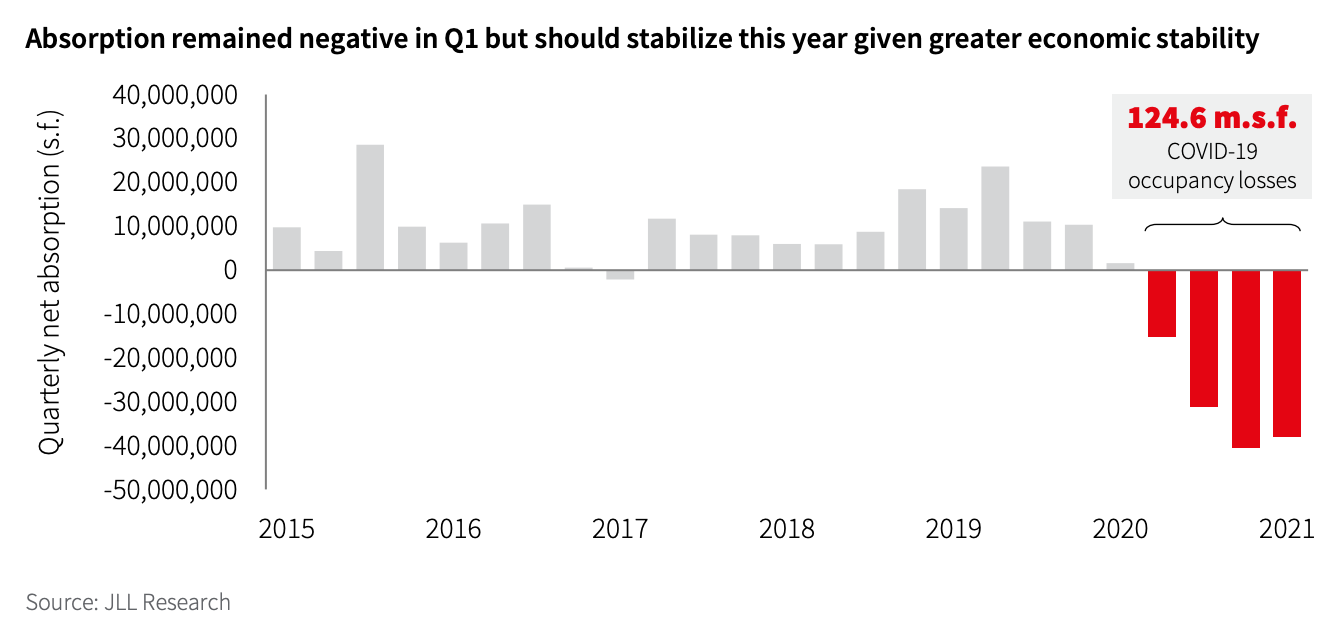

Meanwhile, office leasing fell off a cliff, as tenants with lease expirations vacated space, while many organizations put on pause decisions on new office space. As a result of these factors, office space absorption turned sharply negative since COVID, as indicated in the below chart from JLL.

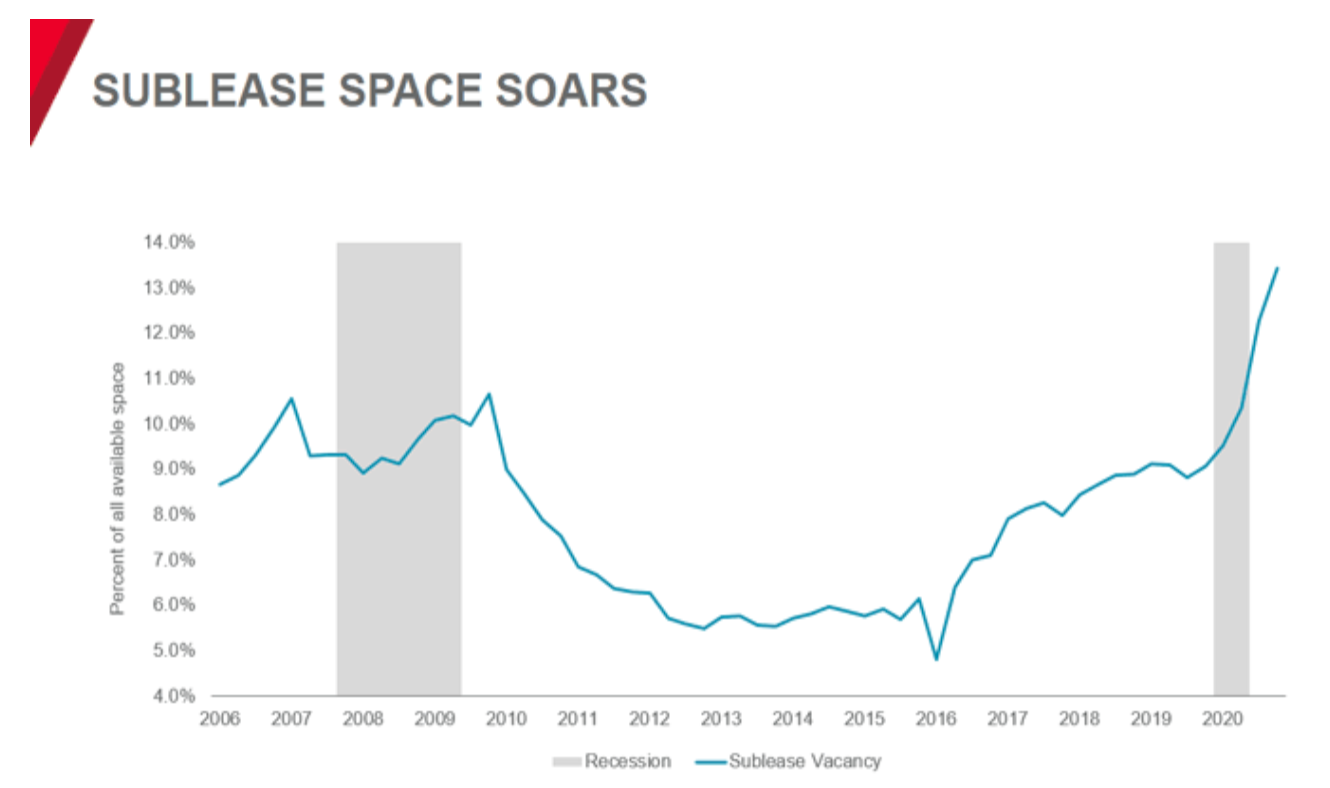

As the pandemic dragged on, many tenants began to realize that they didn’t need as much office space given that their organizations could run effectively with employees working from home. Thus, sublease space increased significantly, currently above levels reached during the 2008-09 financial crisis. The below chart from Cushman & Wakefield illustrates the sharp uptick in sublease space as a percentage of total available office space.

Source: Cushman & Wakefield

The concept of work-from-home gained mass adoption during the pandemic, when most non-essential workers stopped going into the office overnight. While as of mid-2021 there are signs of returning to work in a normal office environment, the massive work-from-home experiment has also taught many organizations and employees that they can be productive without going into an office. Thus, is it likely that at least a portion of the work-from-home culture will be sticky well beyond the end of the pandemic. Many big tech companies, including Microsoft and Google, have already adopted more permanent work-from-home or hybrid work policies. On the flip side, Amazon and Apple have taken a more office-centric approach so far. The large financial institutions have also been messaging a near full return to the office in the near future.

It remains to be seen what the end result is, but the consensus as of mid-2021 is that on average, office-using employees will work from home 1-2 more days than they did pre-pandemic (2 days work-from-home vs. 0-1 days pre-pandemic). This will reduce office-space utilization and potentially reduce demand for office space overall.

One counter balancing factor at play is density of office space. Prior to COVID, there had been a trend over the last decade towards more dense offices with open floor plans and less square feet per employee (i.e. rows of desks in a big open space, with fewer private offices). Many predict that post-COVID, this trend will reverse or at least stabilize, with organizations focusing on larger and more open shared space, in addition to less dense rows of desks. While expert’s estimates vary, the net impact from more work-from-home adoption offset by lower space density will probably result in less overall demand for office space post-pandemic.

Other new trends in office real estate incited by the COVID pandemic include the following:

- Shorter lease terms, which have already moved from an average of 8-9 years pre-COVID to around 6-7 years post-COVID1

- More focus on in-office health amenities (including air quality, natural light, outdoor access, and thermal comfort)

- “Hot desks” to easily accommodate different employees on different days

- More dedicated collaboration space (going forward, employees may come into the office with more intent to collaborate with team members)

- Touchless technology to provide access building areas without having to touch doors, elevator buttons, etc.

Office Demand Drivers

The primary demand drivers for office real estate include the following:

- Job Growth

Historically, job growth has been highly correlated with demand for office space. Simply put, as more individuals are employed by organizations, there is a greater need for space for those employees to work. Below is a chart showing total non-farm employees in the U.S. since the 2008-09 recession — the chart shows a steady climb upward in total employees, before taking a huge dip during COVID, and since then a recovery of more than half of the jobs lost.

Source: FRED Economic Data, U.S. Bureau of Labor Statistics

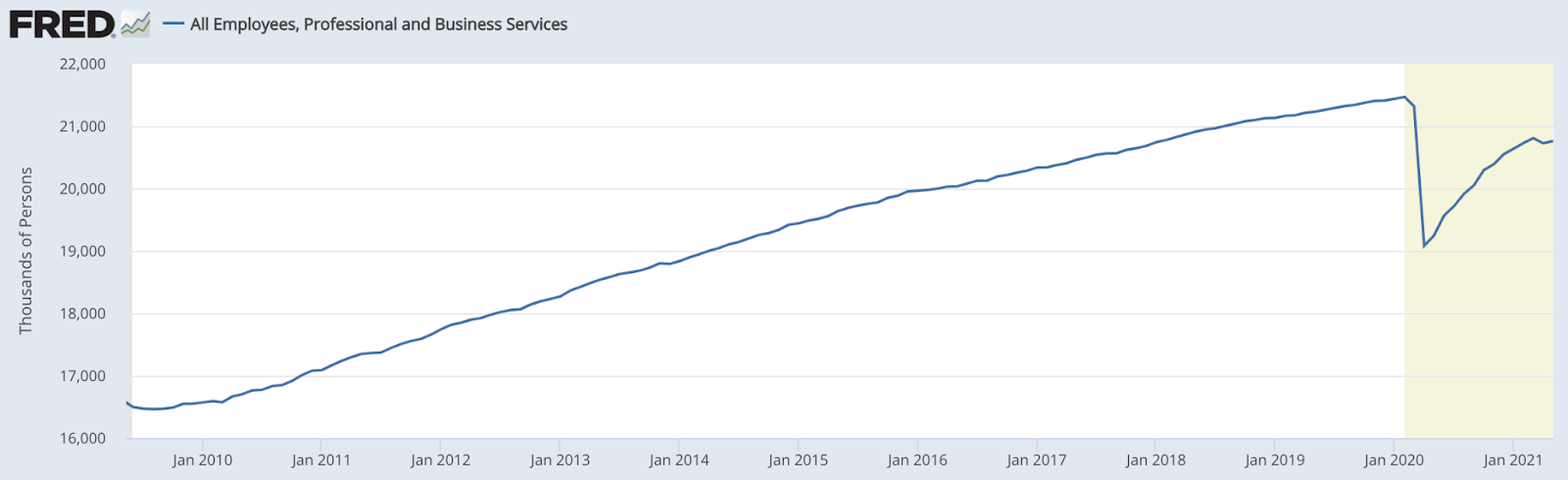

Drilling down a bit further, a more relevant measure of office-using jobs is total employees in the professional and business services sector. This sector classification comprises industries in which professionals generally work in an office environment. The below chart shows total employees in this sector since the 2008-09 recession. While this graph follows a similar pattern to the one above, the job losses are not as severe and the sector has recovered approximately 70% of the jobs lost.

Source: FRED Economic Data, U.S. Bureau of Labor Statistics

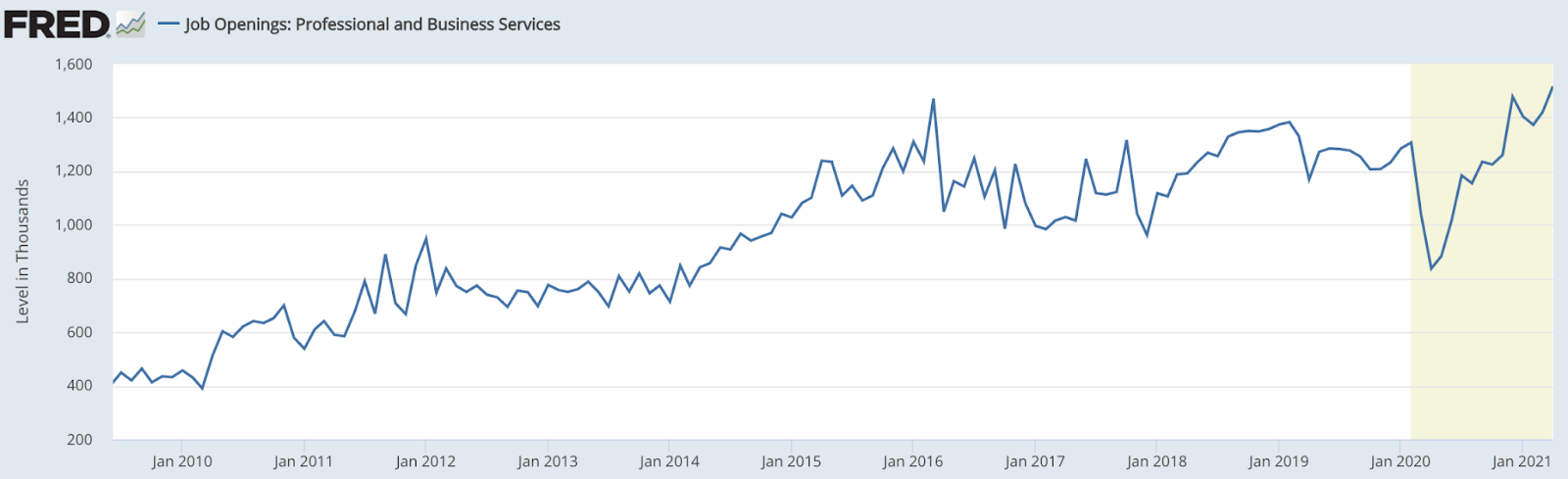

Lastly, a leading indicator of total employees is the number of job openings. Below is a chart showing total job openings in the professional and business services sector since the 2008-09 recession. This chart paints a less dire picture, indicating that job openings have risen fairly quickly off the post-COVID lows.

Source: FRED Economic Data, U.S. Bureau of Labor Statistics

- Corporate Profits

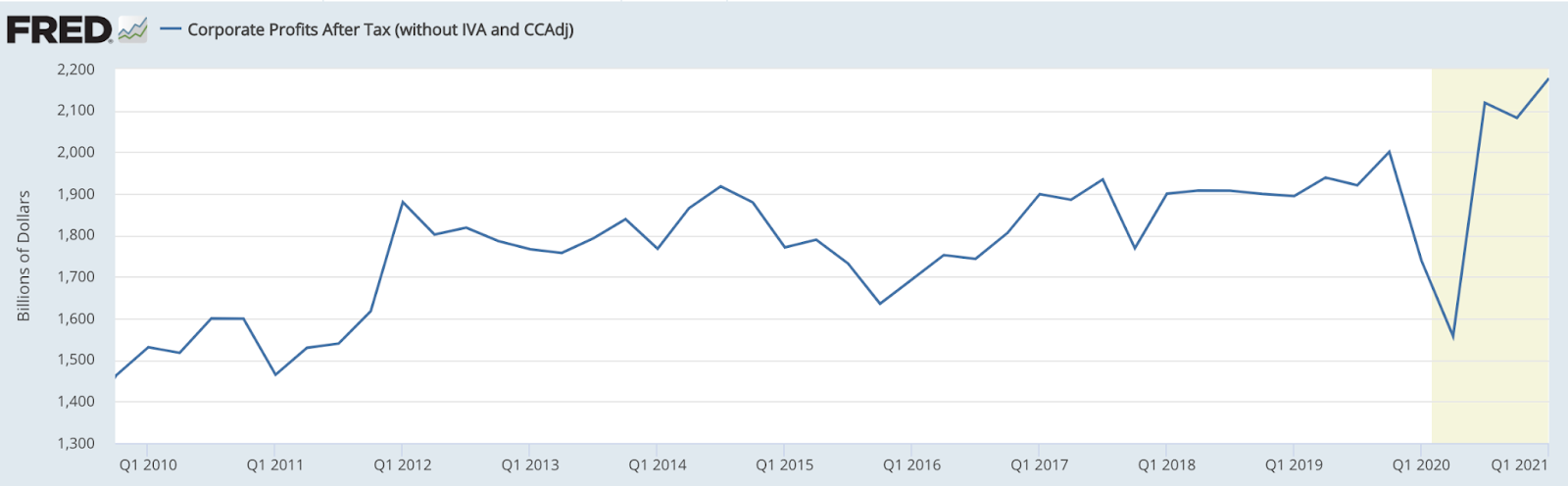

Related to the above, corporate profits are correlated with job growth and are a good measure of the overall strength of the economy. A rising level of corporate profits generally indicates that companies are growing and hiring more employees (with some exceptions). Below is a chart of corporate profits after tax for U.S. companies since the 2008-09 recession. While profits took a temporary dip due to COVID, they have bounced back strongly as the economy has recovered.

Source: FRED Economic Data, U.S. Bureau of Economic Analysis

- Work-From-Home Trend

Job growth results in a greater need for office space to accommodate employees. However, if employees being added to an organization are working from home, then the need for office space may not be one-for-one (rather, demand for office space may grow at some percentage of the employees added). Going forward, the extent to which work-from-home is universally adopted across office-using industries will impact demand for office space.

Supply/Vacancy

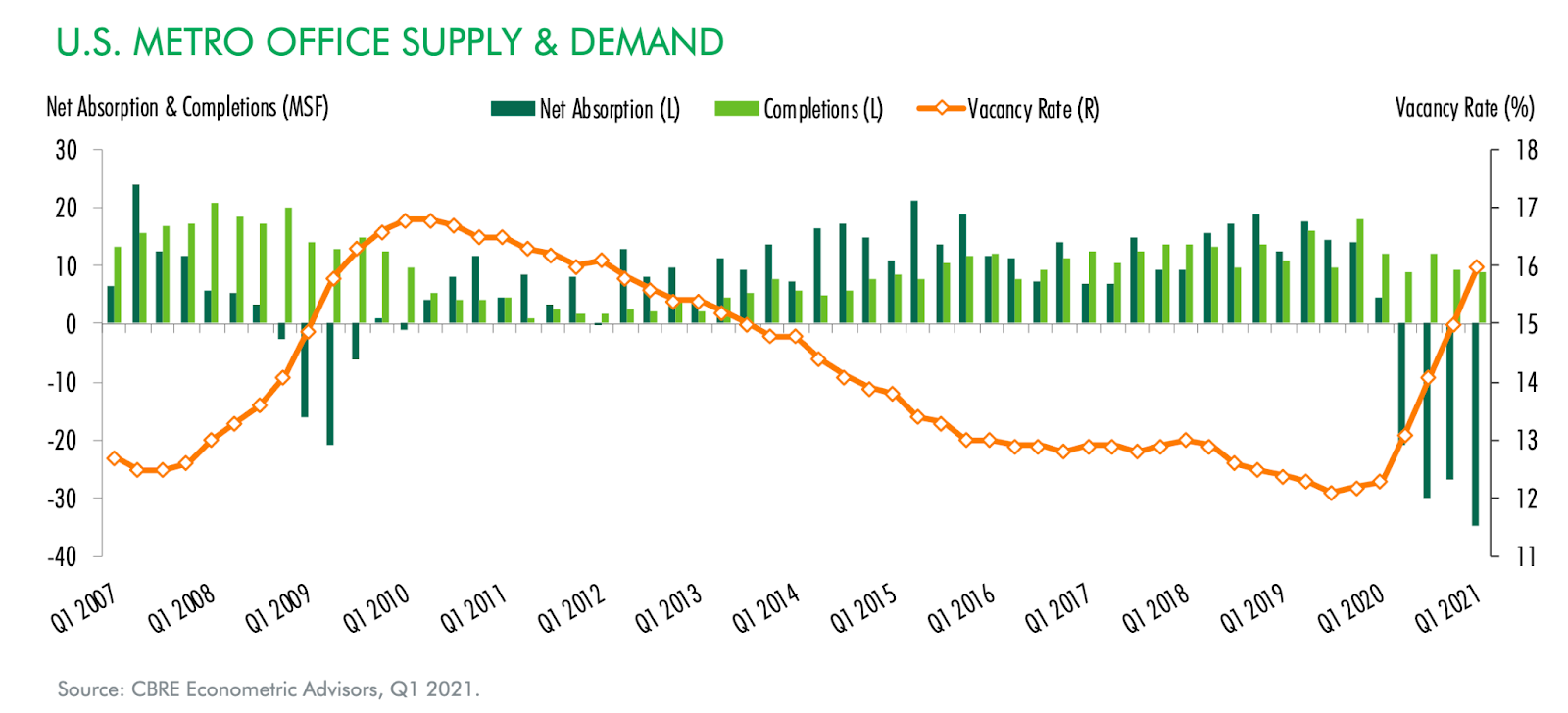

One piece of good news is that supply in the office market has been relatively measured since the 2008-09 recession. Given that the economics of office real estate are not all that favorable relative to other commercial real estate sectors, in aggregate, developers have not created too much stock during the last cycle. The below chart from CBRE shows U.S. office completions (light green bars) compared to net absorption (dark green bars) going back to 2007. Note that since 2016, completions and net absorption have been relatively inline with one another, at least until COVID. Thus, over this period the office vacancy rate (orange line) drifted lower, bottoming in the low-double-digit range.

Since COVID, completions have remained steady (developments already in progress coming online) while net absorption has fallen off a cliff (vacancies have significantly outpaced leasing). As a result, the office vacancy rate has shot up to the mid-teens range, and is nearly back to the peak vacancy rate post-2008-09 recession.

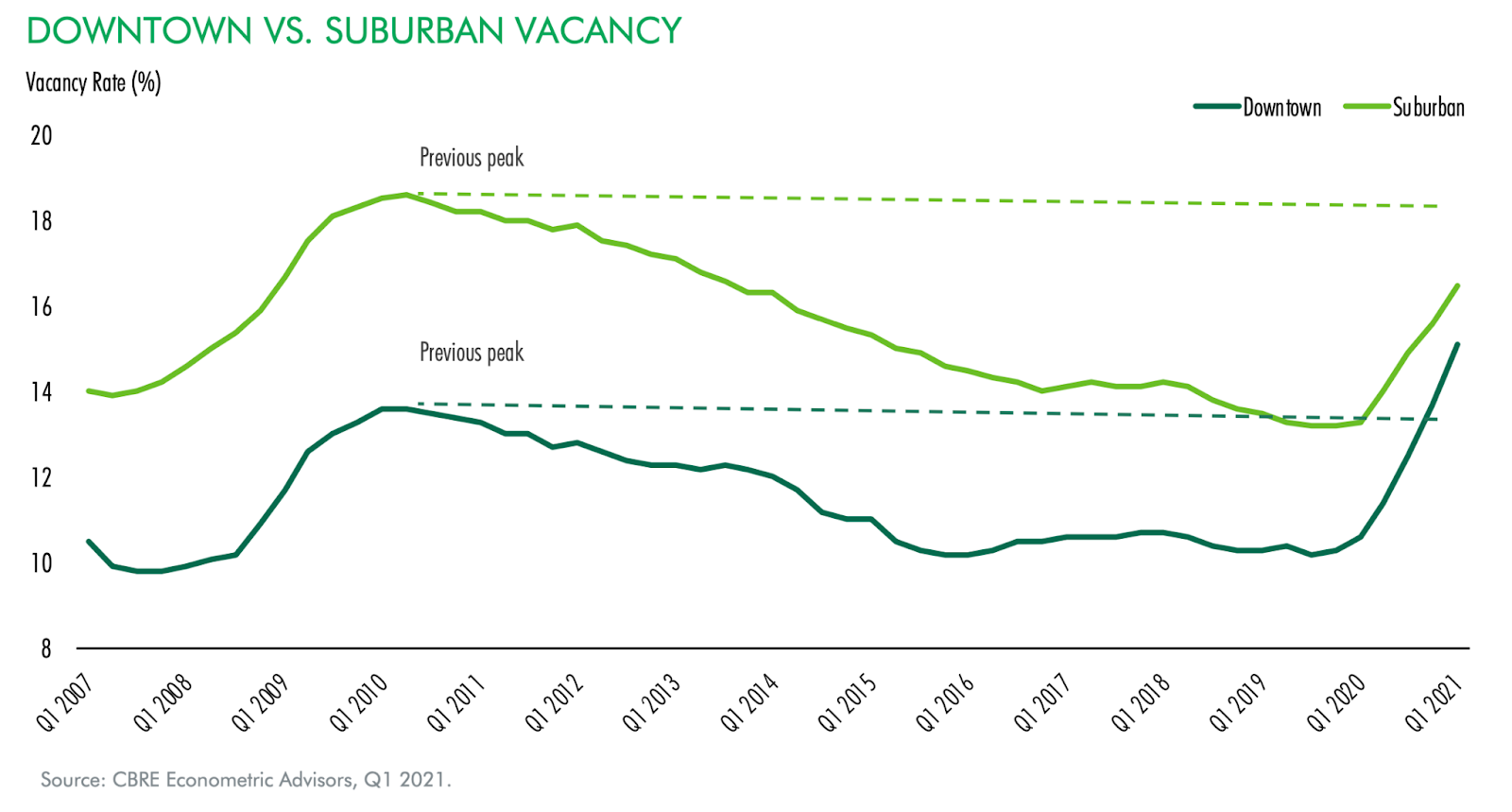

Another interesting trend is the dichotomy between central business district (CBD) and suburban office. Similar to other real estate sectors, CBD office properties have fared worse post-COVID given the temporary outmigration from dense, urban areas. It remains to be seen how sticky this trend will be, though it’s very possible that it will continue for some time. Below is a chart from CBRE that shows CBD and suburban office vacancy rates since 2007. Though suburban office started from a point of higher vacancy, through Q1 2021 suburban has outperformed CBD in terms of the rise in vacancy rate. CBD vacancy is already above its prior peak in 2010, and is fast approaching the current suburban vacancy rate.

Rent Growth

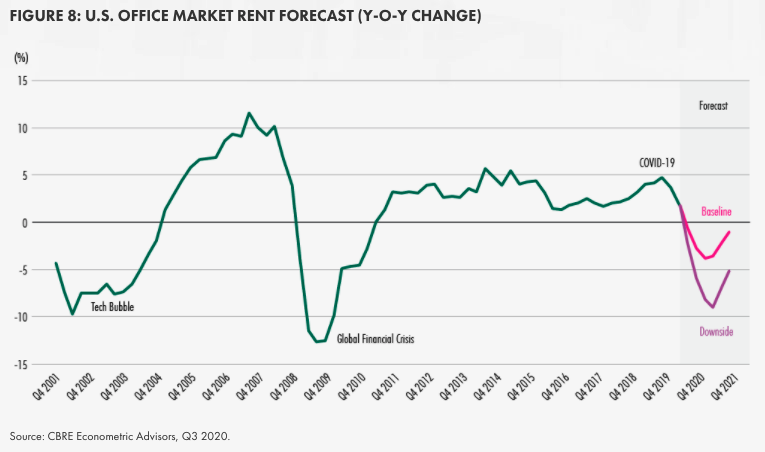

As expected, given the fundamental imbalance between supply and demand, office rent growth has decelerated and turned negative (average asking rents declined 1.6% in Q1 2021, per the CBRE Q1 2021 Office Report). After concessions, the net effective rent (not reported) is likely much worse than this. The below chart from CBRE shows U.S. office market rent growth through Q3 2020, with a forecast of rent growth in future quarters. At this point it is known that rent growth has turned negative, though the open question is how negative will things go, compared to previous recessions.

Conclusion

Historically a popular sector to allocate time and capital, office real estate was significantly disrupted by COVID, given the quick pivot to work-from-home that many employees and organizations adopted overnight. However, in-person collaboration is a key missing ingredient in a work-from-home environment, prompting leaders of many organizations to push for employees to return to the office. Not all organizations have adopted this approach, with many realizing that things function as efficiently if not more so with employees working from home. Regardless, the way we work is likely to look very different in five years than it did five years ago, and this has major implications for office real estate.

As a result of COVID, demand for office space has fallen off a cliff — vacancy rates have moved higher and rent growth has turned negative. The near-term outlook for the sector is negative, given that rent growth probably has further to fall in order for the market to reach equilibrium (supply/demand to come into balance). The medium-term outlook for the sector is less clear, given the uncertainty of the future of work. Uncertainty typically leads to opportunity, and the uncertainty created by the evolving nature of office real estate will likely be no exception.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.