Executive Summary / “TLDR”

Hotels are a unique real estate type because of their “nightly leases”, which is different from all other sectors with longer leases. Because they have nightly leases, hotels react much more quickly to changes in the broader economy than types of real estate. Hotels are also more operationally intensive than other real estate sectors, requiring more labor, marketing, and management costs, resulting in greater operating leverage and lower margins. All of this adds up to much greater swings in cash flow than that of other sectors, depending on the health of the overall economy.

No sector was put to a greater test during the COVID-19 pandemic than hotels. Travel and lodging demand dropped to virtually zero overnight, before slowly recovering at different speeds, depending on geographic area and hotel type. For many hotels, EBITDA turned negative for a few quarters, before bouncing back to positive. Many hotel owners received temporary forbearance from their lenders, given the extenuating circumstance, in order to delay debt interest payments for a period of time. As of this writing, in July 2021, the hotel sector has significantly recovered from the bottom, but still has more ground to make up in order to get back to 2019 levels.

The longer-term impact of the pandemic on the hotel sector remains to be seen, but odds are good that business travel will be modestly reduced on a permanent basis. Companies and employees have become more comfortable with using technology to conduct virtual meetings and events during the pandemic. While not a perfect substitute, virtual meetings will likely serve as a replacement for the more marginal business travel in the past. Leisure travel will likely be unaffected, or perhaps even increase post-pandemic, given the cultural shift towards working remotely on a regular basis. The hotel industry is likely to evolve toward a new type of traveler — one that prefers larger room sizes for multiple uses, free and fast internet service, a touchless check-in process, and other health-focused amenities. While things may look different in the hotel industry in five years than they do today, one thing will always stay the same: hotels will continue to be a “boom and bust” sector within real estate.

Quick Note: Think of this blog post as part hotel real estate primer and part hotel sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Categories of Hotels

Hotels are placed into various buckets for comparison purposes. Two main ones are 1) Chain Scale and 2) Full-Service / Select-Service. Chain scale is a segmentation system established by hotel data-provider, STR, that categorizes hotels by average daily rate (ADR). The chain scale categories are listed in the below chart:

| Chain Scale | Level of service | Example hotel brands | Approx. ADR |

| Luxury | Highest level of service & amenities | Four Seasons, W Hotels | $330 |

| Upper Upscale | High level of service & amenities | Marriott, Hilton, Hyatt, Westin | $190 |

| Upscale | High level of service, some amenities | Courtyard, DoubleTree, aLoft | $145 |

| Upper Midscale | Medium service, basic amenities | Holiday Inn, Hampton Inn | $115 |

| Midscale | Basic service, few amenities | Best Western, Ramada | $90 |

| Economy | Basic service, limited amenities | Days Inn, Super 8 | $65 |

| Independent | Varies (defined as separate category, since not branded hotels) | Various, fragmented market | Various |

Hotels can also be broken down into Full-Service and Select-Service. Full-service hotels generally have one or multiple bar/restaurants at the hotel, amenities like pools and spas, and large meeting and group areas. Select-service hotels are generally smaller and do not have all of the extras. Select-service hotels tend to operate at higher margins, since they have less exposure to lower-margin bar/restaurant and other ancillary revenue streams.

Defining RevPAR

The hotel industry has a number of industry-specific key terms, one of which is RevPAR. RevPAR stands for “revenue per available room”. RevPAR is derived by multiplying the average hotel occupancy by the average daily rate (ADR):

RevPAR = Occupancy x ADR

To illustrate with an example, suppose that a hotel has 100 rooms and an average annual occupancy of 60%. Suppose that the hotel’s ADR is $150. Then the hotel’s RevPAR is $90, or 60% occupancy x $150 ADR. Conceptually, a $90 RevPAR simply means that the hotel earns $90 per available room (total rooms at the hotel). Now, suppose the hotel has 100 rooms that are available 365 days per year. That’s a total of 36,500 room nights per year (100 x 365). In order to calculate annual room revenue for the hotel, we simply take the 36,500 room nights and multiply by the $90 RevPAR in order to get total annual room revenue of approximately $3.29 million.

RevPAR is effectively a metric that combines both occupancy and ADR into one number, in order to compare hotels against one another on an apples-to-apples basis (this is because occupancy and ADR can vary widely depending on the type of hotel and management strategy.

A few companies compile RevPAR data for hotels (among other data points), the most popular of which is STR, which is owned by CoStar Group. STR publishes “STAR reports” by hotel market and hotel segment on a weekly/monthly basis, which are frequently cited and utilized by industry participants.

Seasonality

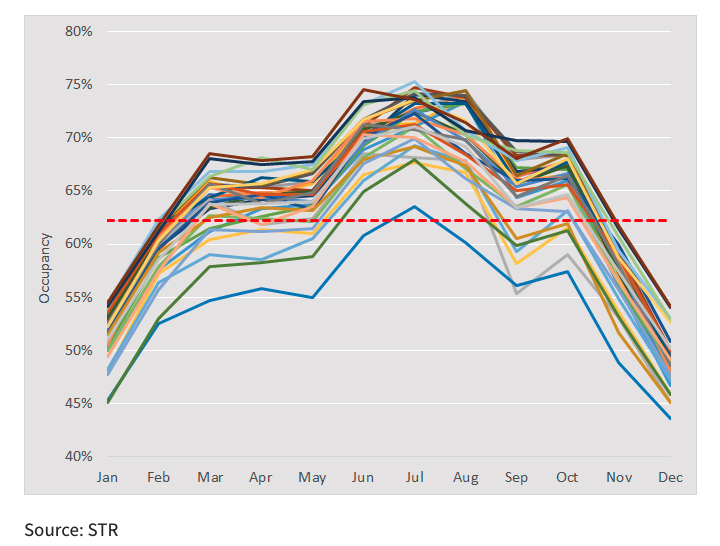

Since hotels have short-term leases that change each day depending on travel demand, seasonality is a much bigger consideration than for other property types. On average, U.S. hotel occupancy tends to peak in the summer months (June – August) and trough in the winter months (December – January), as people are traveling less (both business and leisure travel). Below is a chart showing average U.S. hotel occupancy by month over a 30-year period from 1987-2019:

Source: STR data, via hotelinvestmentstrategies.com

Note that this is an overall average, but is definitely not the pattern for all hotels. For example, warm-weather resort or ski-resort hotels experience peak occupancy during the winter months (January – March), with the off-season in the summer and shoulder seasons in the spring/fall.

Because of this monthly seasonality issue, hotel cash flows are typically not even throughout the year, but rather vary widely season-to-season or month-to-month. Thus, many hotels have a “seasonality reserve” put in place by the hotel’s lender, where the hotel accrues excess cash flow into an account during the peak demand months, and then during the low demand months draws down that account to cover the loan interest payments.

EBITDA Margins

Hotels have much lower margins than that of other property types. For hotels, the industry typically uses “EBITDA margin” vs. “NOI margin”, since hotels are more of an operating business than other types of real estate. The primary reasons that hotels operate at lower margins include:

- Hotels are more labor intensive than other real estate

- Hotels are typically “branded” with flags

- Hotels often incorporate lower-margin, non-room revenue sources

Since hotels are more labor intensive than other property types, they require both extra payroll to employ a staff and management fees for a third-party management company. Also, hotels are often branded with flags, such as Hilton or Marriott, resulting in added franchise and marketing fees. Lastly, full-service hotels incorporate non-room revenue like restaurants and spas, which operate at lower margins than room revenue.

Because hotels have lower margins than other property types, and not all of the expenses are variable costs (some are fixed, which adds operating leverage), EBITDA for hotels is much more sensitive to changes in top-line revenue. On top of that, hotel revenue is more volatile than other property types due daily leases and seasonality, discussed above. This means that hotels greatly outperform other property types in good times and greatly underperform in bad times.

Capital Expenditures

Capital expenditures or “capex” is another defining feature of the hotel sector. Simply put, hotels receive a lot of wear and tear as guests come in and out of the hotel on a nightly basis. The furniture, fixtures, and equipment (FF&E) in the hotel have a shorter useful life than most other real estate components, around 5-10 years. Also, unlike some other real estate types, the guest experience is paramount in the hospitality business, which means that hotels are more liberal when it comes to spending capex.

In total, hotel capex represents a big percentage of the net operating income or EBITDA, often as high as 40% of NOI, depending on the hotel type. This is a much higher percentage of NOI than that of other core sectors, with the exception of office, which is also high. This means that with hotels, there is an even greater focus on understanding the building net cash flow, which factors in capex.

Note that the industry standard for hotel underwriting is to use an FF&E or capex reserve of 3%-5% of revenue, which works out to about 15% of NOI. This undershoots the actual capex by a wide margin. This is because the capex used in underwriting is often defined as maintenance capex, which accounts for interim upkeep but doesn’t account for large-scale renovation programs that happen every 10 years or so. In standard underwriting this is often considered to be the “next owner’s problem”, and is sometimes factored into the sale price at the end of the investment period.

To be continued in Hotels (Part 2)…

Given that the hotel sector has a lot of ground to cover, we broke this post into two parts. In the second part, we’ll review the various ways in which the hotel sector has been impacted by COVID, provide an overview of the fundamental demand drivers for the sector, and conclude with our outlook for the sector.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.