Note: If you have not already read Part 1 of the Hotel Sector Series, you may want to start there. Part 1 provides a basic overview of hotel real estate, including categories of hotels, important industry terms, and a discussion of hotel seasonality, EBITDA margins, and capex. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Impact of COVID on Hotels

There is no sector that was more immediately impacted by the COVID-19 pandemic than hotels, given that travel nearly came to a standstill in March 2020. Hotel occupancy rates fell off a cliff and EBITDA turned sharply lower, in some cases negative. That said, as the economy has reopened and travel has resumed, hotels have also been the fastest sector to rebound.

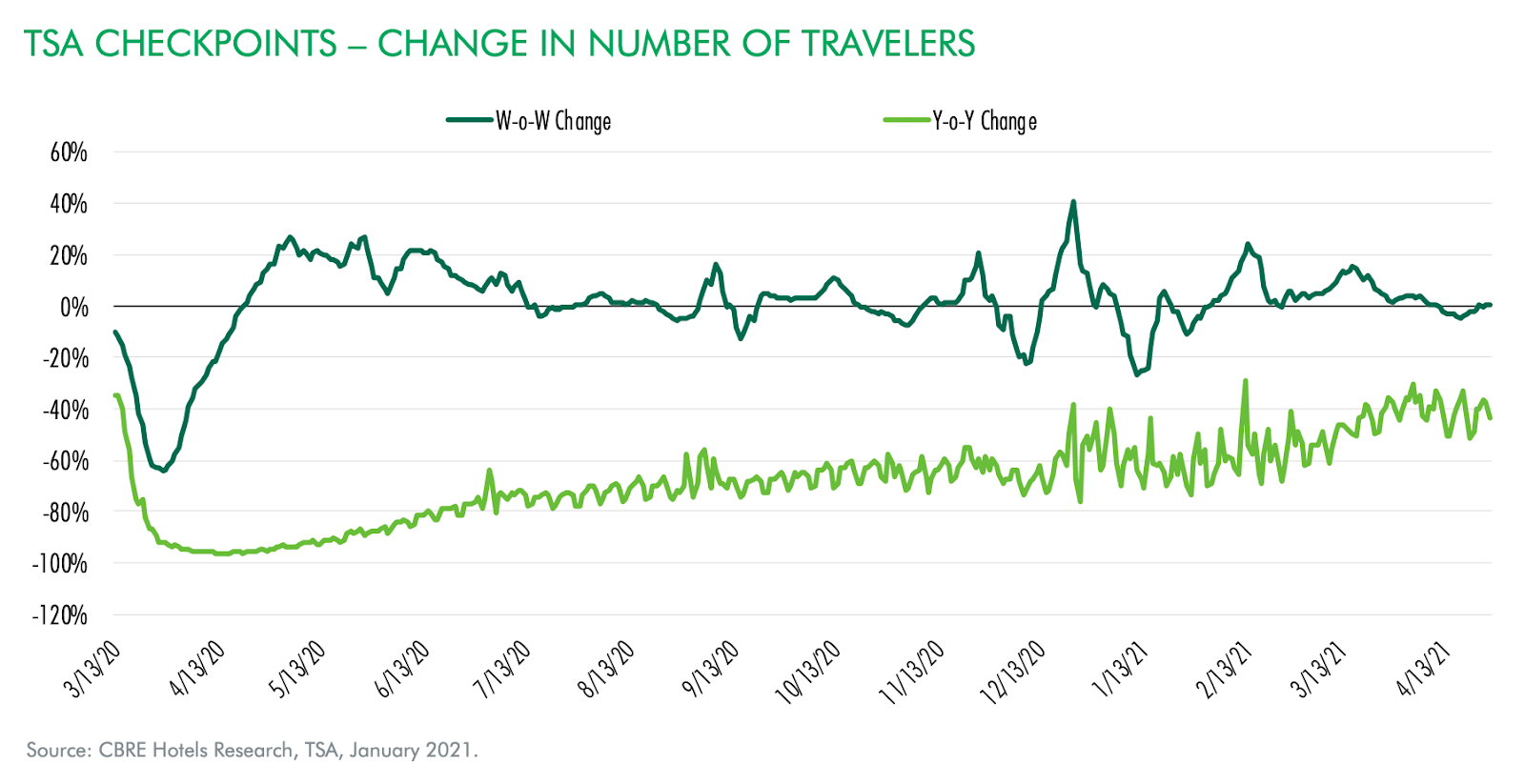

Below is a chart showing the number of travelers passing through TSA checkpoints, from March 2020 to April 2021. After a nearly 100% falloff in travel, things climbed back to a level down 40% from the pre-COVID period as of April 2021 (as of June 2021, TSA traffic is only down around 20%).

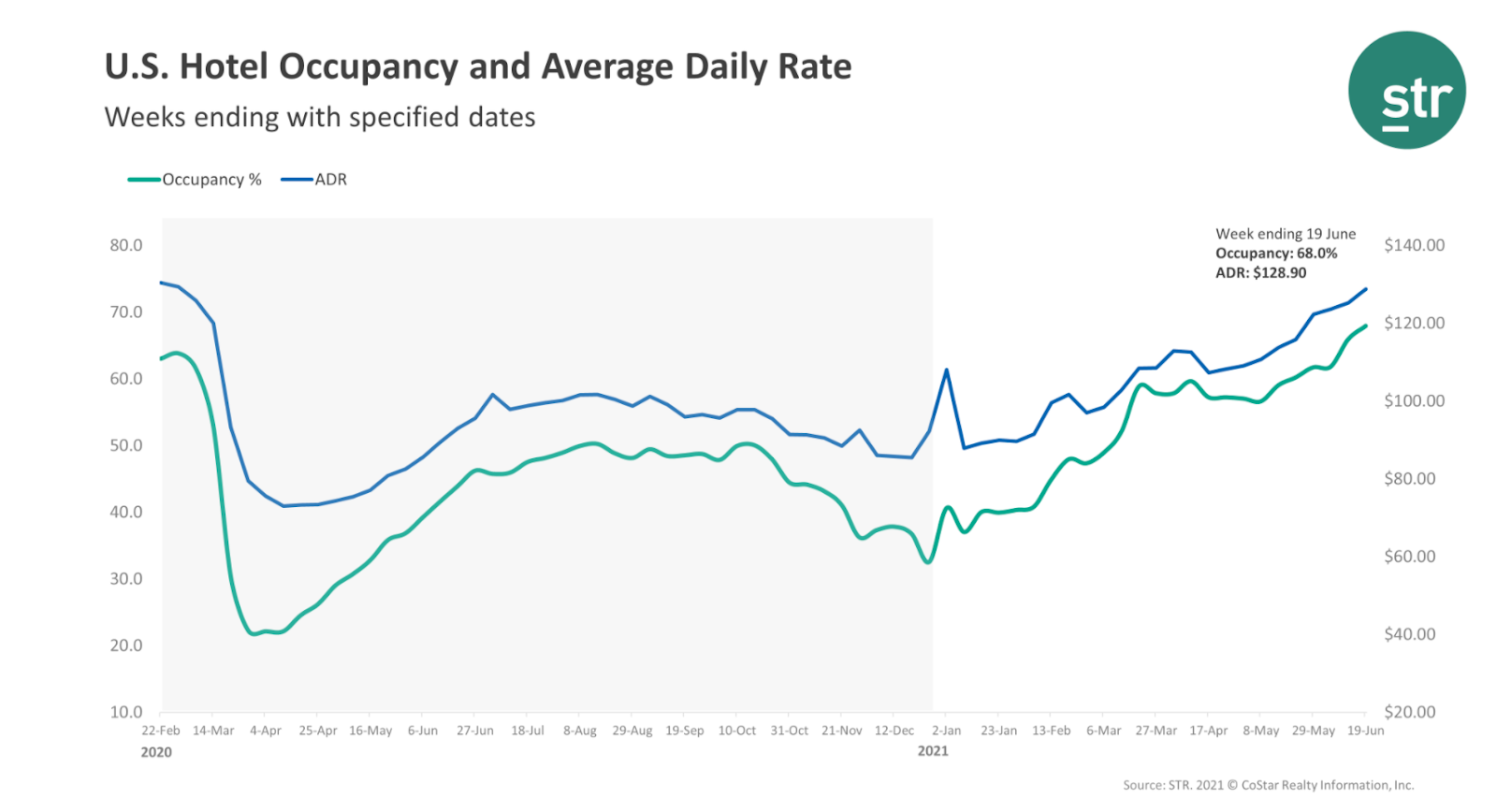

Hotel occupancy rates and ADR followed a similar trajectory, as illustrated by the below chart showing average U.S. hotel occupancy and ADR since the beginning of the pandemic. While it would appear from the chart that occupancy and ADR levels are back to pre-COVID levels, keep in mind that the data points are not comparable, since February is a low-point seasonally while June is a high point. That said, the industry has made up significant ground since the lows at the onset of the pandemic.

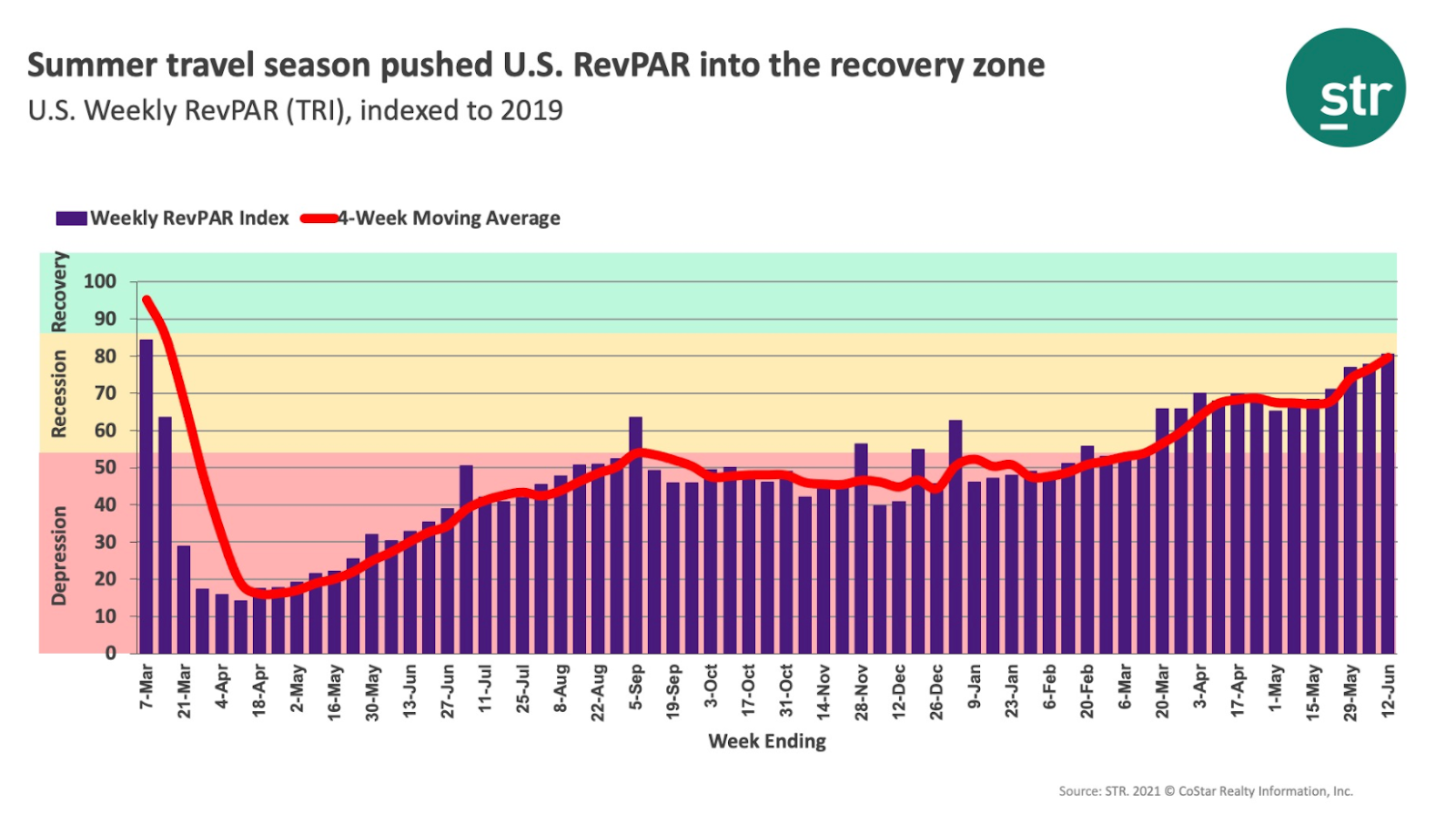

Taking occupancy and ADR together, RevPAR has unsurprisingly followed a similar path, dipping into a depression-level territory before bouncing back to a level in June 2021 that is near the recovery zone, per STR.

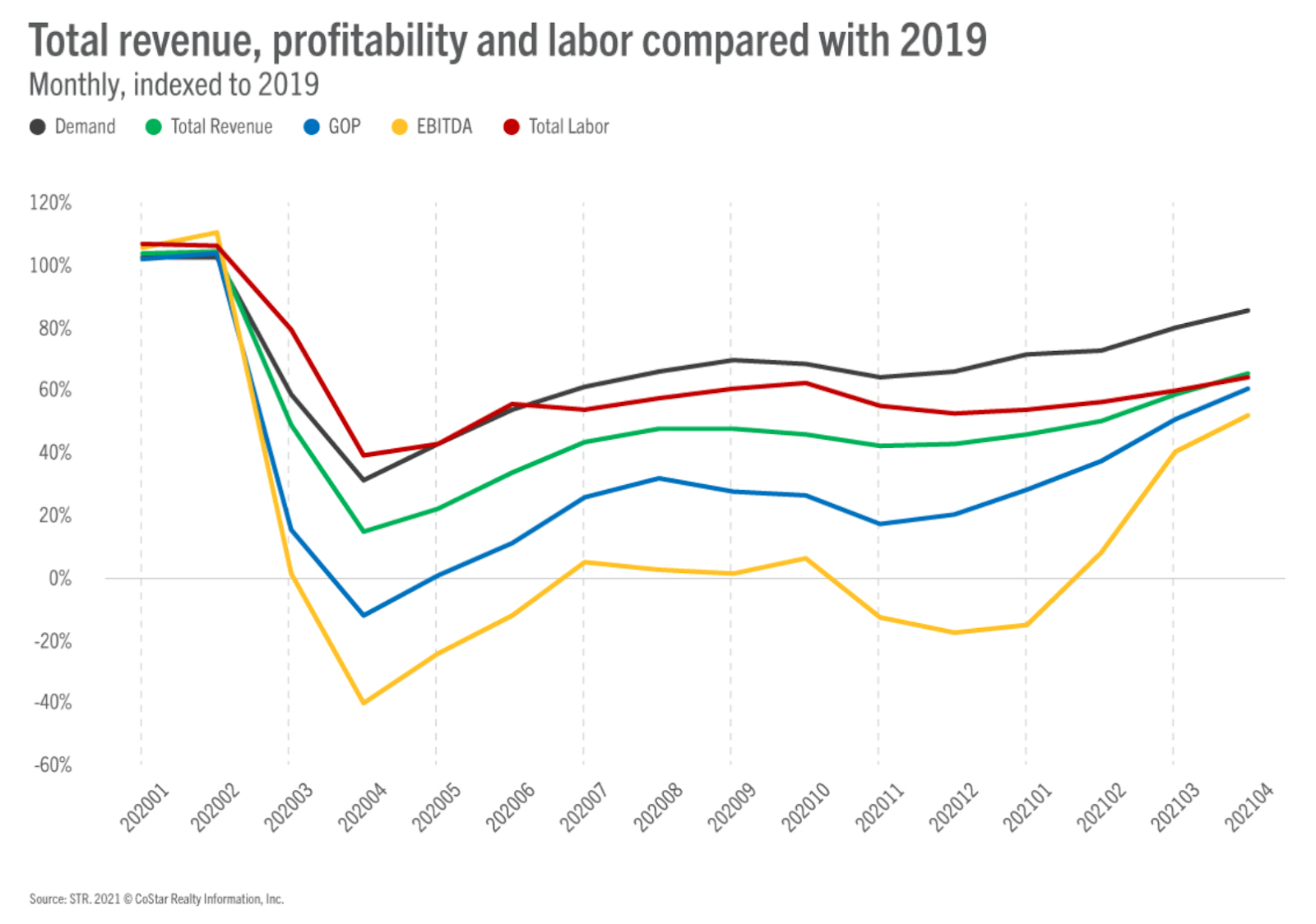

In terms of how this has affected hotel revenue and profitability, below is a chart from STR comparing hotel revenue and profitability to pre-pandemic numbers. On average, as of June 2021 revenue is at around 60% of pre-pandemic numbers (green line, below), while EBITDA is at around 40% of pre-pandemic numbers (yellow line, below). These metrics are both down significantly, but the good news is that EBITDA is positive after being negative for much of the pandemic.

Regardless of when the hotel industry fully recovers, there are likely to be some lasting changes in the industry as a result of the pandemic. Those emerging industry trends include the following:

- Reversal of pre-COVID trend toward smaller room sizes (average of 1,600 square feet in 2010 compared to 1,100 square feet in 2019, per JLL); going forward, larger hotel rooms will have spaces to work, eat, and exercise

- More focus on extended-stay travelers (i.e. compete with Airbnb for travelers working remotely in a different location)

- Touchless check-in process and fast/free internet connection

- More focus on health and wellness amenities (air filtration, outdoor spaces, fitness space)

- Conference rooms on-demand, in order to accommodate meeting space for organizations utilizing less office space going forward

- Technology solutions to accommodate hybrid conferences, i.e. in-person conference amenities paired with technology to enable high-quality virtual viewings

- More focus on sustainability initiatives, including solar panels, digitally-controlled energy management, and motion sensors for in-room lighting and HVAC

Hotel Supply & Demand

Historically hotel demand has been highly correlated with GDP. Hotel demand has grown around 2% annually on average, per Cushman & Wakefield, moving roughly in sync with GDP. There are several demand segments that make up total hotel demand:

- Business Transient (one-off business trips)

- Group Travel (further divided into “business group” and other gatherings classified as “SMERF”: Social, Military, Education, Religious, Fraternal)

- Leisure (vacation, events, trips to visit family)

International travel is another important demand driver for hotels, since international visitors tend to stay for longer periods of time. International travel makes up roughly 20% of U.S. hotel demand.

In terms of how these segments are likely to be impacted by COVID, leisure is least likely to be impacted, while business group travel is mostly likely to be impacted permanently. Coming out of the pandemic, leisure travel picked up first, as individuals have prioritized visiting family and taking vacations. Business travel has been slower to recover, as companies have found other means to connect with customers and have been reluctant to schedule corporate events.

Longer-term, the business transient segment, or one-off trips to visit current and prospective customers, is likely to mostly return to pre-pandemic levels. Despite virtual meetings becoming much more of a mainstay during the pandemic, it is still important to meet face-to-face to form relationships, particularly for prospective customers. Business group travel, however, faces more headwinds post pandemic, due to a culture that has developed around hybrid conferences and group events.

One positive offset is a potential new segment created by the pandemic, or “work-from-anywhere travel”. This is where employees set up to work from anywhere move to another location while working for an extended period of time, even without a specific business purpose to do so. It is likely that Airbnb or similar platforms will pick up a large percentage of this new segment demand, however, the hotel industry will likely evolve to meet this new segment.

Net-net, longer-term demand for hotels is likely to be modestly lower post-pandemic, mainly driven by reduced demand from the business segment, potentially offset by increased demand from leisure or the newly created “work-from-anywhere” segment.

In terms of supply, hotel supply growth has been inline or slightly below demand growth, averaging 1.7% over the 20 years leading up to COVID, per Cushman & Wakefield. Occupancy has been relatively steady over this period, with ADR and RevPAR averaging around 3% annual growth. The hotel industry experiences booms and busts based on demand variability, not supply growth, which has been steady over time.

Airbnb as a Competitor to Hotels

Founded in 2008, Airbnb started out as a site where hosts could rent out extra rooms or unused space to guests that were in town for an event. The site grew very rapidly and around 2015-2016 started to be viewed as a modest competitive threat for hotels. One 2018 research study found that the presence of Airbnb in major cities reduced hotel revenues by 1.5% and hotel profits by nearly 4%. A lot of this comes from Airbnb acting as “flex supply” when major events cause lodging demand to spike, thus capping the ability for hotels to raise prices. Another study found that the presence of Airbnb caused hotel RevPAR to decrease by around 2% during the period from 2008 to 2017.

Today, Airbnb has 4 million hosts on the site and makes up less than 4% of global lodging market share, though higher than that in the U.S. (average estimate is around 5% share in the U.S.). Airbnb has also outperformed hotels through the pandemic, given Airbnb’s skew towards leisure travelers and availability of listings of entire houses, which have been more desirable given social distancing. Airbnb has also been used by many as a platform to book for longer periods of time while living and working away from home. In the first quarter of 2021, Airbnb bookings were down 20% from 2019, but gross booking value was actually up 3% over 2019, given a higher ADR resulting from more frequent renting of entire homes.

Airbnb has already proven to be an effective source of flex supply during high demand periods, but coming out of the pandemic the company is poised to accelerate its growth in hosts and bookings. Odds are good that Airbnb’s impact on hotels will be greater post-pandemic, as travel demand shifts away from business travel and toward leisure and extended-stay travel.

Conclusion

Hotels have never been a sector for risk-averse investors, given their big cyclical swings alongside the economy. The COVID-19 pandemic proved this once again, to an even greater extent than in prior cycles. That said, the industry has bounced back quickly and is on the road to full recovery as of mid-2021. The travel industry is gearing up for the mother of all booms in the U.S. as people are anxious to travel again after a long hiatus.

The near-term outlook for hotels is positive, given the likely acceleration of cash flows off of depressed levels. The medium-to-long-term outlook is less clear, however, given that some business travel will likely be permanently curbed. In addition, Airbnb has proven to be a formidable competitor for the industry, providing excess flex supply and catering to the interests of the millennial traveler. There’s no doubt that the hotel industry will evolve to meet the shift in demand brought about by COVID, though that process could also add costs and modestly reduce investment returns in the industry going forward.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.