Executive Summary / “TLDR”

Retail is a fairly diverse sector, encompassing everything from small neighborhood shopping centers to large super-regional malls. This report applies to all types of retail, but is geared toward shopping centers, which make up around 80% of all retail space in the U.S.

In the last several years, online shopping, or e-commerce, has become a dominant force, gaining traction with all types of consumers. The e-commerce trend accelerated during the COVID-19 pandemic, as many consumers were forced to stay at home and order goods online vs. shopping in stores. As the COVID pandemic abates and consumers get back to everyday life, in-store shopping will surely bounce back, but e-commerce will continue to grow more quickly and take more share of the overall retail sales pie. Since retailers understand this trend, and cater to the preferences of the consumer, they will continue to tilt their omnichannel strategies toward e-commerce, at the expense of brick and mortar stores. Over time, this evolution will likely result in lackluster demand for retail space.

On the supply side, there is too much existing stock of retail space in the U.S., relative to the population size. Weak demand paired with oversupply has weighed on the retail sector over the last several years, resulting in anemic occupancy and rent growth. This trend is unlikely to change going forward, particularly given that coming out of COVID, consumer preferences have shifted toward convenience vs. experiential retail. Before the pandemic, investing in the in-store shopping experience was retailers’ best defense against e-commerce, but even that strategy will likely be less effective going forward.

Like in any sector that is out of favor for an extended period of time, there will be opportunities to uncover value in the retail sector. However, with the secular headwinds unlikely to abate, investors need to be careful about catching a falling knife.

Quick Note: Think of this blog post as part retail real estate primer and part retail sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Types of Retail Centers

There are a number of different types of retail centers, with each serving a slightly different purpose. Retail centers can be broadly divided into two groups, 1) shopping centers and 2) regional malls. The primary differences between shopping centers and malls are that malls are enclosed, have a larger footprint, and serve a larger trade area. In contrast, shopping centers are smaller and more convenience-oriented. Below is a chart that details the main types of retail centers in the U.S.

| Retail Center Type | Approx. % of all retail | Description |

| Neighborhood Center | 31% | Grocery-anchored with convenience-oriented tenants |

| Community Center | 25% | Larger than neighborhood center with wider trade area, mix of anchors |

| Regional Mall | 15% | Enclosed, generally merchandise or fashion-oriented offerings, anchored by department stores, movie theaters, and food courts |

| Power Center | 13% | Larger than community center with wider trade area, mostly big box stores and few small tenants |

| Strip Center | 12% | Small number of tenants, typically no anchor, narrow trade area |

| Other | 4% | Includes lifestyle centers, outlets, airport retail |

Source: ICSC

Types of Tenants

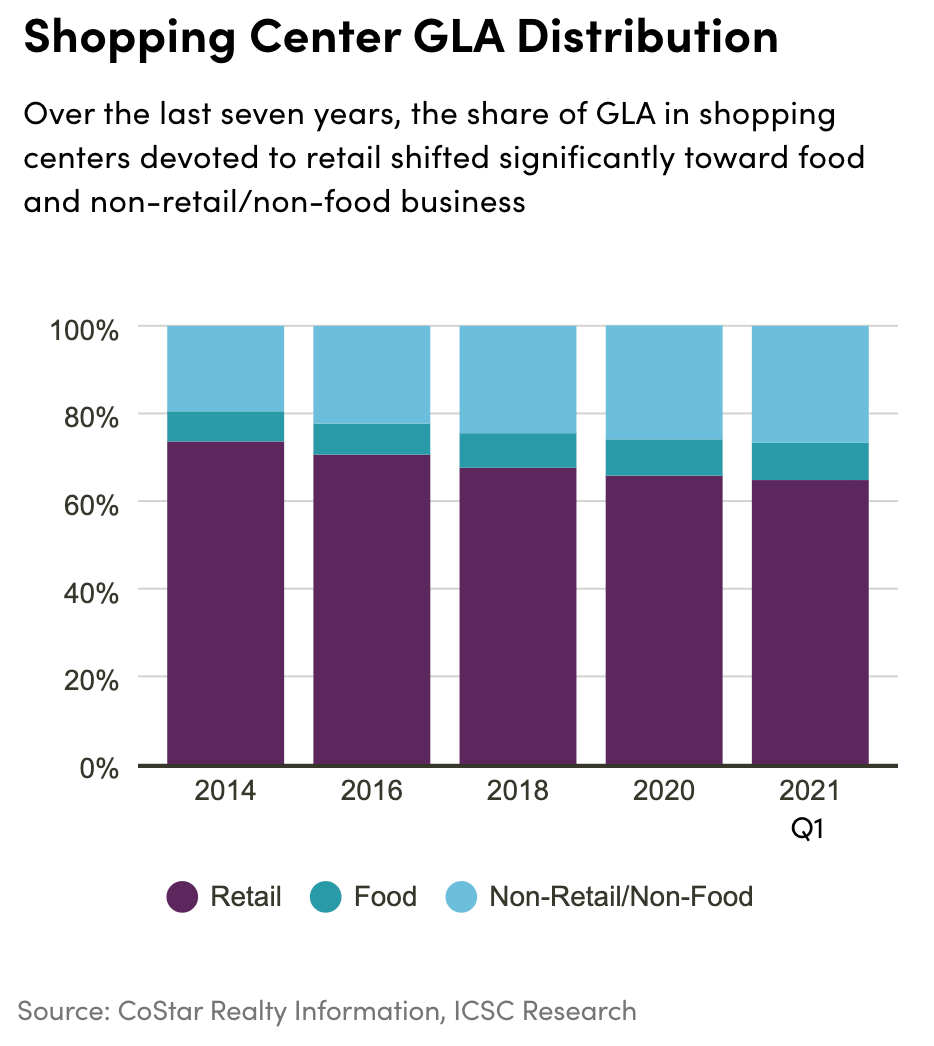

In terms of tenants, below is a list of several retail categories commonly found in shopping centers with the more common retailers listed for each category. In the last several years, as e-commerce has taken share from brick and mortar retail, there has been a shift in tenant mix away from traditional retail (general merchandise and apparel) and toward food and non-traditional retail (i.e. gyms and experiential retail). The second chart below details this shift in tenant mix over the last seven years. While this evolution toward food and non-traditional retail has been a slow process, given that leases are generally 3-5 years in length, it is a clear trend. This shift in tenant mix indicates landlords responding to the preferences of consumers.

Tenant Categories

General Merchandise Anchors: Walmart, Target

Wholesale Clubs: Costco, Sam’s Club

Grocery: Publix, Kroger, Albertsons, Giant, Trader Joe’s, Whole Foods

Off-price: T.J. Maxx, Ross, Burlington, Kohl’s, Nordstrom Rack

Big Box: Home Depot, Lowe’s, Bed Bath & Beyond, Best Buy

Fitness/Gyms: Planet Fitness, L.A. Fitness

Drug Stores: Walgreens, CVS

Pet: Petsmart, Petco

Restaurants: Starbucks, Panera, Darden Restaurants (Olive Garden, Longhorn, etc.)

Movie Theaters: Regal, AMC

Capex

Capital expenditures or “capex” is another important consideration in the retail sector. Over the years, capex has steadily risen for retail centers as landlords have been forced to redevelop and improve their centers in order to compete with the rising popularity of online shopping. Additionally, an increase in tenant bankruptcies and store closures has added to redevelopment and re-leasing costs.

Capex is formally defined as money required to maintain, repair, or lease an asset. Retail capex includes the following items:

- Tenant improvements (TIs): money paid by the landlord to a new tenant upon lease signing that covers the tenants’ costs to build-out their space.

- Leasing commissions (LCs): money paid by the landlord to a leasing broker in exchange for finding a tenant.

- Building maintenance expenses: includes ongoing maintenance and one-time replacement of certain features or equipment.

- Redevelopment costs: money invested to update or change the structure of the retail center, including dividing up vacant boxes into smaller spaces, adding alternative uses to the center, or reconfiguring the center to accommodate new tenants.

In total, capex as a percentage of NOI has risen from the mid-teens in the 2000s to more than 20% today, with development costs accounting for the majority of the increase. Even so, retail capex as a percent of NOI is still lower than that of the office and hotel sectors, which are in the 30%+ range.

Demand

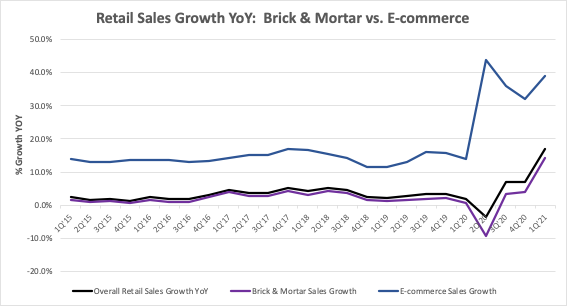

The primary driver of demand for retail real estate is demand for buying retail goods in stores. Simply put, if more people are buying goods and services in stores then there is more demand for retail space. Overall retail sales growth has been healthy since 2010, averaging more than 4% growth through 1Q 2021. However, in-store retail sales growth has averaged around 3% growth since 2010, while e-commerce growth has averaged more than 16%.

This disparity in growth further accelerated during the COVID-19 pandemic, with in-store sales growth averaging 3% during the pandemic (2Q 2020 through 1Q 2021) and e-commerce sales growth averaging 38%. The massive uptick in e-commerce sales growth will likely moderate going forward. However, the pandemic significantly disrupted the shopping habits for many, resulting in a higher propensity for consumers to buy goods online. This will ultimately lead to higher e-commerce growth rates post-COVID vs. pre-COVID. Below is a chart showing e-commerce sales growth (blue line) vs. brick and mortar sales growth (purple line), relative to overall retail sales growth (black line), going back to 2015.

Source: U.S. Census Bureau, via FRED Economic Data

The chart clearly indicates that e-commerce is growing at a pace much higher than overall retail sales growth, whereas in-store sales growth is modestly lagging. Note that e-commerce is still a small piece of the overall retail pie (13%-14% of total retail sales, as of 1Q 2021) and has room for further expansion.

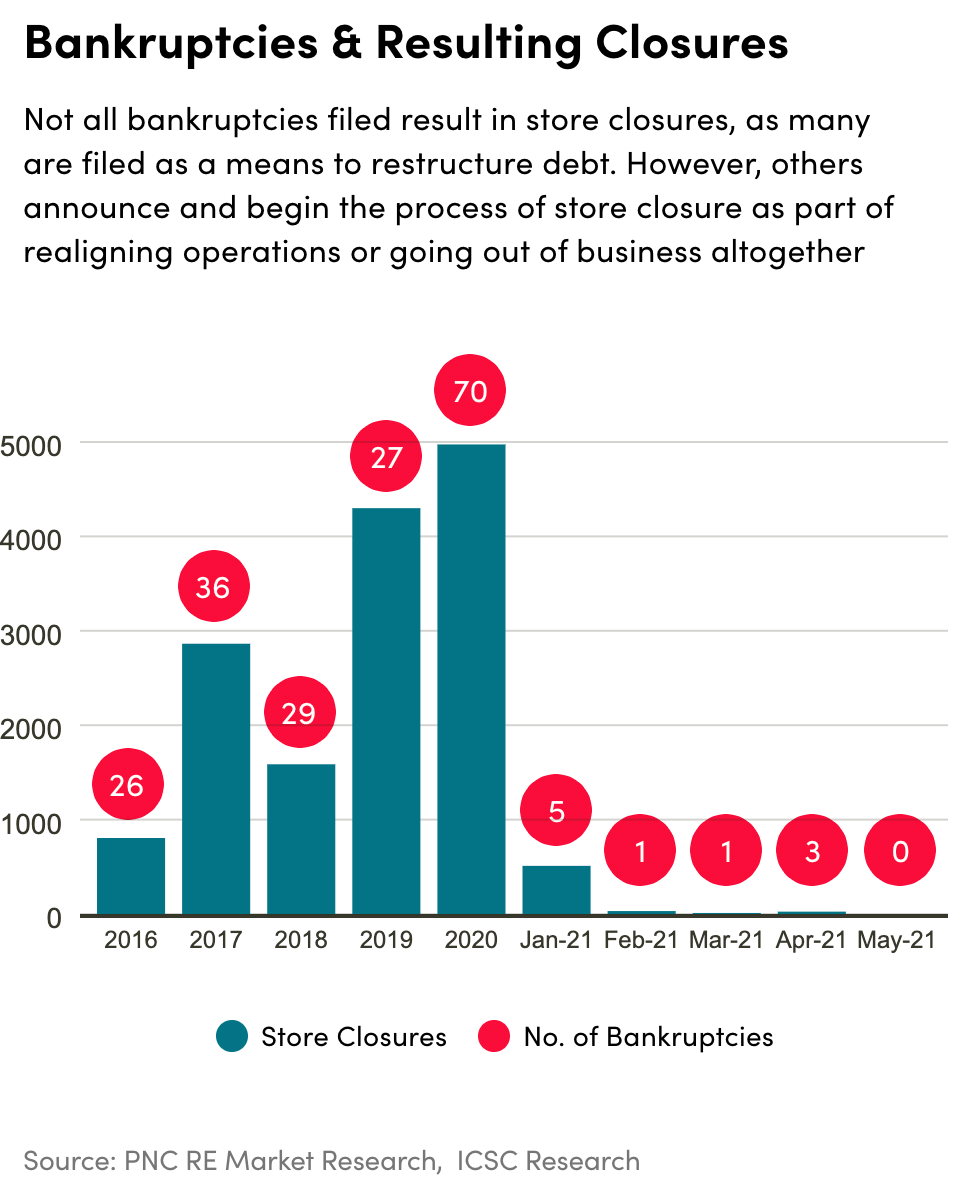

Due to stiff competition from e-commerce, the number of retail bankruptcies and store closures has accelerated in the last few years, peaking in 2020 during the pandemic. Below is a chart illustrating retail bankruptcies and store closures in recent years. Note that there have been new store openings as well to offset, but the number of store closures has significantly outpaced the number of new store openings.

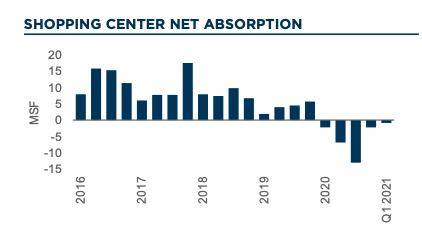

As a result, net absorption of retail space (newly leased space, less vacated space) has decelerated in the years leading up to the pandemic and turned severely negative during the pandemic. This is illustrated in the below chart from Cushman & Wakefield. Net absorption has already bounced back from the pandemic-lows, but will continue to face headwinds going forward as e-commerce becomes even more prevalent.

Source: Cushman & Wakefield

Supply

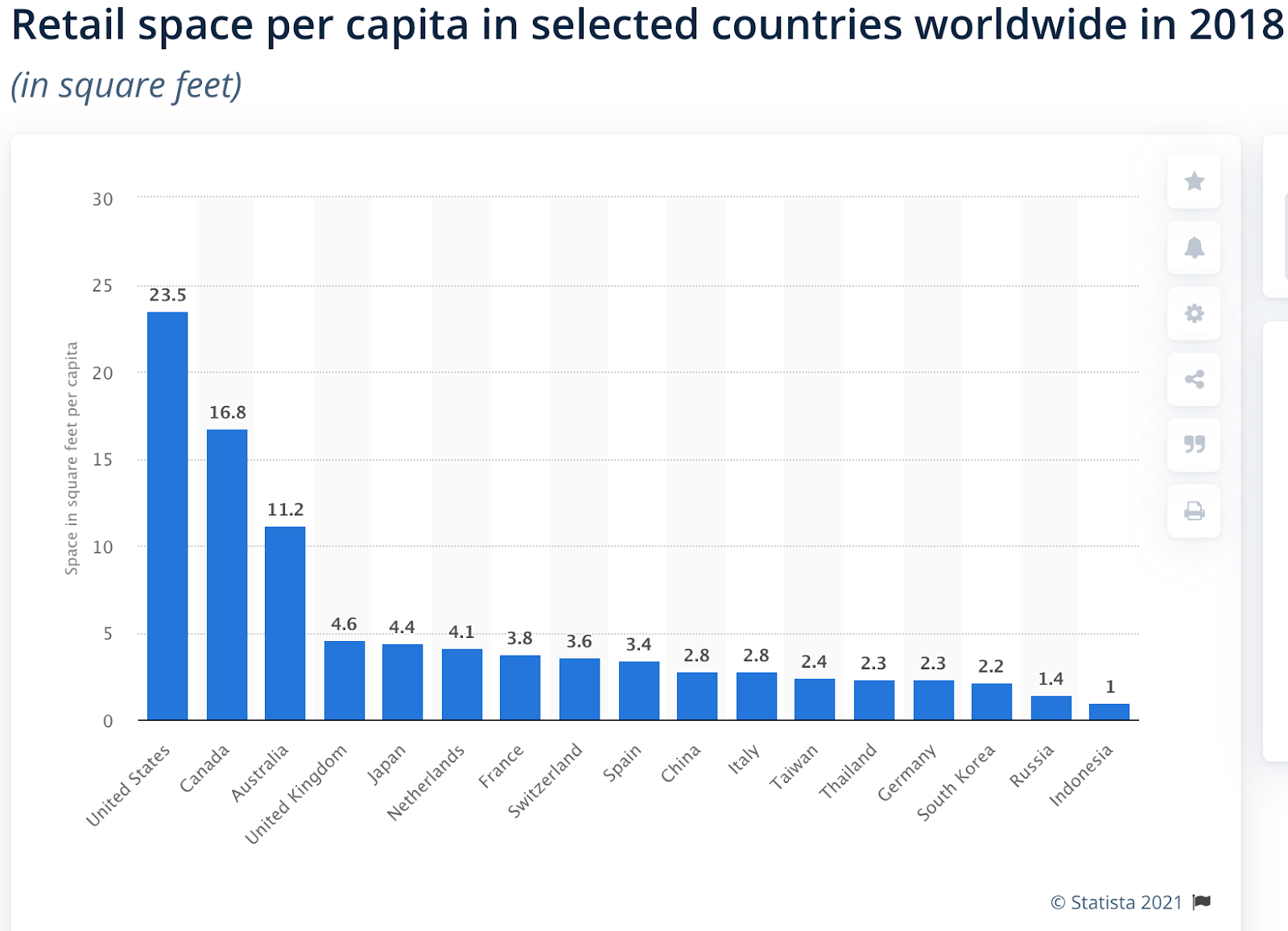

On the supply side, not much new retail space has been developed, due to the lack of demand. However, the U.S. is significantly “over-retailed” relative to other countries, due to retail space that was overbuilt over the last several decades. Below is a chart showing retail space per person in the U.S. (23 square feet per person) relative to that of other countries (16 square feet and below).

Source: Statista

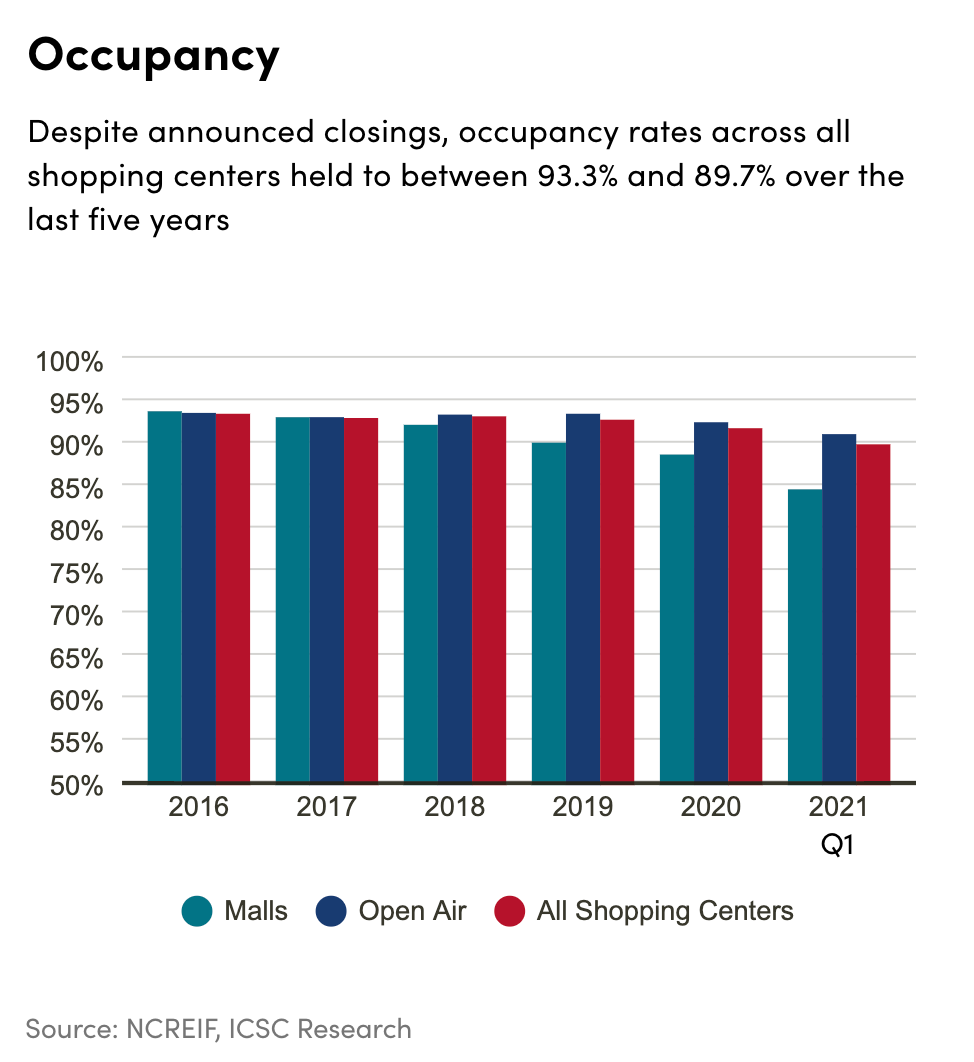

Due to tepid demand for retail space and abundant supply of space, occupancy has steadily trended lower, per the below chart. Malls have been more negatively impacted than shopping centers, but shopping centers have not been immune to this trend.

Rent growth in shopping centers has also been muted, ranging from 0%-2% growth over the last few years. Rent growth in malls has been far worse, ranging from low single-digits to materially negative for lower-quality, Class B malls. Retailers have clearly had the bargaining power vs. landlords in rent negotiations for several years now.

Retail Real Estate Post-COVID

The COVID-19 pandemic disrupted everyday life in a multitude of ways and imparted new consumer habits that will likely be sticky post-pandemic. Some of the emerging trends in the retail sector as a result of the pandemic include the following:

- More focus on convenience and ease of purchase, de-emphasis on experiential retail. Prior to the pandemic, experiential retail was viewed as the best way to compete with e-commerce, which by nature can’t offer much of an experience. Post-pandemic, consumer priorities have shifted towards convenience vs. having an engaging shopping experience.

- More focus on “click and collect”. This method of purchasing goods online and picking them up at the store was already an emerging trend pre-pandemic, but has accelerated post-pandemic. This is both convenient for consumers and also attractive for retailers, since it eliminates shipping costs.

- Brick & mortar stores as a part of the supply chain. Post-pandemic, retailers are re-examining their supply chains and figuring out ways to use retail stores as a part of their supply chains. This both creates an alternative use for retail stores and also reduces the need for additional last-mile industrial space, which is becoming expensive.

- More focus on suburban shopping centers vs. street retail. Given the population shift from cities to the suburbs, particularly during daytime business hours, street retail has seen less traffic and demand, whereas suburban shopping centers have seen a pickup in demand.

- Restaurants adopting takeout and installing drive-throughs. Restaurants were forced to adopt a takeout business during the early days of the pandemic in order to stay afloat, but this trend is becoming more permanent. Additionally, many quick service restaurants are investing in drive-throughs in order to accommodate customers that have become accustomed to picking up food with minimal contact.

Conclusion

The retail sector was already facing secular headwinds pre-COVID, but COVID has accelerated these existing trends. The near-term could be somewhat positive for the retail sector, given that pent-up demand from consumers may bolster retail sales post-pandemic. However, the longer-term outlook for the sector is decidedly negative. There’s simply too much available retail space and demand for space is not very robust. Over time, supply will likely move lower as obsolete retail space is demolished or converted to other uses, while demand will grow at a modest pace to meet supply. This process will result in a more healthy market equilibrium, though it could take years or even decades for this to unfold.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.