Executive Summary / “TLDR”

The net lease sector is defined by its lease structure as opposed to its property type, like most other sectors. The net lease sector encompasses a mix of property types, including office, industrial, and retail properties. The common feature among all of these properties is that the tenant is subject to a net lease. The tenant, typically a sole occupant of the building, pays a “net rent” to the landlord and is responsible for covering the building’s operating expenses.

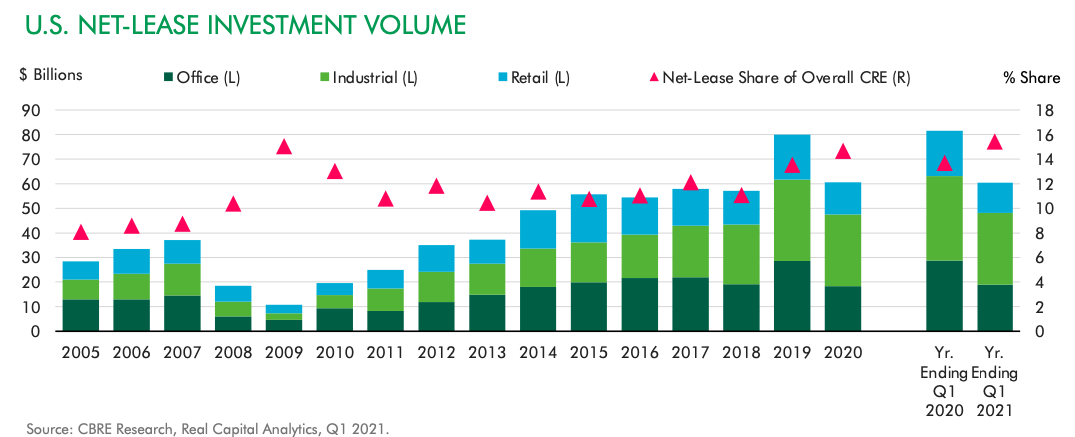

While many people think about net lease in terms of freestanding retail stores (i.e. fast-food restaurants or convenience stores), office and industrial net lease transactions each make up a greater percentage of the overall transaction market, per CBRE (reference the chart below). Over time, many businesses have concluded that owning real estate is not a core competency or optimal use of capital. Thus, many businesses have elected to lease their real estate rather than own it. This has resulted in a rising popularity of sale-leaseback transactions, which has been a tailwind for expansion of the net lease sector.

Net lease investing is a fairly simple and hands-off approach to owning real estate. For most net lease assets, the tenant manages the building day-to-day and pays the operating expenses. Landlord capex is fairly minimal, given that the tenant usually shares in those costs with the landlord. Finally, lease durations are generally very long (10+ years), resulting in limited tenant turnover. All in, net lease assets generally produce consistent cash flows and returns over time, requiring less effort than most other property types.

Quick Note: Think of this blog post as part net lease real estate primer and part net lease sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Net Lease Structure

Net leases are most common in single-tenant buildings, where the tenant is responsible for paying the building’s operating expenses and pays a net rent to the landlord. There are a few different types of net leases, detailed below. The most common lease type is a triple-net lease, which is most associated with the net lease sector.

- Triple-net (or NNN) lease: single-tenant building, tenant is responsible for paying all operating expenses.

- Double-net (or NN) lease: can be multi-tenant or single-tenant building, tenant is responsible for paying their share of property taxes and insurance.

- Single-net (or N) lease: can be multi-tenant or single-tenant building, tenant is responsible for paying their share of property taxes.

The average lease term for a triple-net lease is long in duration, often ten years or more. Given that the tenant usually spends money to build out their space and operates it as if it were their own, they typically want to remain in occupancy for a long period of time. In terms of rent growth, rent increases are often based on predetermined rent steps (i.e. 2% annually or 10% every 5 years) or are tied to an inflation index. Suffice it to say, rent growth is fairly minimal in the net lease sector.

From a landlord’s perspective, the long lease duration is attractive because it provides assurity of rent and stable cash flows for a long period of time. While the landlord gives up the right to raise rents inline with market rental rates (assuming market rents grow faster than 2%-3%), in exchange the landlord receives the benefit of having limited tenant turnover costs.

Net Lease Property Types

Net lease real estate is defined by its lease structure rather than its property type, meaning that a mix of property types fall into the net lease sector, including office, industrial, and retail. Below is a chart from CBRE showing total net lease transaction volume over the last cycle, divided by property type (office in dark green, industrial in light green, and retail in blue). This chart indicates that office and industrial net lease properties have made up a growing piece of overall net lease transaction volume, with retail growing but to a lesser extent.

The overall rise in net lease transaction volume has been supported by the secular trend of companies operating asset-light businesses. Increasingly, businesses don’t view owning their real estate as an optimal use of capital, instead preferring to lease their real estate on a long-term basis. The sale-leaseback transaction type has become more popular over the last cycle, where a business that owns its real estate sells its building to a third-party investor and then net leases the building back on a long-term basis.

Types of Tenants

In terms of tenants, below is a list of several tenant categories and companies most commonly found in net lease deals. Note that most of these tenants are in the retail sector, simply because the retail sector tends to be more concentrated than that of the office or industrial sectors. A smaller number of large retailers tend to operate a lot of retail locations, making up a significant percentage of net lease transactions. In contrast, the office sector tends to be the least concentrated, given that most companies don’t have more than a few office locations.

Tenant Categories

Convenience Stores: 7-Eleven, Circle K, Speedway

Grocery/General Merchandise: Walmart, Kroger, Albertsons

Wholesale Clubs: Costco, Sam’s Club

Drug Stores: Walgreens, CVS

Dollar Stores: Dollar General, Dollar Tree

Fitness/Gyms: L.A. Fitness, Lifetime Fitness

Movie Theaters: Regal, AMC

Quick-Service Restaurants: KFC, Taco Bell

Home Improvement: Home Depot, Lowe’s

Bank branches: Bank of America, Chase Bank

Industrial logistics: FedEx, Amazon

Capex

Capital expenditures (or lack thereof) is another defining feature of the net lease sector. In net lease, tenants are often responsible for at least a portion of the ongoing capex. Often, the landlord is responsible for major exterior structural updates (i.e. a roof replacement), while the tenant covers smaller ongoing capex items. Additionally, in net lease there are less re-leasing expenses. This is due to longer lease terms and limited tenant turnover. This results in capex for the net lease sector of less than 5% of NOI, on average. This compares favorably to other sectors, where capex is regularly more than 15% of NOI.

Bond Wrapped in Real Estate

Since net lease properties are very often leased to a single tenant on a long-term basis, the primary risk for investors is tenant credit risk. From an investment perspective, triple-net lease real estate is often compared to owning bonds, given that the primary risk for each is credit risk and they each produce relatively fixed cash flows over a long time period.

In net lease, it is common for the tenant to provide a corporate guarantee to back up the lease. A corporate guarantee provides surety to the landlord that even if the individual location isn’t profitable anymore or strategic to the organization, the rent is still guaranteed by the company. Assuming a corporate guarantee exists, net lease assets can effectively be thought of as “bonds wrapped in real estate”, or bonds that are further secured by real estate.

In terms of pricing, cap rates on net lease deals are typically priced at some positive spread above the yield of the corporate bonds of the tenant. For example, assuming that Walgreens corporate debt yields around 3%, then Walgreens net lease deals might trade in the 5% cap rate range. This additional yield (5% vs. 3%) accounts for two risks inherent to real estate vs. corporate bonds:

1) Illiquidity risk

2) Lease rejection risk

Illiquidity risk is simply the risk that owning a building is not as liquid as owning a corporate bond. Lease rejection risk is the risk that a tenant can reject its leases and walk away in a Chapter 11 bankruptcy scenario. In contrast, tenants or companies in Chapter 11 cannot simply reject interest payments on corporate bonds. Rather, companies would need to first get approval by the majority of creditors in order to restructure debt and interest payments.

Performance During COVID

The net lease sector held up relatively well through COVID, with minimal sector-wide impact. A portion of retail tenants were granted rent forbearance for a period of time, though this was remedied fairly quickly. The pandemic did accelerate several retail bankruptcies that likely would have happened without the pandemic, just a few years later. All things considered, the net lease sector emerged from COVID relatively unscathed, particularly for industrial and office net lease assets.

Going forward, one emerging risk to the net lease sector is inflation risk or interest-rate risk. Generally, the net lease sector performs best in a flat or downward-trending interest-rate environment with minimal inflation. Given that net leases are fixed for long periods of time, a rising rate environment with inflationary pressure makes owning net lease assets less desirable (similar to how a rising rate environment would negatively impact fixed-rate bond prices).

Conclusion

While the net lease sector is smaller than other core real estate sectors (multifamily, industrial, office, retail), it has grown over time. Net lease is a sensible way to finance real estate and is attractive for both tenants and landlords. While the net lease sector is less exciting than other sectors from an investment standpoint, it is both predictable and profitable.

The net lease sector navigated the COVID-19 pandemic relatively well, with long lease durations preventing much cash flow disruption and limiting re-leasing risk. Going forward, one open question is how the sector might respond to an inflationary environment, should that turn out to be the macroeconomic path ahead. The overall outlook for the sector is modestly positive. The caveat is that net lease investing is more of a bottom-up, deal-by-deal analysis, given the importance of tenant credit. One characteristic will surely hold going forward — compared to other real estate sectors, net lease will experience higher lows and lower highs.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.