Executive Summary / “TLDR”

The multifamily or apartment sector is the “core-est” of the core real estate sectors and has attracted a wide range of real estate investors. Over the long-term, the sector has proved itself with strong performance, good liquidity, and a straightforward operating model. One differentiating factor versus other sectors is that the multifamily sector has a more granular tenant base, without large lease rollover risk. Multifamily leases are typically 1 year in length, resulting in revenue growth that fairly closely mirrors shifts in the economy. The primary multifamily demand drivers are job growth and age demographics. Supply has not been an issue for the multifamily market in the last cycle, given the sharp pullback in development following the 2008-09 financial crisis.

Since COVID, the multifamily sector has held up reasonably well, ceding some occupancy and rent growth, with minimal credit loss. Moreover, the market appears to have stabilized as of Q1 2021. Intra-sector performance disparity has materialized, with apartments in southern sunbelt markets materially outperforming apartments in northern, urban centers. Population migration patterns and a strong preference for more space in lower-density markets has largely driven this performance divide.

Age demographics were a marginal tailwind for apartments over the last decade, but will be a marginal headwind going forward. In short, millennials are growing up. The median millennial was about 30 years old when COVID hit, which is the prime family formation age. Millennials are forming families and having a need for more space, which often means moving out of urban apartments and into suburban single-family homes. This demographic trend was massively accelerated by COVID, which was a catalyst for many families to make the move. This is not to say that multifamily demand will be weak going forward, but it simply will not be as strong as it has been historically.

In summary, multifamily is a steady sector that will likely perform well going forward, but it also has less upside than sectors with stronger emerging tailwinds, including industrial and single-family rental. Apartment investors may be wise to focus on certain areas that do have stronger demand, including B+ apartments in growing sunbelt markets and redevelopment of workforce or affordable housing.

Quick Note: Think of this blog post as part multifamily real estate primer and part multifamily sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Multifamily Classifications

Apartments are divided into a few different building types depending on their layout and functionality, including garden style, mid-rise, and high-rise. The descriptions for each type are below.

- Garden style – low-rise buildings with 2-3 floors and green space, typically located in suburban areas.

- Mid-rise – 4 to 8-floor structures, typically located in urban or exurban areas.

- High-rise/urban infill – apartment towers with more than 8 floors, typically located in dense, urban areas.

Other niche apartment types that are less common include mixed-use buildings (apartments with retail on the ground floor), micro-apartments (tiny apartments with less than 400 square feet of space), and subsidized or public housing apartments.

Multifamily can also be classified by quality grades into Class A, Class B, or Class C, similar to other core property types. The descriptions of each quality grade are below.

- Class A – newly constructed or recently renovated apartments with high-end finishes and a range of building amenities. These buildings command the highest rents.

- Class B – slightly lower-quality than Class A apartments, due to a range of factors including age, location, amenities, finishes, and deferred maintenance. These buildings get average market rents.

- Class C – lowest-quality apartments due to inferior location, old age, deferred maintenance, or poor property management. These buildings get the lowest rents.

Lastly, from an investment standpoint, apartments can be classified by type of investment opportunity, which includes the following types below.

- Core – high-quality assets that are fully leased and located in strong markets. These assets tend to have the highest prices and lowest yields.

- Core plus – similar to core, but with either a small value-add component or a slightly inferior location. These assets carry more risk and have higher yields.

- Value-add – older assets that require varying degrees of renovation, including upgrading units, common areas, or enhancing amenities. These assets tend to have lower starting yields, but grow during the investment period as capital is invested. Value-add deals have become very popular in recent years, given their attractive return potential.

- Opportunistic or development – full-scale repositioning of an asset or a ground-up development project. These assets have both the highest risk and highest return potential.

Multifamily Characteristics

Most apartment layouts have 1-2 bedrooms and are less than 1,000 square feet in size. There are also studios and 3-bedroom units, though these layouts are much less common. Multifamily amenities in Class A and B+ buildings commonly include covered parking, swimming pools, outdoor grills, fitness centers, tennis courts, and resident lounges. Below are some sample images of common multifamily amenities, per CBRE.

Resort-style swimming pool

Source: CBRE Multifamily Primer

Fitness center

Source: CBRE Multifamily Primer

Leases and Rent Growth

Most apartment leases are 1 year in length, with a very small percentage that are less than 1 year or greater than 18 months. The average tenant length of stay is approximately two years, which means that tenant turnover in a multifamily building is roughly 50% of residents each year. This results in active leasing management as tenants cycle in and out of the building. Typically, an apartment building has a small on-site staff that is responsible for managing and leasing the building.

Multifamily rent growth is divided between new lease rent growth and renewal rent growth. In strong market environments, new lease rent growth is usually higher than renewal rent growth. In weak market environments, the reverse can be true, since new lease rent growth may be minimal or even negative, whereas renewal growth can still be modestly positive. New and renewal rent growth are blended together in order to produce average rent growth for the asset. Then, average rent growth is combined with occupancy growth in order to arrive at total revenue growth for the building.

Multifamily Market Size

The U.S. multifamily market size is about 23 million units, per NMHC (National Multifamily Housing Council, an industry trade organization). This compares to about 90 million single-family homes in the U.S. The total value of all apartments in the U.S. is about $5 trillion, per NMHC. Institutional ownership in the multifamily sector has been rising over the past few decades, with multifamily now representing about 25% of the NCREIF Property Index (second only to office), up from 11% of the Index 25 years ago, per CBRE.

Historical Performance

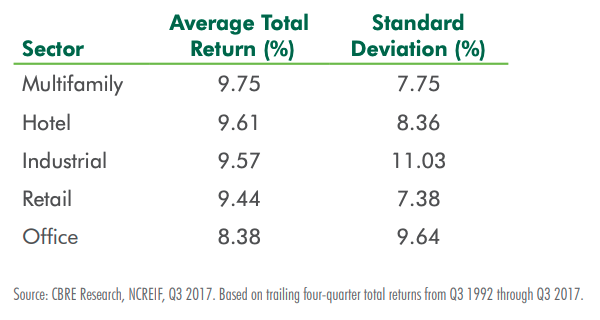

The multifamily sector gets good marks on historical performance. The sector has the highest returns of any commercial real estate sector over the last 25 years at 9.8% average annual returns, per CBRE. Multifamily also has the second-lowest standard deviation of returns over this period, meaning that the multifamily sector has produced very attractive risk-adjusted returns. In part because of its historical track record, multifamily is considered to be a more “defensive sector” in the real estate investment world. The below chart from CBRE details the historical performance by sector over the last 25 years.

Liquidity

Another attractive feature of the multifamily sector is liquidity. Of all the core property types, multifamily has the greatest liquidity. This is due to a few factors, including 1) strong historical investment performance, 2) a large number of buyers and sellers, both domestic and international, and 3) a very robust debt financing market anchored by government sponsored entities (Fannie Mae and Freddie Mac).

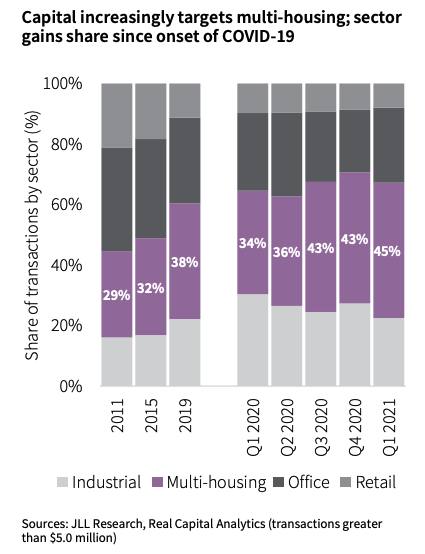

The below chart from JLL shows transaction volume broken out by property type, with multifamily represented by the purple bars. From 2011 through 2019, multifamily overtook office as the sector with the greatest share of transaction volume. Since COVID, multifamily has expanded its position as the sector with the highest amount of transaction volume. This is likely due to the availability of debt financing and the fact that multifamily is considered to be a safer than other sectors.

To be continued in Multifamily (Part 2)…

Given that the multifamily sector has a lot of ground to cover, we broke this post into two parts. In the second part, we’ll provide an overview of the fundamental demand drivers for the sector, analyze the ways in which the sector has been impacted by COVID, and conclude with our outlook for the sector.