Note: If you have not already read Part 1 of the Multifamily Sector Series, you may want to start there. Part 1 provides a basic overview of multifamily real estate, including categories of multifamily, market characteristics, and historical performance. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Multifamily Demand Drivers

The primary demand drivers for multifamily are 1) job growth, 2) age demographics, and 3) household formation.

- Job Growth

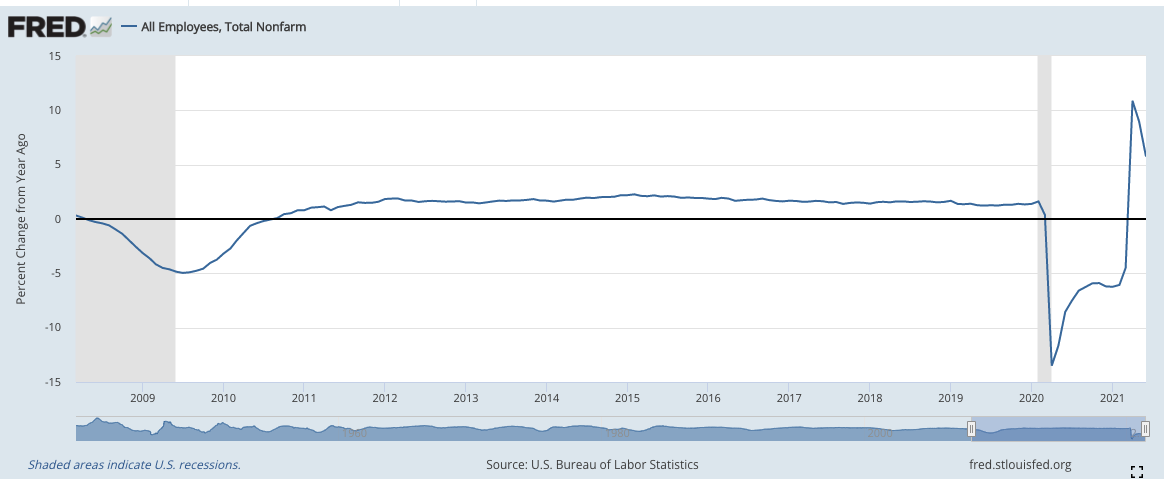

Historically, there has been a high correlation between job growth and multifamily revenue growth. This makes intuitive sense — the stronger the job market, the more likely people are to move for jobs, whether relocating to a new city or moving out of their parents’ house. Below is a chart showing year-over-year job growth in the U.S. over the last cycle. The job growth numbers were steady for most of the cycle, in the 1%-2% range, before plunging sharply due to COVID, and subsequently rebounding strongly. All in, the U.S. is still down a significant number of jobs compared to pre-COVID levels, as of June 2021, though the trajectory is very positive. This bodes well for a rebound in demand in the multifamily sector.

- Age Demographics

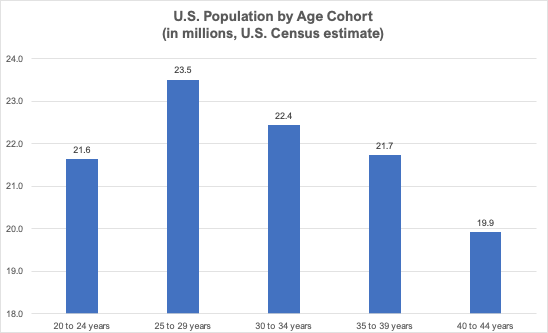

The prime apartment renter base is young adults in their 20s. Young adults tend to have a lot of transition periods in their lives that cause them to move. In addition, many young adults have not saved up enough to be able to afford a home and instead choose to rent. Below is a chart showing the U.S. population by age cohort, per the U.S. Census Bureau (as of 2019). The largest age cohort is the 25-29 year bucket. This large millennial cohort has provided a nice tailwind for multifamily demand over the last cycle.

That said, millennials are growing up and will soon be moving out of the prime apartment renter bucket and into the prime single-family home bucket. COVID has accelerated this shift by creating more demand for larger living spaces in less dense areas (i.e. suburban single-family homes).

Source: U.S. Census Bureau (July 2019)

- Household formation

Household formation is defined as the net change in number of households in the U.S. Household formation is driven by a variety of factors, including population growth and age distribution, job market strength, immigration, and societal norms. Household formation is very much related to the first two apartment demand drivers, job growth and age demographics. The below chart shows total households in the U.S. over the last cycle. Despite some noise in household estimates around COVID, household formation has generally experienced a nice upward trend, with some minor bumps along the way. This is supportive of strong residential and multifamily demand.

Supply

In terms of supply, the best data to analyze is multifamily housing starts and completions, published monthly by the U.S. Census Bureau. Multifamily completions count apartment units when they are completed and delivered, whereas multifamily starts count apartment units upon construction commencement. Thus, multifamily starts are a more forward-looking indicator of future multifamily supply. Historically, the construction cycle for multifamily is about 12 months, meaning that multifamily starts lead multifamily completions by about a year. Below is a chart of multifamily housing starts over the last cycle. Note that multifamily housing starts peaked just prior to COVID, then fell significantly at the beginning of COVID, and have recovered since then.

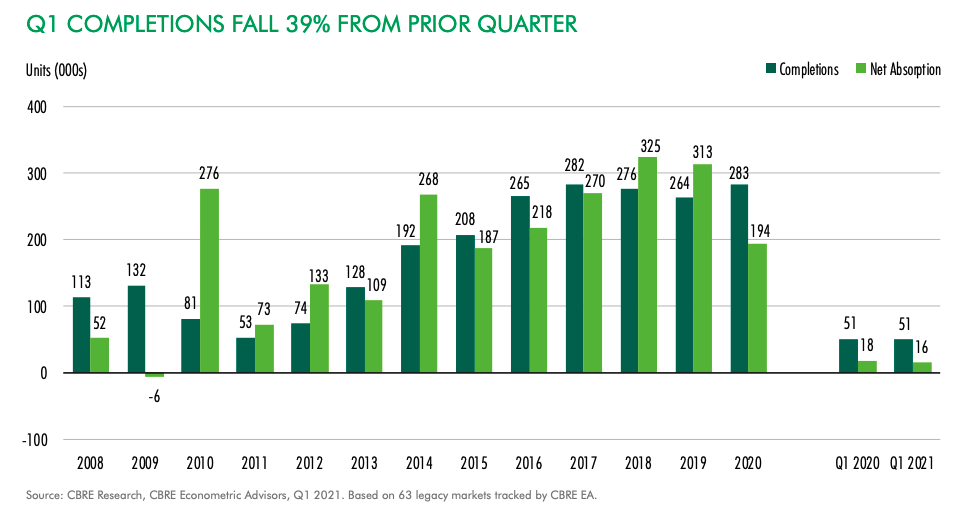

Putting together both supply and demand, the below chart from CBRE shows multifamily completions (dark green bars) and net absorption (light green bars) over the last cycle. Net absorption is simply newly leased space, less newly vacated space over a given period. The chart shows that despite rising multifamily completions over the last cycle, demand has been equal if not higher, with net absorption roughly inline with completions.

Occupancy & Rent Growth

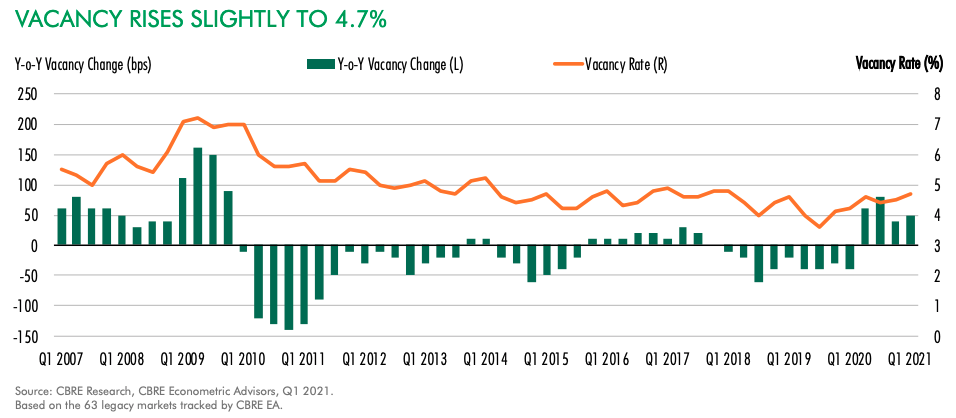

Given strong demand for multifamily units relative to supply, multifamily vacancy has steadily trended lower over the last cycle, from a peak of just over 7% vacancy in 2009 to under 4% prior to COVID, per the below chart from CBRE. Since COVID, multifamily vacancy has ticked up modestly to just under 5%. Note that similar charts from other sources show higher starting and ending vacancy rates, but the trend is the same.

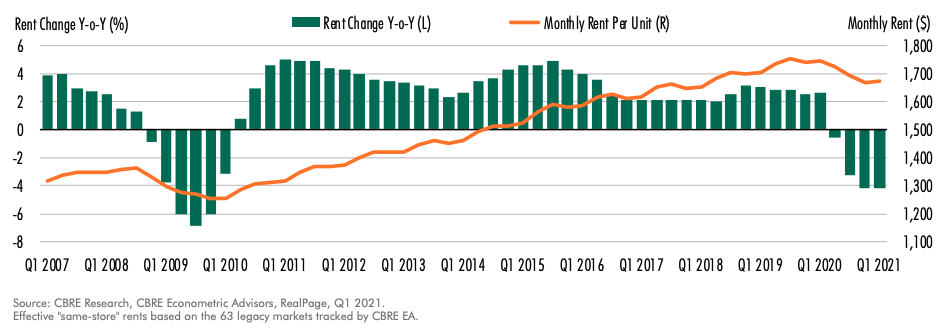

It’s no surprise that rent growth during this period has also been robust. For the early part of the last cycle, multifamily rent growth trended in the 4% range, before notching down to the 2%-3% range in 2017, per the below chart from CBRE. During COVID, rent growth turned negative as landlords were forced to cut rates and offer concessions in order to maintain occupancy. The caveat is that these post-COVID numbers are disproportionately impacted by San Francisco, San Jose, and New York, three markets that were hit particularly hard by COVID. Removing these markets, the rent decline in Q1 2021 would have been -1% vs. -4%. Going forward, demand appears to be firming up as of Q1 2021 and rents will likely bounce back in the medium-term.

COVID-19 Impact on Multifamily

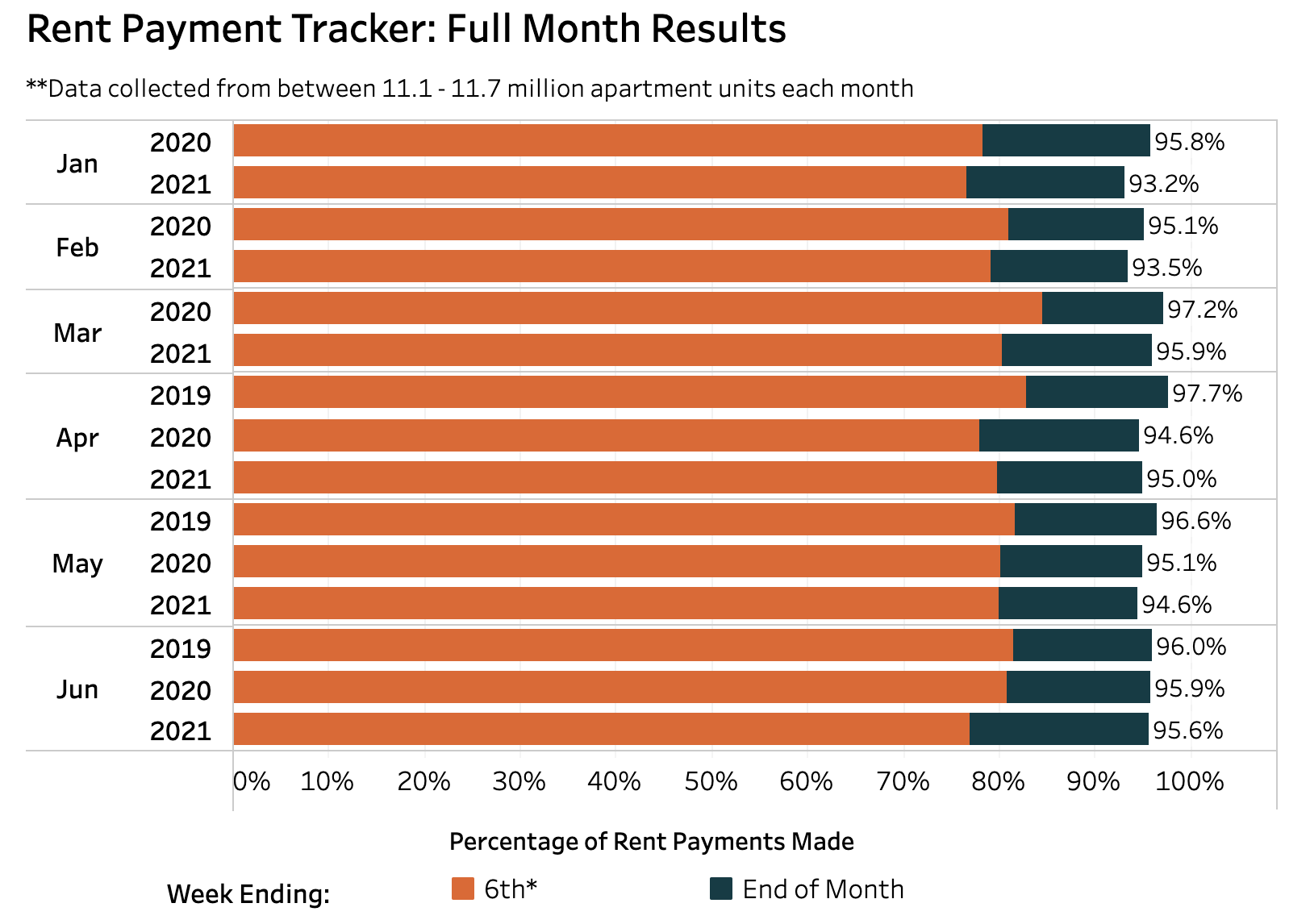

The impact of the COVID pandemic can be broken down into the near-term impact and the likely long-term impact. In the near-term, the multifamily sector was negatively impacted, but not nearly to the extent felt by the hotel sector. Government support programs were effective in bolstering the economic position of many U.S. residents. Also, since people spent a lot more time at home, they placed a higher value on their residences. The below chart from NMHC shows the percentage of apartment rent that was collected on a monthly basis for pre-COVID months vs. those same months post-COVID. The rent collection data indicate that while the rent collection numbers fell off modestly in the calendar months January through May, for the month of June the difference was almost indistinguishable.

Source: NMHC Rent Payment Tracker

Obviously, analysis of rent collection only accounts for the risk of credit loss and does not account for any decline in occupancy or rents resulting from COVID. There has been a measurable falloff in occupancy and rent growth since COVID, as illustrated by the CBRE charts above. That said, assuming a fairly quick economic recovery, as many are projecting, the impact will not be nearly as severe as that of the last recession in 2009.

The long-term impact of COVID on the multifamily sector is more interesting to analyze, since it is still largely unknown (as of August 2021). The long-term impact can be divided into 1) population/demographic shifts and 2) emerging sector trends.

Population/demographic shifts

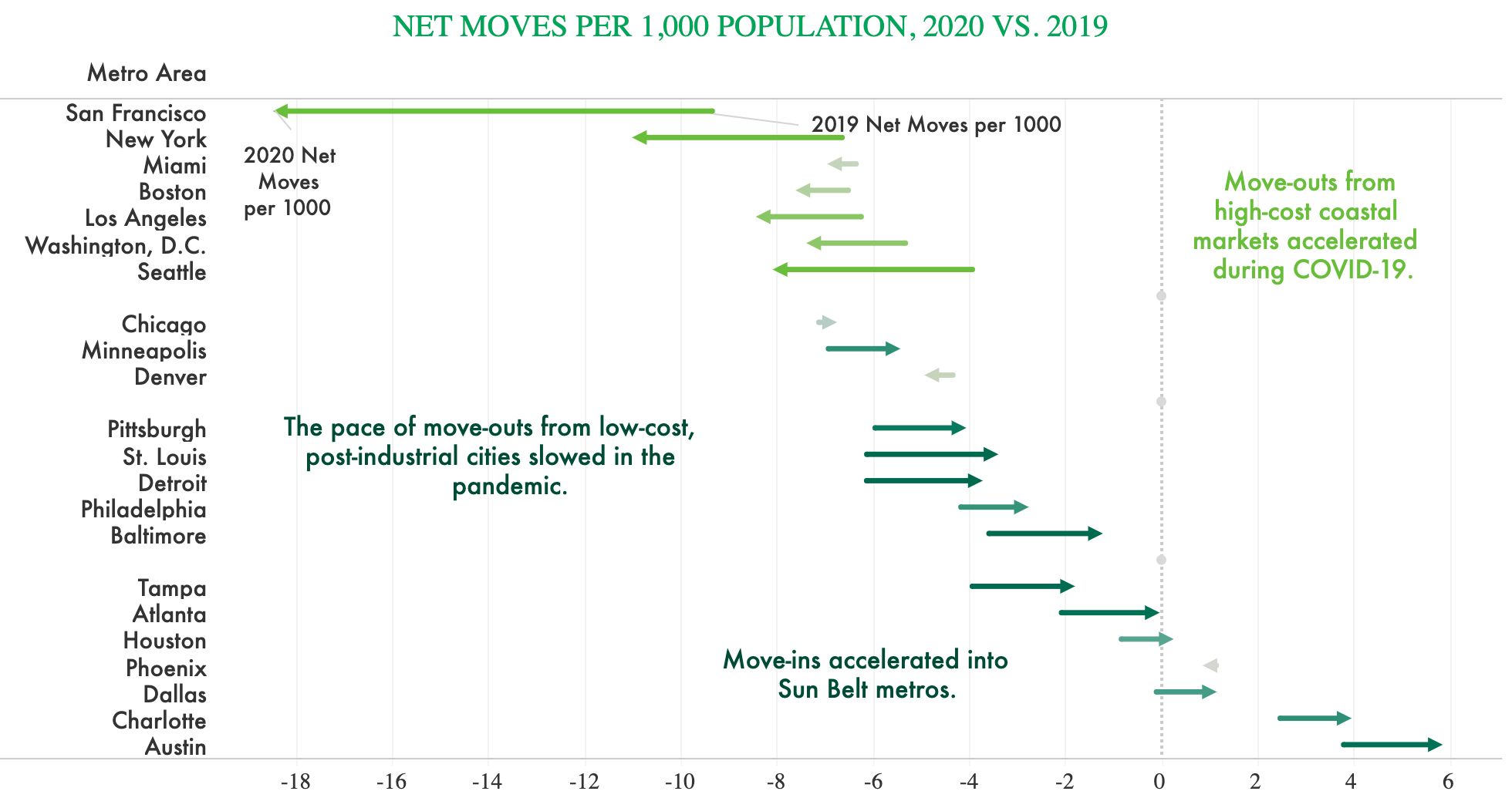

One big shift caused by the COVID pandemic is the short-term migration out of dense cities to less dense cities, suburban and rural areas. In one study, CBRE analyzed net moves to major MSAs in 2019 vs. 2020, which roughly captures the impact of COVID. The chart below shows the results, with large net move-outs from San Francisco, New York, Boston, and L.A., and net move-ins to Austin, Charlotte, Dallas, Atlanta, and Tampa. To a significant extent, the cities already experiencing the greatest share of move-outs in 2019 saw the impact magnified in 2020 (largely move-outs from northern, high-cost of living cities), whereas the cities experiencing the greatest share of move-ins in 2019 saw that effect magnified in 2020 (largely move-ins to southern, lower-cost of living cities).

Source: CBRE

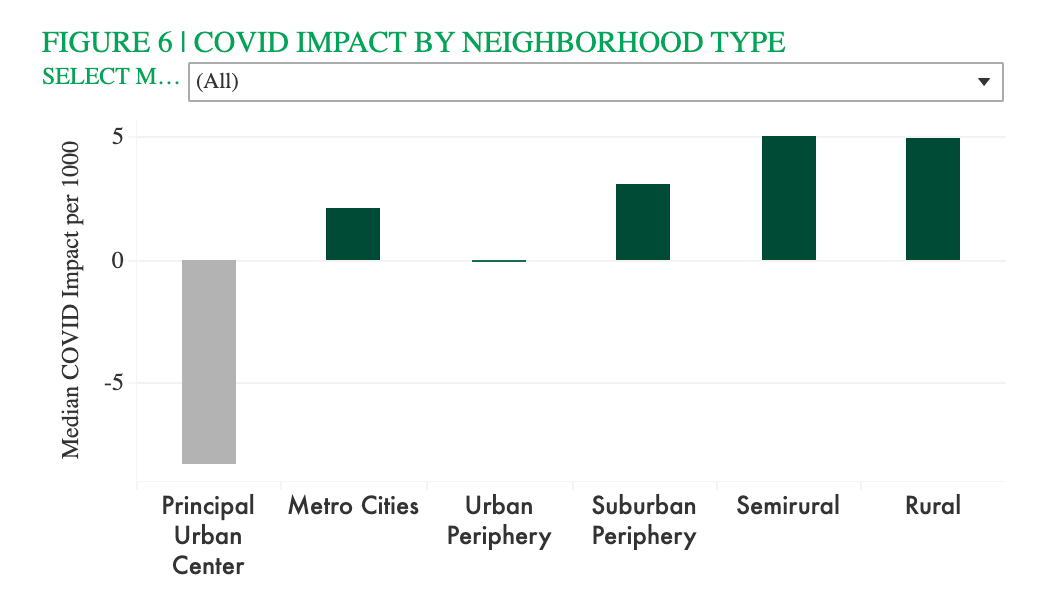

This second chart below from CBRE summarizes the net moves by neighborhood type, with a clear marginal loss of population in urban centers and a marginal gain in population in suburban, rural, and semi-rural areas as well as lower-density cities. The big question for the multifamily sector is how much of these migration patterns will be temporary vs. more permanent? For some, it may not be practical to live outside of dense, urban areas, particularly for young professionals in their 20s. Though at the margin the scale has tilted in favor of living in non-urban areas, due to increased prevalence of remote work, greater acceptance of living outside of daily commuting distance of the office, and increased appeal of lower-density and lower-cost-of-living communities. This development is a headwind for apartments located in dense, urban environments.

Source: CBRE

A second macro shift caused by COVID is a pull-forward in demand from the millennial cohort for single-family homes. The median millennial was about 30 years old at the onset of the COVID, which is the prime family formation age. Thus, many millennials accelerated their plans to move to the suburbs in 2020-21, given the reduced benefits and higher risks of living in urban areas. In addition, having more living space became much more valued by people across the board, given the increased time spent at home during COVID. Millennial migration to the suburbs will likely continue at an accelerated pace, which is net negative for urban apartments and a net positive for suburban single-family homes.

Emerging sector trends

Similar to other sectors, the tastes and preferences of consumers have changed due to COVID, resulting in a few emerging trends for the sector. These trends including the following:

- Greater demand for larger apartments with more space, which is a reversal of a decade-long prior trend towards smaller apartments

- Desire for dedicated office space for 1 or 2 people, in order to accommodate work from home at least a couple of days per week

- Increased incorporation of technology solutions through the entire apartment rental process (virtual tours, contact less showings, online lease signing, rent payment, and maintenance requests, and mobile apps for resident services)

- Greater demand for value price points and high-quality workforce housing, given the reduced economic security of lower-income households as a result of COVID

Conclusion

The multifamily sector has historically been a strong performer that culminated in the years following the 2008-09 financial crisis, when demand rebounded alongside limited supply, with the millennial cohort in its prime apartment renting years. Fast forward a decade, and COVID has marginally reduced the appeal of living in apartments in urban areas while millennials are now forming families and moving to single-family homes in the suburbs. While this is an overly simplistic narrative for the sector, it frames big issues. Stepping back, demand for residential living spaces, whether apartments or single-family homes, will remain strong going forward, and supply is very much in check at present. The outlook for the multifamily sector is positive, though perhaps not as positive as that of its smaller but faster-growing cousin, single-family rental.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.