Executive Summary / “TLDR”

The U.S. self storage industry got started in the 1960s in the state of Texas, where most homes lack basements (and thus extra storage space). Self storage units back then were simple boxes with garage-like doors that locked. The industry has evolved somewhat since then, with large, multilevel structures housing indoor units commonplace in both urban and suburban areas today. The sector has performed well over time, due to its steady demand profile through economic booms and busts. Additionally, operating margins are high and capex is low, resulting in a strong cash-on-cash profile for the sector.

This solid performance has attracted more capital to the sector, most recently in the period from 2015 through 2019, which resulted in an acceleration of new supply. This new supply temporarily dragged on rate growth in 2018-19, but things quickly turned positive after COVID hit. Demand for storage rebounded sharply, driven by a spike in demand for business and residential storage precipitated by the pandemic. Moving activity accelerated as many people relocated for various reasons, which is a positive driver of self storage demand. As a result, self storage rate growth rebounded from slightly negative pre-pandemic to positive 10% as of mid-2021, a very robust level.

While some of the COVID-induced demand spike is temporary, a portion of it may be more permanent, given the higher priority placed on residential space post-COVID. In addition, COVID introduced a new cohort of customers to the self storage industry, many of whom may not have found it otherwise. COVID was a positive catalyst for self storage demand. On the supply side, self storage facilities are relatively easy to build, so supply will eventually follow to meet demand. Even so, the sector is set up to perform very well in the near-to-medium term.

Quick Note: Think of this blog post as part self storage real estate primer and part self storage sector update. We cover the basics for those new to real estate private equity, but also dig into the weeds for those looking for something more. Ultimately, we aim to cover the things that really matter for the sector in just a few, easily digestible pages.

Self Storage 101

Self storage units are simply empty rooms with garage-like roll up doors and secure access. Self storage units come in a variety of sizes, ranging from 5×5 ft. (size of a small walk-in closet) to 20×20 ft. (size of a two-car garage). Suburban self storage facilities often have outside parking available for RVs, boats, and other motor vehicles.

The self storage industry in the U.S. originated in the state of Texas in the 1960s. Many homes in Texas lack basements, and thus residents had a greater need for storage space outside of homes. Back then, self storage units were arranged in rows of outdoor, street-level units with no climate control. Below is an example of a basic outdoor self storage facility with drive-up access.

Example of outdoor drive-up storage units (non-climate controlled)

Photo Credit: Scott Meyers

The industry has evolved since then, and self storage facilities have migrated toward multi-story structures with indoor, climate controlled units. This is especially the case in urban areas where building footprints are more limited. Though this model has also become more popular in suburban areas. Below is an example of a multi-story self storage facility in an urban area.

Example of a Multi-Story Self Storage Building

Source: CubeSmart company presentation

Lastly, below is a picture of indoor, climate controlled self storage units. Indoor units have the same layout and function as outdoor units, only they are located in the interior of the building.

Example of Indoor Climate Controlled Storage Units

Source: ExtraSpace Storage website

In terms of rent, the average monthly rent per square foot as of May 2021 for a self storage unit (per Yardi Matrix) was in the $1.25 – $1.40 per square foot range. For a standard 10×10 ft. unit, or 100 square feet of space, this translates to a monthly rent in the $125 – $140 range.

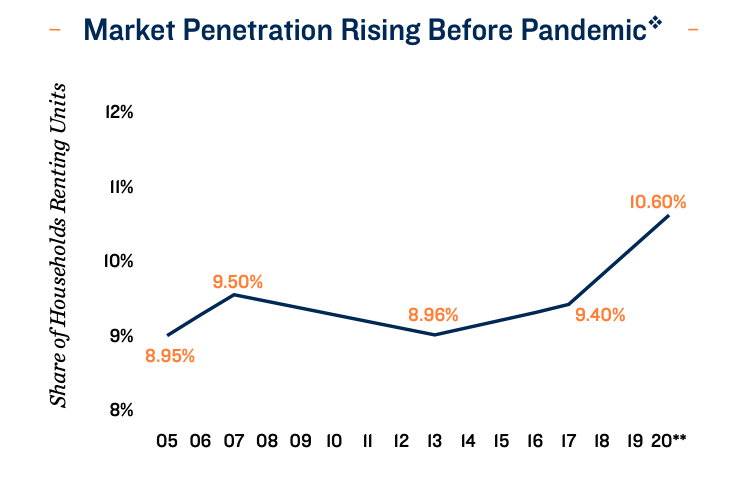

Roughly 10% of U.S. households rent a self storage unit, a number that has been slowly rising over time as adoption rates have increased. The below chart shows customer adoption of self storage in the U.S. over the last 15 years.

Share of U.S. Households Renting Self Storage Units

Source: Marcus & Millichap 2021 Self Storage Outlook

The more common reasons for renting a self storage unit include moving, various life transitions (downsizing a home, divorce, death/estate transition), seasonal equipment storage, home projects/remodeling, college storage, military deployment storage, extra vehicle storage, and business storage.

The factors that determine a good location for a self storage facility include street visibility, ease of access, proximity to customers within a 3-5 mile radius, and household income in the area.

In terms of capex, self storage units require minimal capex, due to the simple build-out and infrequent usage. Capex for a self storage asset is typically less than 5% of NOI, lower than that of most other real estate sectors. The operating expenses to run a self storage facility are on the lower end when compared to other sectors, resulting in fairly high NOI margins for the sector (>70% for the public REITs).

Market Summary

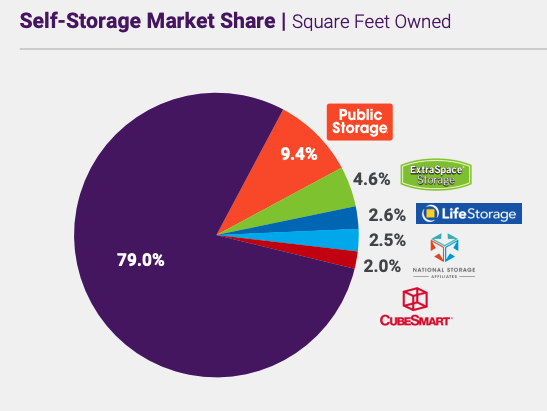

There are approximately 50,000 self storage facilities in the U.S. totaling approximately 1.9 billion square feet, per Self Storage Almanac. This puts the average facility size at around 40,000 square feet. The self storage market is fragmented. The largest six players in the market include five public REITs and U-Haul, which is a private company, accounting for 20% of the total self storage market. The other 80% made up of smaller, private companies. Below is a chart showing market share for the largest companies in the industry.

Source: Public Storage presentation

Demand

The main demand drivers for self storage are various life events. These include changing locations for a job, downsizing a home in retirement, divorce and dividing a household, and death and estate transitions. In addition, two trackable metrics that are indicators of self storage demand include 1) Existing Home Sales and 2) Moving Activity. In a good economy, both of these metrics tend to be strong alongside robust demand for self storage.

That said, even during a recession or a weak economy, self storage demand tends to hold up. This is because during recessions, people tend to downsize or consolidate households, which creates a need for storage. Thus, self storage demand is somewhat insulated from economic downturns. Below is a detailed summary of the two key metrics correlated with self storage demand.

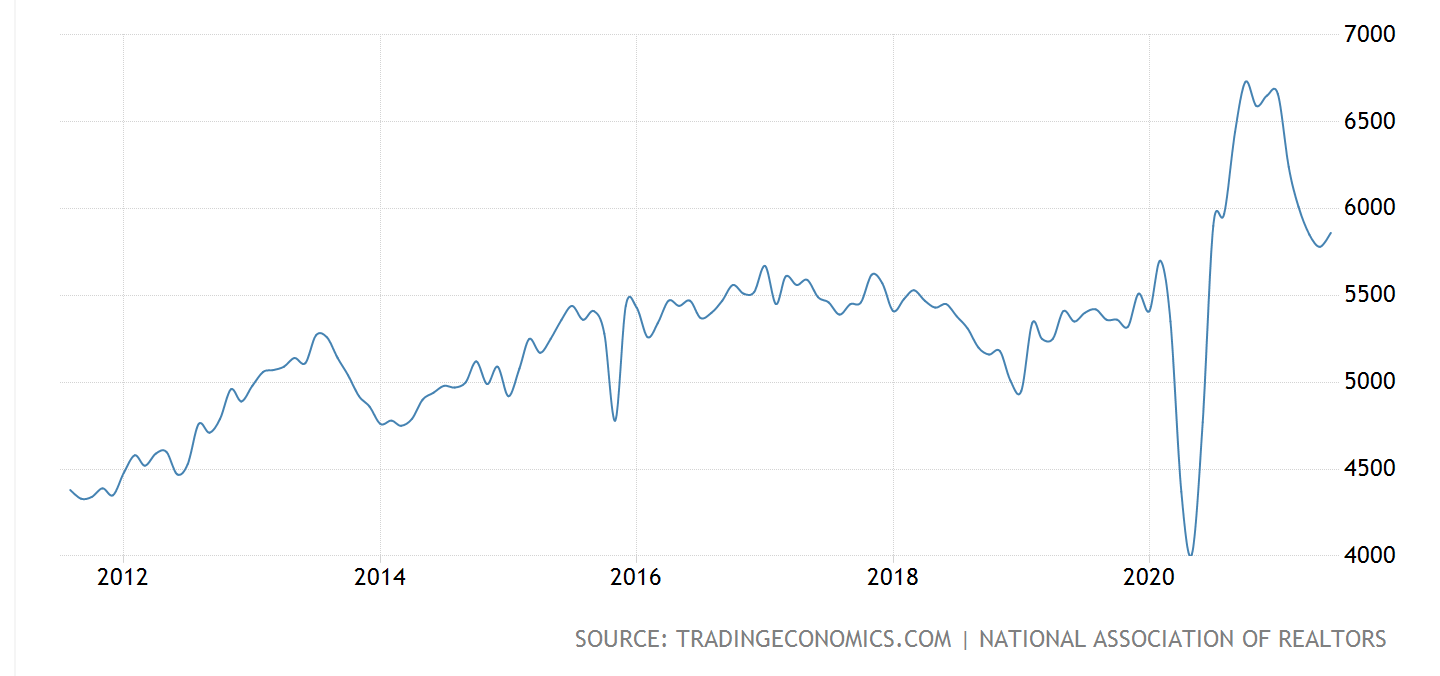

- Existing Home Sales

Existing homes sales are defined as sales of existing single-family homes, condos, and co-ops during a given period. The data is tracked and published monthly by the National Association of Realtors. As indicated in the chart below, existing homes sales trended upward following the 2009 recession, before briefly falling off at the beginning of COVID, and then sharply spiking upward to a new level in the second half of 2020.

Source: Trading Economics, via National Association of Realtors

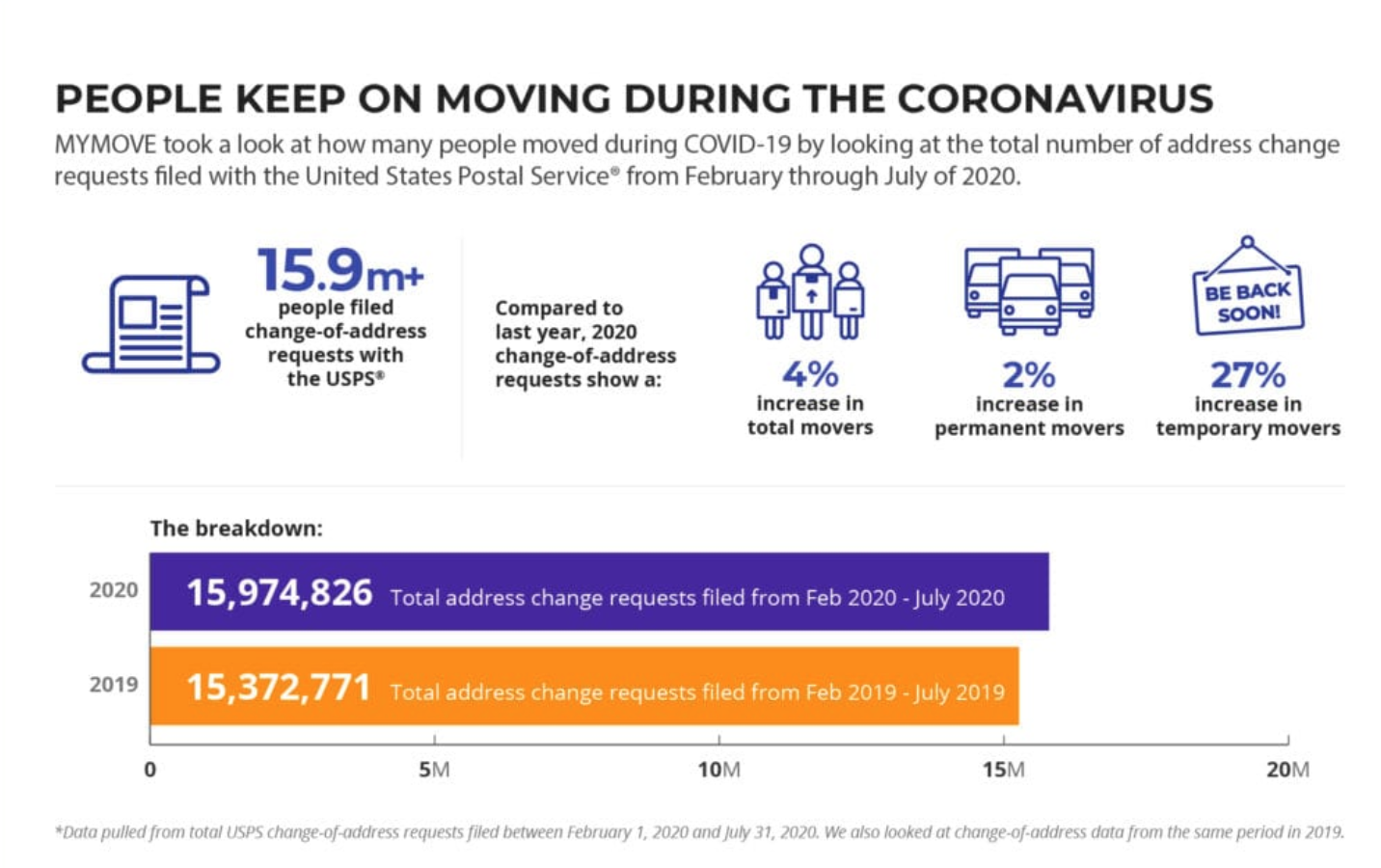

- Moving Activity

Moving activity is more difficult to track, but certain websites have recently compiled USPS change of address requests as a barometer for moving activity. The below infographic shows the number of moves during the first half of 2020 as compared to 2019, which measures the uptick in moving activity as a result of the COVID pandemic. For the first half of 2020, the number of change of address forms increased 4% vs. 2019, or an additional 600,000 moves in the U.S. due to COVID. Some percentage of these residents probably used self storage for a period of time.

Source: mymove.com

In addition, there are COVID-specific demand drivers that emerged for the self storage sector during the pandemic. These include the following:

- Businesses that closed or downsized on a temporary basis due to COVID stored equipment in self storage facilities, resulting in a surge of business storage demand

- Residents stored furnishings while moving out of urban centers on a temporary basis, resulting in greater demand for storage near urban areas

- Residents engaged in de-cluttering activity in order to accommodate home offices, home gyms, or just to create more living space

While the first two categories are more temporary demand drivers, the third category may very well be permanent, as people will probably spend more time at home even after COVID recedes. Self storage demand is currently very robust, due to the above factors as well as an uptick in home sales and moving activity all caused by COVID.

Supply

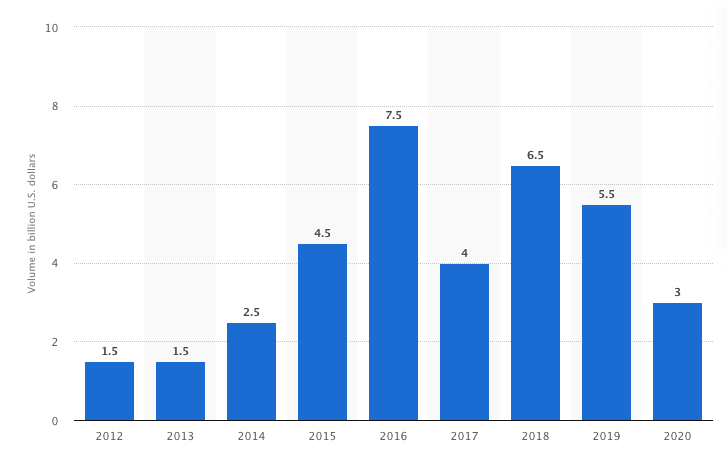

Up until COVID hit and self storage demand inflected higher, supply was a much bigger issue for the sector. Over the last few years, there was an influx of capital into the self storage sector, driving up supply growth. Below is a chart from Statista outlining the volume of self storage investment in the U.S from 2012 through 2020. As indicated in the chart, investment in the sector started to ramp up in 2015 and remained elevated for several years thereafter, even into 2020.

Volume of Self Storage Investment in the U.S.

Source: Statista

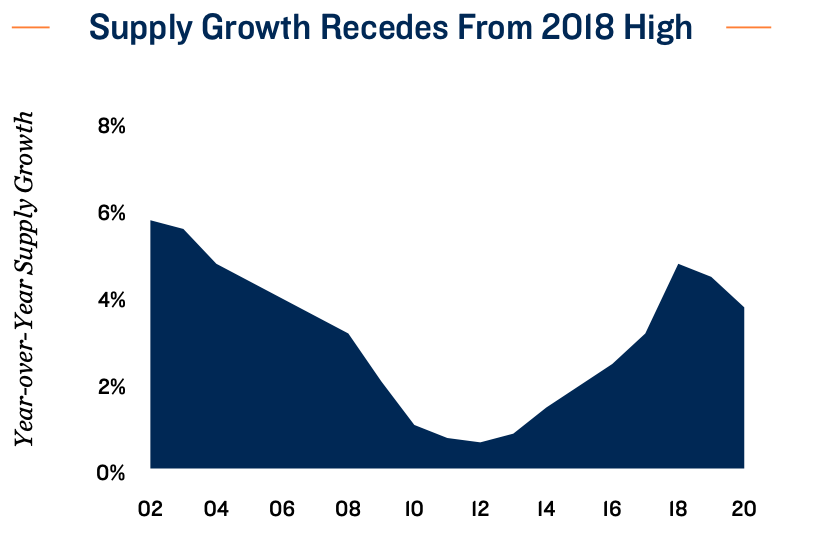

This investment has translated to a significant increase in supply growth in the sector over the last few years, as indicated in the below chart from Marcus & Millichap. As shown in the chart, supply growth peaked in 2018 and decelerated modestly into 2020.

U.S. Self Storage Sector Supply Growth

Source: Marcus & Millichap 2021 Self Storage Outlook

This high level of supply growth weighed on the sector in 2018 and 2019, resulting in a decline in asking rates across the board.

Occupancy and Rent Growth

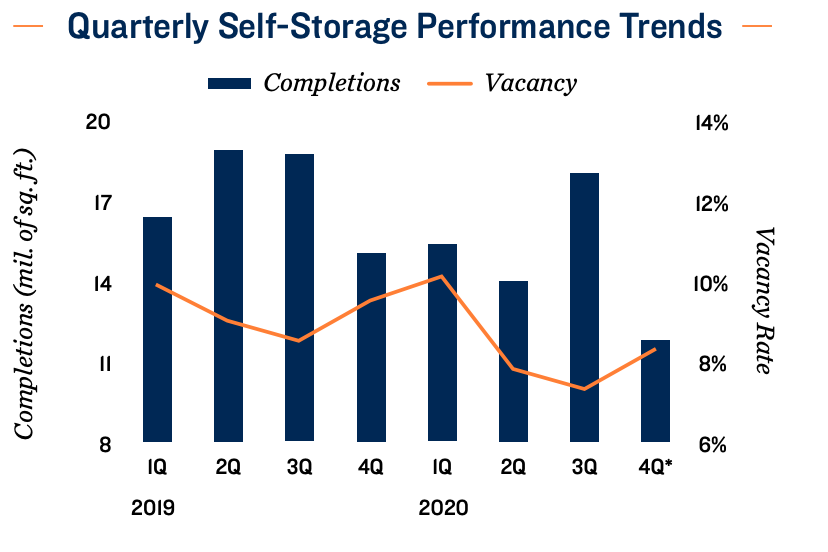

Since COVID, incremental demand has accelerated significantly while incremental supply has receded from its peak. This has resulted in demand significantly outpacing supply, a total reversal from the prevailing market dynamic a couple of years ago. The below chart from Marcus & Millichap shows self storage construction completions (blue bars) alongside the industry vacancy rate (orange line). The vacancy rate ticked up briefly in 1Q 2020, before declining for in the remainder of 2020 as the market tightened back up.

Source: Marcus & Millichap 2021 Self Storage Outlook

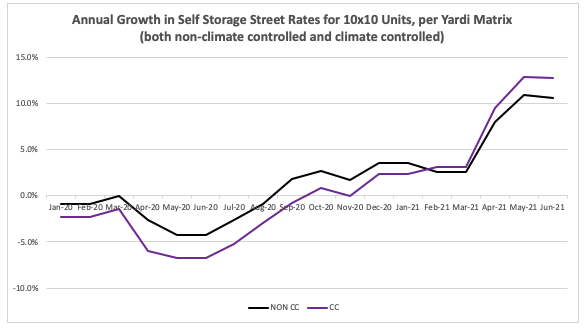

Once occupancy was back up (and vacancy down), operators regained pricing power in 2021. The chart below shows Yardi Matrix published self storage “street rates” (asking rates) based on surveys of operators on a monthly basis. After being negative in the first half of 2020, rate growth inflected positively in 3Q 2020 and continued to accelerate in 2021. The current street rate growth (as of June 2021) is north of 10% on a year-over-year basis, a very robust level.

Source: Data compiled from Yardi Matrix monthly news releases

Conclusion

The self storage sector is gradually moving from being a “fringe sector” to one of the primary food groups, given its strong performance and steady growth over time. COVID acted as an accelerant for self storage demand for a variety of reasons. Longer-term, demographics are supportive of demand as millennials are entering the core cohort of self storage customers. One key issue to watch going forward will be supply growth, given that storage is relatively easy to build. That said, based on the very robust demand growth since COVID, some of which is likely non-transient, the medium term outlook for the sector is very strong.

Looking to learn more? Why not check out our educational resources! Whether you’re yet to begin a formal real estate private equity interview process or are crunching through real estate private equity interview questions at the last minute, we have what you need. All you need to bring is your effort.