Almost all real estate transactions are financed with debt, with debt levels dependent on the borrower’s investment strategy, risk tolerance, and capital markets availability. In doing so, investors are able to reduce their upfront capital outlay and increase their return on equity. By incorporating debt, investors can enhance their returns with leverage. But, this is not always the case. In certain situations, adding leverage can negatively impact real estate returns. This phenomenon, known as negative leverage, has become topical as the Fed is in the process of hiking interest rates to combat inflation.

Understanding Leverage

Typically, leverage is measured by the property’s loan-to-value (LTV) ratio, which is the ratio of the property’s loan amount divided by the property’s purchase price. For example, suppose an investor acquires a building for $10 million and obtains a $7 million loan, funding the remaining $3 million with equity. The LTV on this deal would be 70% or the $7 million loan divided by $10 million purchase price.

Typically, LTVs range from 50% to 80% depending on investment strategy, property type, asset quality, and cash flow profile, with higher percentages representing higher levels of leverage. In most situations, particularly during periods of low interest rates, higher leverage levels will increase equity yields (also known as cash-on-cash returns, calculated as net cash flow divided by the equity).

For an investor to benefit from having leverage, the property’s going-in cap rate has to be higher than the interest rate (or loan constant, which is the annual debt service as a percentage of the total loan amount). Thus, the investor earns the spread between the cap rate and the interest rate, magnified by the leverage amount. In addition, the property value must appreciate during the hold period in order for the investor’s equity investment to gain value.

Positive Leverage

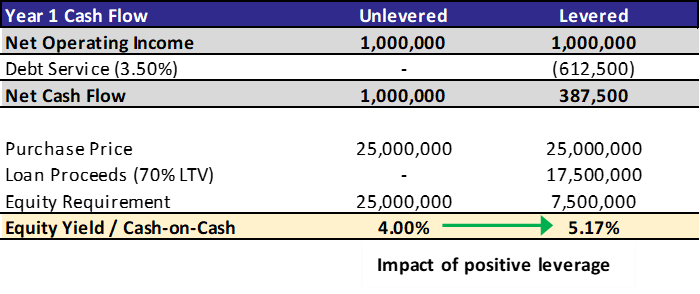

To demonstrate this, let’s look at a simple scenario comparing equity yields on a hypothetical acquisition with 70% debt (levered scenario) versus an all-cash deal (unlevered scenario). Let’s assume the investment has the following characteristics:

- Purchase Price: $25 million

- Cap Rate: 4.00%

- Loan-to-value (LTV): 70%

- Interest Rate: 3.50%

In the above example, the cap rate on the deal is 4.00%, which is higher than the interest rate of 3.50%. Since the cap rate is greater than the interest rate, the investor increases their equity yield from 4.00% to 5.17% through the use of leverage.

Note that you can quickly calculate the levered equity yield using the following formula:

Equity Yield = Cap Rate + (% Debt / % Equity) x (Cap Rate – Interest Rate);

For the above example: 4.00% + (70% / 30%) x (4.00% – 3.50%) = 5.17% equity yield

Negative Leverage

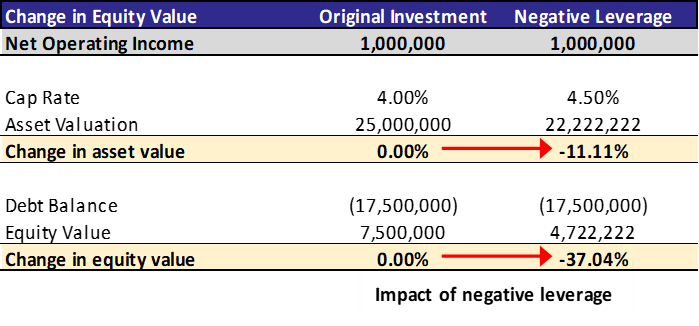

Now, let’s consider a scenario where both interest rates and cap rates increase, degrading the property’s value and reducing the refinancing loan achievable by the borrower after a 3-year hold period. For simplicity, let’s assume that the property’s cash flows remain the same over this 3-year period. Assuming a 100 bps increase in the interest rate and a 50 bps increase in cap rate, what happens to the investor’s equity value?

Given the 50 bps increase in cap rate, the property value decreases by 11%, and after factoring in leverage, the equity value decreases by 37%. In this case, the investor would most likely decide to wait to sell the property or refinance the debt until the NOI grows enough in order to offset the increase in cap rate.

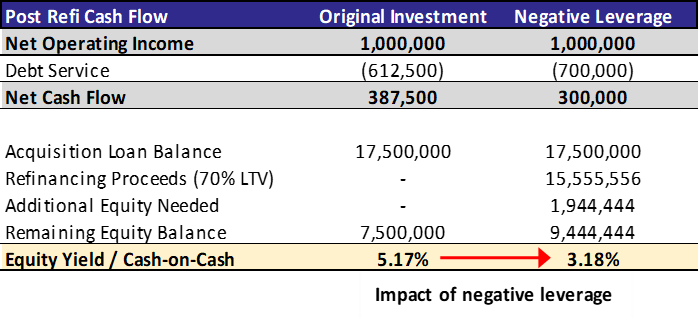

But, what if the investor has no choice but to refinance the debt in a down market due to a debt maturity? Let’s look at how the investor’s equity position is impacted if they refinance the debt using the same cap rate and interest rate assumptions above (100 bps increase in interest rate and 50 bps increase in cap rate).

As shown, the $15.55 million in loan refinance proceeds (based on a 70% LTV on a $22.2 million valuation) are not enough to repay the original loan balance of $17.5 million. Thus, the investor must put in an additional $1.94 million of equity into the deal. This brings the investor’s total equity balance from $7.5 million to $9.44 million, negatively impacting the investor’s equity yield and potentially derailing the investment if they cannot cover this equity deficit.

This negative leverage scenario illustrates the situation that some real estate investors may find themselves in over the next 18-24 months, particularly if they purchased low cap rate deals with short-term bridge loan. Should long-term interest rates continue to increase, this will put additional upward pressure on cap rates and interest rates, exacerbating the issue.

As demonstrated above, increasing cap rates for levered real estate investments can rapidly erode an investor’s equity position. Down the road, this may result in distressed real estate sales down as debt comes due and forces a decision by investors. Or, it may lead to opportunities for rescue financing in order to plug holes in the capital stack. This situation may be the new normal for the real estate industry, following a decade characterized by cheap debt and increasing asset prices. Going forward, investors will need to be more disciplined in their acquisition underwriting and fully consider the range of possible outcomes for cap rates and interest rates. This may also push investors toward longer-term debt and also an increased focus on higher-quality assets with strong fundamentals, where the impact of rising rates can be offset by strong NOI growth.

Final Thoughts

Here’s a final question to consider: in a rising interest rate environment, which property type is most at risk of a negative leverage scenario? Which property type is least at risk? Why?

Looking to learn more? Check out our various professional resources! Whether you have yet to break into the industry or are just starting out in a new role, we have everything you need. All you need to bring is your effort!