According to the latest report from the U.S. Bureau of Labor Statistics, the annual inflation rate in June 2022 was 9.1%, its highest level since 1981, as measured by the consumer price index. This persistently high inflation for several months has forced the Fed to rapidly increase benchmark interest rates. The Fed funds target rate currently sits in a range of 1.50% to 1.75%, following the Fed’s most aggressive rate hike since 1994 of 0.75% in June 2022. As of this writing, the market is expecting another 0.75% interest rate hike in July. With interest rate headwinds already impacting both the public and private equity markets, many investors are wondering what the implications are for the real estate market.

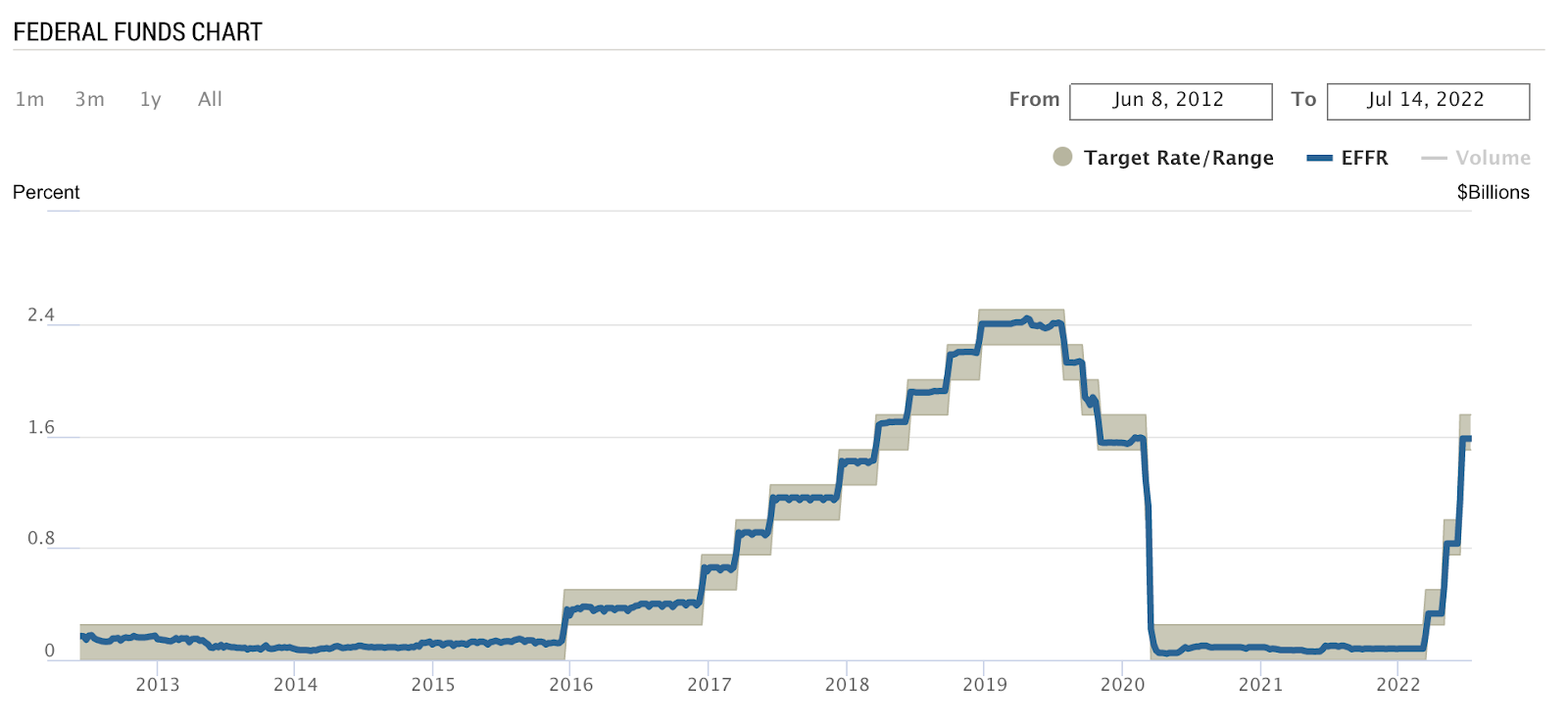

The below chart shows the Fed Funds target rate over the last 10 years, which highlights the recent upward spike in interest rates.

Source: Federal Reserve Bank of New York

Cap rates (or net initial yields in the UK) are a metric used to measure real estate valuations. Cap rates indicate an investor’s unlevered going-in return based on the first year of expected net operating income (NOI) for a property relative to the purchase price. Specifically, cap rates are calculated by dividing the property’s first year of NOI by its purchase price. For example, a property with $1 million in net operating income that was purchased for $20 million would have a going-in cap rate of 5% ($1 million / $20 million). Given the cap rate and the purchase price, the formula can also be rewritten to calculate the property’s NOI: $20 million x 5% = $1 million NOI.

The real estate industry’s usage of cap rates is similar to the bond industry’s usage of yields. In real estate, the primary source of cash flow is based on lease contracts that are fixed over a period of time in the future. This is similar to how bonds have fixed payments for some period of time in the future. Thus, just as bonds are compared by their yields, real estate assets are compared by their cap rates.

Cap rates can be viewed using the framework of the Gordon Growth Model, which helps approximate the value of a stabilized asset that is expected to have cash flow at a fixed growth rate in perpetuity. The framework is as follows:

Real Estate Value = NOI / (Discount Rate – Perpetual Growth Rate)

The cap rate portion of this equation is the denominator: Cap Rate = (Discount Rate – Perpetual Growth Rate).

The Discount Rate can be further broken down into the following two pieces: Discount Rate = (Risk-Free Rate + Risk Premium).

Summing it up, there are three key variables that impact cap rates:

- Risk-Free Rate or Base Rate (approximated by the 10-year U.S. Treasury Rate)

- Risk Premium (varies based on risk appetite for real estate)

- Perpetual Growth Rate (varies based on the supply/demand for a particular property type or market)

So if the base rate moves up by 100 bps or one percentage point, by how much should cap rates move up? There’s no correct answer here, unfortunately. If the risk premium and perpetual growth rate are unchanged, then cap rates should increase by 100 bps. In reality, the risk premium and perpetual growth rate are likely both changing at the same time, which may offset the change in the base rate. That said, a rising interest rate environment does put upward pressure on cap rates and downward pressure on real estate values.

The other big variable impacting cap rates is the cost of debt financing. Since almost all real estate is financed with debt, and nearly all investors focus on levered returns, the cost of debt is a significant variable impacting investors’ ability to pay a higher price or a lower cap rate. If the cost of debt financing goes up, that puts downward pressure on levered returns and in turn, puts upward pressure on cap rates (in order to get back to the same or similar levered returns).

Practical Implications

Now that we understand the variables that impact cap rates, it is important to consider the current market environment and its influence on the future trajectory of cap rates across various asset classes over the near-to-medium term.

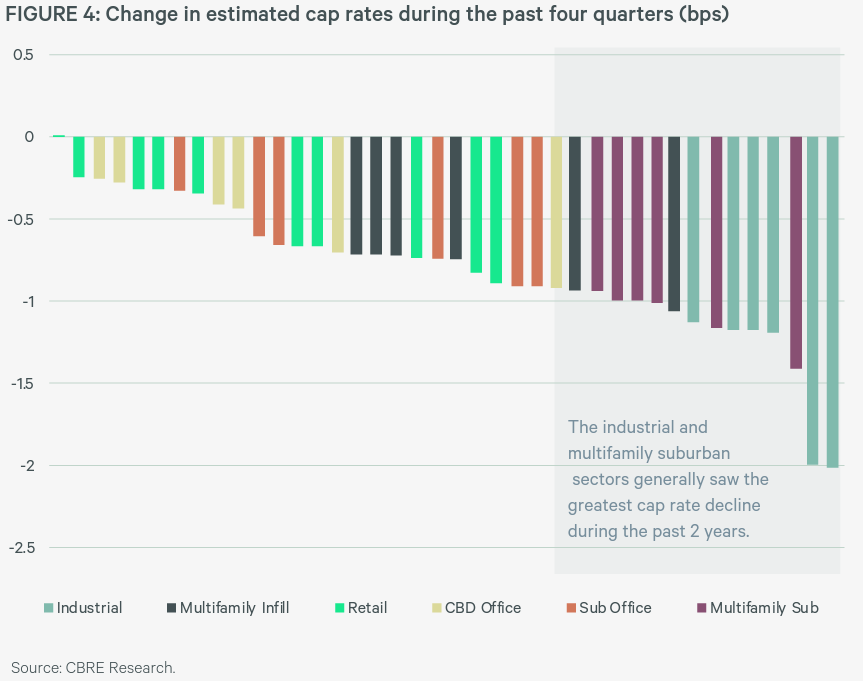

The U.S. industrial sector in particular has seen strong cap rate compression over the last several years, fueled by low interest rates, growth in e-commerce, re-shoring / near-shoring of supply chains, and the shift in inventory requirements from occupiers. This has brought down vacancy levels, increased rental rate growth, and placed upward pressure on values across all submarkets. The below graph from CBRE’s H2 2021 U.S. Cap Rate Survey report shows how compared to all asset classes, the industrial sector has accounted for the greatest decline in yields, regardless of class or risk profile.

Source: CBRE’s H2 2021 U.S. Cap Rate Survey

With the national average cap rates for industrial properties in the range of 3.75% to 4.25% as of H2 2021, the recent interest rate increases have caught many real estate investors by surprise. With the 10-year U.S. Treasury rate hovering around 2.9% as of July 15th, 2022, up about 130 bps from the end of 2021, real estate investors are seeing some upward pressure on cap rates.

To demonstrate how increasing cap rates impact an investor’s equity position, let’s look at an example:

Let’s assume an investor purchased an industrial building for $25 million at a 4% going-in cap rate, implying a year one NOI of $1 million. Now, let’s assume that market cap rates increase from 4% to 5%, resulting in a 20% decrease in property value ($25 million to $20 million). In reality, the investor is likely expecting NOI to increase significantly, as rents are marked up at the building. But, by how much would NOI need to grow in order to maintain the building value? The answer is that NOI would have to grow by 20% in order to offset the cap rate increase from 4% to 5%. That is a significant amount of NOI growth that may or may not occur over a typical hold period of five years. And keep in mind, that’s just to keep the value of the building unchanged, not to mention any increase in property value.

Now, looking at things on a levered basis, how does the change in property value translate to change in equity value? Assuming the investor used a 60% LTV interest-only loan to acquire the property, we can use the following formula to estimate the impact of the cap rate change on the investor’s equity position:

Equity Value % Change = (Asset Value % Change) / (1 – LTV)

Therefore, a 20% decrease in asset value in the above scenario would result in a 50% decline in equity value: 20% / (1 – 60%) = 20% / 40% = 50%.

While the trajectory of cap rates remains to be seen, it’s easy to see a scenario where the cap rate compression over the last 12 to 24 months reverses course, resulting in 25 to 50+ bps increases in cap rates across the board. If this happens, it’s very possible that returns on many properties purchased in 2019 through 2021 will be very lackluster and, at worst, negative.

Going forward, real estate investors will likely become more prudent with their underwriting assumptions, particularly as it relates to the exit cap rate assumption. Given that cap rates change dynamically as investor perceptions surrounding interest rates, investment risk, and growth change, investors need to understand the forces impacting these variables in order to determine a likely range of outcomes.

Final Thoughts

Here’s a final question to consider: Which asset class or sector will be most adversely impacted by the expected increase in market cap rates over the near term? Why? How will these increases impact investment returns?

Looking to learn more? Check out our various professional resources! Whether you have yet to break into the industry or are just starting out in a new role, we have everything you need. All you need to bring is your effort.